Equity protection is not an exercise in founder greed. It is the structural discipline required to ensure long term value and attract sophisticated capital. You likely understand that scaling requires external investment, yet the anxiety of losing control to venture capitalists or co-founders often leads to questions about how to protect my equity as a founder. These risks are manageable through rigorous legal and strategic frameworks that prioritize a clean cap table.

This guide provides the technical mechanisms required to safeguard your ownership while scaling toward a liquidity event. We examine the non-negotiable 30 day 83(b) filing window, the updated $15 million QSBS gain exclusion thresholds for 2026, and the anti-dilution clauses necessary for legal certainty. You will find a clear roadmap to maintaining influence through to exit while positioning your company for premium investor introductions and business listings. Accessing these structural safeguards ensures you remain a qualified candidate for high level financial opportunities.

Key Takeaways

- Distinguish between economic dilution and control dilution to ensure your voting rights remain intact during aggressive growth phases.

- Execute a comprehensive Shareholders’ Agreement and Articles of Association to provide legal certainty over IP and share transfers.

- Utilize convertible instruments and strategic fundraising sequences to understand how to protect my equity as a founder while managing capital influx.

- Eliminate cap table red flags and consolidate fragmented holdings to meet the stringent requirements of pre-IPO and IPO-stage investors.

- Access exclusive business listing services and investor introductions to streamline your path toward a successful and structured exit.

Understanding Equity Dilution and the Founder’s Dilemma

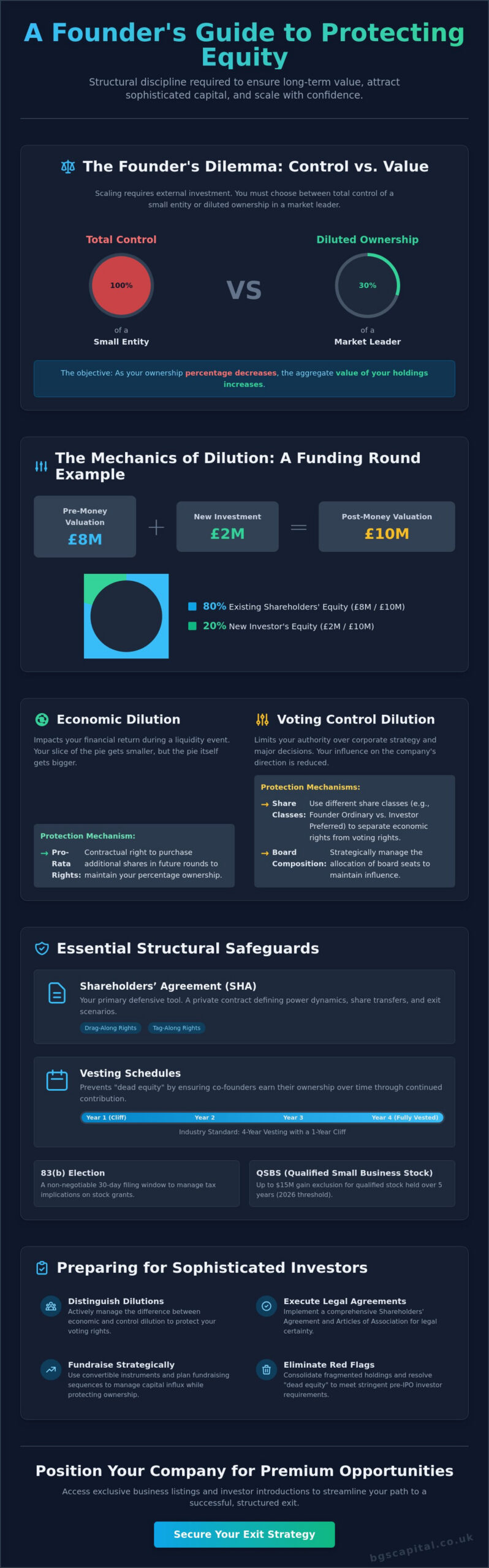

Equity dilution represents the reduction in ownership percentage for existing shareholders when a company issues new stock. This is a standard mechanic of startup funding. Every new round of capital involves a trade-off. You exchange ownership for the resources required to scale. The primary objective is to ensure that while your percentage decreases, the aggregate value of your holdings increases. This is the “Founder’s Dilemma.” You must choose between total control of a small entity or limited influence within a market leader. Understanding Equity Dilution is the first step in managing this transition effectively.

Capital influx validates the business model but introduces new stakeholders. Effective management of this transition is how to protect my equity as a founder without stifling the company’s potential. Investors bring more than just cash; they bring networks and governance requirements that alter the company’s trajectory. Balancing these interests requires a strategic approach to the cap table from the earliest stages of formation.

