For sophisticated investors and founders, a successful exit is the culmination of significant risk and strategic effort. Yet, a substantial portion of these hard-earned returns can be eroded by an often-misunderstood liability: capital gains tax. The complex rules, rates, and available reliefs surrounding the disposal of business assets or investment portfolios-particularly unlisted and pre-IPO shares-create significant uncertainty and a material risk of overpayment to HMRC.

This definitive guide is engineered to demystify the UK’s Capital Gains Tax framework. We provide a direct breakdown of when CGT applies, how to calculate your potential liability, and most critically, how to strategically utilise key reliefs such as Business Asset Disposal Relief. The objective is to equip you with the essential knowledge required to make tax-efficient decisions, ensuring your final net return is maximised and your exit strategy is as robust in practice as it is on paper.

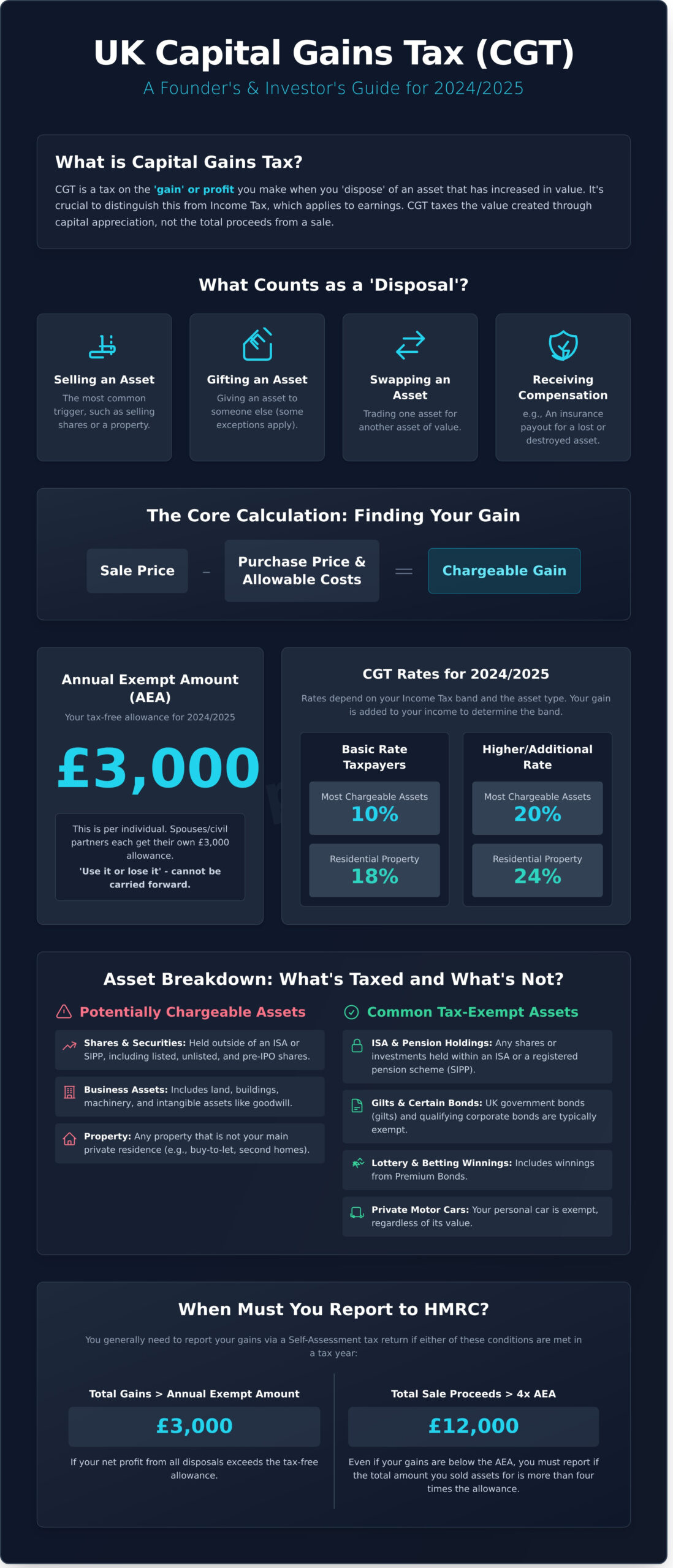

What is Capital Gains Tax (CGT) and Who Pays It?

Capital Gains Tax (CGT) is a UK tax levied on the profit-or ‘gain’-realised upon the disposal of an asset that has increased in value. It is crucial for founders and investors to distinguish this from Income Tax; CGT applies to profits from investments, whereas Income Tax applies to earnings. The core mechanics of Capital Gains Tax in the United Kingdom are designed to tax the value created through capital appreciation, not the total proceeds from a sale.

Liability for CGT generally falls upon UK residents, including individuals, trustees, and personal representatives of a deceased person’s estate. Certain businesses may also be liable. The key trigger for a potential CGT event is the ‘disposal’ of an asset. This term encompasses more than just a straightforward sale and includes:

- Gifting an asset to another person (with some exceptions).

- Swapping an asset for something else.

- Receiving compensation for an asset, such as an insurance payout if it has been lost or destroyed.

The Core Principle: Taxing the ‘Gain’

The fundamental principle of CGT is that tax is only due on the net profit. The chargeable gain is calculated by subtracting the initial purchase price and any allowable costs from the final sale price. For example, if you acquired shares for £50,000 and later sold them for £85,000, your initial gain is £35,000. From this, you can deduct allowable costs such as broker fees or stamp duty, which reduces your taxable gain. This calculation applies to a wide range of assets, including shares, business assets, and property that is not your primary residence.

Who Needs to Report and Pay CGT?

An individual must report and pay capital gains tax if their total gains in a tax year exceed the Annual Exempt Amount (AEA)-a tax-free allowance set by the government. Gains below this threshold do not typically need to be reported to HMRC, provided your total sale proceeds are not more than four times the AEA. Reporting is completed via a Self