The Mechanics of Dilution in Funding Rounds

Valuation timing dictates the severity of dilution. A pre-money valuation is the company’s agreed value before investment; the post-money valuation adds the new capital to that figure. If you raise £2 million on an £8 million pre-money valuation, your post-money value is £10 million. The new investor now owns 20%. In a typical Series A round, founders often see their stakes compressed as the option pool is expanded to attract talent. Pro-rata rights are essential here. These contractual provisions grant you the right, but not the obligation, to purchase additional shares in subsequent rounds. They are a critical tool when considering how to protect my equity as a founder from excessive erosion during high growth phases.

Economic vs. Voting Control: A Crucial Distinction

Economic dilution and control dilution are separate risks. Economic dilution impacts your financial return during a liquidity event. Control dilution limits your authority over corporate strategy. Sophisticated founders use share classes to manage this split. Ordinary shares are standard for founders, while investors typically demand Preferred shares with liquidation preferences. Board composition is equally vital. Investors often require board seats as a condition of funding, which can shift the balance of power. In the context of UK company law, control dilution refers specifically to the reduction of a shareholder’s voting power relative to the total number of voting rights in the company. Learning how to protect my equity as a founder requires a technical grasp of these structural differences. Maintaining a clean cap table is the only way to ensure these legal distinctions remain clear as you scale toward an exit.

Structural Safeguards: Vesting, IP Assignment, and Shareholders’ Agreements

A robust legal architecture is the only way to ensure long term security for your holdings. While the Articles of Association provide the public regulatory framework required by UK company law, the Shareholders’ Agreement (SHA) acts as the private contract that defines the actual power dynamics. If you’re investigating how to protect my equity as a founder, the SHA is your primary defensive tool. It establishes drag-along and tag-along rights, ensuring you aren’t left behind during a sale or forced into an unfavorable exit by minority stakeholders.

Vesting schedules serve as a critical contingency against “dead equity.” This occurs when a co-founder departs early but retains a significant ownership stake. Without a vesting mechanism, that equity remains locked, making it nearly impossible to attract future venture capital. A clean cap table requires that equity is earned through continued contribution rather than granted solely at inception. Failure to implement these controls early often results in irreparable cap table damage.

Implementing a Standard Vesting Schedule

The industry standard follows a four-year vesting cycle with a one-year cliff. Under this model, no equity is earned until the first anniversary of service. After the cliff, shares vest monthly or quarterly. Acceleration clauses are equally vital. A single-trigger clause accelerates vesting upon an acquisition. A double-trigger clause requires both an acquisition and the founder’s termination without cause. These provisions ensure that your hard earned ownership isn’t forfeited during corporate restructuring. It’s a fundamental aspect of how to protect my equity as a founder when dealing with aggressive acquirers.

IP Assignment: Who Owns the Code?

Intellectual Property (IP) gaps are a primary reason for failed due diligence. Every participant must sign a comprehensive IP assignment agreement from day one. Informal contributions create “clouds” over ownership. If a founder writes code or designs a brand before the company is legally formed, that IP technically belongs to the individual, not the corporation. Featuring your business on a curated platform often requires proof of these assignments to verify eligibility and professional status. During audits, institutional investors will scrutinize these gaps. Any ambiguity regarding ownership of the core technology can derail a pre-IPO round or an exit. Secure your IP early to maintain the integrity of your cap table.

Fundraising Strategy: Balancing Capital Influx with Ownership Control

Raising capital is a strategic necessity that carries a permanent cost in ownership. Each stage of startup funding introduces specific dilution pressures. Early stage rounds typically focus on speed. Later stages demand rigorous structural protections. Founders must evaluate the long term impact of every term sheet to determine how to protect my equity as a founder during successive raises. Miscalculating the cost of capital at the Seed stage can leave you with insufficient leverage by Series B.

Instruments like Simple Agreements for Future Equity (SAFEs) and convertible notes are standard for delaying valuation. They allow you to defer the equity conversation until a priced round occurs. However, these instruments carry valuation caps that can cause unexpected dilution if the company scales rapidly. Strategic use of debt financing offers a non-dilutive alternative for companies with predictable cash flows. By 2026, the shift toward post-money SAFEs has made cap table modeling essential before any signature is applied. You must also watch for the “Option Pool Shuffle.” Investors often insist that the employee option pool is created or expanded before the investment. This move dilutes the founders specifically, rather than the incoming investors. It’s a subtle tactic that can cost you significant percentage points if left unnegotiated.

Choosing the Right Investor for the Right Stage

The profile of your capital source dictates your level of control. Angel investors often provide more flexible terms because they are investing personal capital. Their goals usually align with founder led growth and longer horizons. Institutional venture capital firms operate under different mandates. They prioritize massive scale and aggressive exit timelines. This pressure can lead to control dilution where founders lose the ability to set the company’s direction. Ensuring investor alignment with your specific exit goals is a primary defense mechanism. Verify the status and track record of any potential partner before engagement. Professional introductions to qualified investors can mitigate the risk of misaligned incentives.

Anti-Dilution Clauses: Protection or Poison?

Anti-dilution clauses protect investors if you raise money at a lower valuation in the future. A Full Ratchet clause is the most aggressive. It resets the investor’s share price to the new, lower price, regardless of how much capital was actually raised. This can be devastating for founder equity. A Broad-Based Weighted Average is the more equitable standard. It accounts for the number of shares issued at the lower price, resulting in less severe dilution for founders. Negotiating pay-to-play provisions is a sophisticated way to balance these scales. These require investors to participate in subsequent rounds to maintain their preferential rights. It is a technical but effective method for how to protect my equity as a founder during a down round. Secure these terms early to maintain the integrity of your ownership through to the exit.

Pre-IPO Preparation: Cleaning the Cap Table for Sophisticated Investors

Sophisticated investors demand structural clarity before committing high-level capital. A messy cap table is a primary deterrent during pre-IPO rounds. You must identify red flags early. Fragmented ownership among inactive early-stage contributors creates “noise” that complicates decision-making. Consolidating these small stakes is a fundamental step in how to protect my equity as a founder. It prevents minority shareholders from holding up major transactions or blocking an exit. Institutional players won’t tolerate the administrative burden of managing hundreds of legacy shareholders with negligible stakes.

Legacy shareholder rights often conflict with institutional requirements. Early investors might hold veto rights or information rights that are no longer appropriate for a late-stage company. These must be renegotiated or terminated before institutional due diligence begins. Additionally, capital gains tax planning should be integrated into your equity structuring. Under the One Big Beautiful Bill Act signed in 2025, the maximum federal gain exclusion for Qualified Small Business Stock (QSBS) acquired after July 4, 2025, is now $15 million. This technical alignment is a core component of how to protect my equity as a founder from excessive taxation at the point of exit.

Cap Table Hygiene for High-Net-Worth Introductions

Institutional players and high-net-worth individuals require transparent, digital cap table management. Spreadsheets are prone to error and insufficient for professional-grade audits. You must eliminate “phantom shares” and undocumented verbal promises immediately. These represent significant legal liabilities that can stop a deal in its tracks. If your cap table contains inactive early shareholders, consider a structured buy-out to simplify the structure. Simplification increases your appeal to the exclusive networks that facilitate pre-IPO liquidity and institutional placement. A clean, digital record provides the legal certainty investors demand.

Preparing for Pre-IPO Due Diligence

Due diligence is an exhaustive audit of your company’s legal foundation. You need a centralized repository for your Shareholders’ Agreement, IP assignments, and vesting records. As established in earlier sections, these documents are the bedrock of ownership. Tax-efficient schemes like EIS also impact the final exit valuation. Investors will verify your compliance with these schemes to ensure their own tax reliefs remain valid. Additionally, companies with a nexus to California must ensure they registered with the DFPI by March 1, 2026, and filed their first annual diversity report by April 1, 2026. Non-compliance with these regulatory shifts can derail an IPO timeline.

Register your interest for professional investor introductions to ensure your cap table meets institutional standards before your next funding round.

Strategic Introductions: How BGS Capital Facilitates Clean Capital Raising

BGS Capital operates as a specialist facilitator within the private equity ecosystem. We provide a conduit to exclusive opportunities for both high growth companies and sophisticated investors. Cold outreach often results in misaligned incentives or predatory terms that compromise your ownership. Direct introductions to established investor relations teams ensure your business reaches those who value structural discipline. This professionalized approach is the final stage in how to protect my equity as a founder. It secures capital from sources that respect the legal frameworks you’ve established.

Our role is strictly that of an intermediary. We facilitate the network and manage the platform where qualifying businesses are featured. We don’t provide financial advice or execute transactions directly. Instead, we offer a structured environment where transparency and compliance are prioritized. This ensures that every introduction is built on a foundation of mutual professional status and verified eligibility.

Gaining Exposure to Sophisticated Networks

The “Feature Your Business” process is designed for companies that have completed their structural due diligence. We filter for high-net-worth individuals and institutional entities that understand complex equity arrangements and 2026 regulatory requirements. A professional listing on our curated platform establishes immediate credibility with these groups. It signals that your company has addressed the IP gaps and vesting schedules discussed in previous sections. This exposure is restricted to a select group of qualified participants, maintaining the exclusivity required for high level capital raising.

The Final Step Toward IPO Readiness

Structural equity protection is the prerequisite for a successful exit. By adhering to the updated QSBS thresholds and maintaining a digital, clean cap table, you position your company for institutional scrutiny. BGS Capital provides the gateway to the networks that facilitate this transition. Professionalizing your capital raising efforts is the most effective way to understand how to protect my equity as a founder during the final stages of growth. Don’t leave your ownership to chance during cold outreach cycles. Verify your eligibility and professional status to access our network.

Are you a founder seeking institutional exposure? Register to feature your business on our curated platform and begin the process of professional investor introductions.

Executing Your Exit Strategy with Structural Discipline

Ownership protection requires a transition from founder intuition to institutional rigor. You’ve established the necessity of timely 83(b) elections, the $15 million QSBS thresholds, and the consolidation of fragmented cap tables. These mechanisms ensure your percentage remains a high value asset rather than a diluted liability. Implementing these safeguards is the definitive answer to how to protect my equity as a founder while navigating institutional growth. Professionalizing your legal architecture today prevents the “dead equity” and IP gaps that derail future liquidity events.

BGS Capital facilitates this transition by providing a conduit to exclusive networks. We specialize in pre-IPO and IPO opportunities, strictly adhering to UK investor classification standards. Our platform offers direct access to a high-net-worth investor network for businesses that have reached the requisite level of structural maturity. Are you ready to professionalize your capital raising efforts?

Feature your business and connect with sophisticated investors today.

Take the final step toward a successful exit by aligning your business with qualified, risk-aware capital.

Frequently Asked Questions

What is the most common mistake founders make with equity?

The most frequent error is the failure to file a Section 83(b) election within the non-negotiable 30 day window after receiving restricted stock. This oversight creates massive tax liabilities as the shares vest and increase in value. Additionally, neglecting to implement vesting schedules for all founders often leads to “dead equity” when a partner departs early with a full ownership stake.

How much equity should I give away in my first funding round?

Founders typically relinquish between 10% and 25% of their company during a standard Seed or Series A round. The exact percentage depends on your pre-money valuation and the capital required to reach your next growth milestone. Understanding the long term impact of this initial dilution is essential for those learning how to protect my equity as a founder during successive raises.

Can a founder be forced out of their own company if they lose majority equity?

A founder can be removed from operational roles if they lose majority voting control and lack specific board protections. Share ownership does not automatically guarantee a permanent executive position or a board seat. You must negotiate protective provisions and board composition rules within the Shareholders’ Agreement to maintain influence despite economic dilution during scaling phases.

What happens to my equity if I leave the company before my vesting cliff?

Departing before a one year cliff usually results in the total forfeiture of all unvested shares. The company retains this equity, ensuring that ownership remains concentrated among those actively contributing to the business. This mechanism protects the cap table from being cluttered with inactive shareholders, which is a primary requirement for attracting sophisticated institutional investors and high-net-worth individuals.

What is a “down round” and how does it affect founder equity?

A down round occurs when a company raises capital at a lower valuation than its previous funding round. This situation leads to severe dilution for existing shareholders, especially if investors have “Full Ratchet” anti-dilution protections. These clauses reset the investor’s share price to the new, lower value, forcing the founder to issue more shares and significantly reducing their ownership percentage.

How do anti-dilution clauses work in a UK Shareholders’ Agreement?

In a UK legal context, anti-dilution clauses typically utilize a “Weighted Average” formula rather than a “Full Ratchet” model. This approach is more equitable as it accounts for both the lower share price and the actual amount of capital raised. These provisions are integrated into the Shareholders’ Agreement to protect investor value during subsequent rounds while preventing the total erosion of founder stakes.

Is it possible to regain equity after it has been diluted?

Regaining equity is possible through performance-based option grants or “top-up” allocations, though this requires board and investor approval. It’s generally difficult to claw back significant percentages once they’re surrendered. Focusing on how to protect my equity as a founder through pro-rata rights and strategic valuation management is a more reliable method for maintaining a substantial stake through to exit.

What role does a “cap table” play in protecting founder ownership?

A capitalization table acts as the definitive ledger for all share ownership, warrants, and option pools. It allows you to model the dilutive impact of new investments before signing a term sheet. Maintaining a clean, digital cap table is a prerequisite for professional investor introductions, as it provides the transparency and legal certainty required for institutional due diligence.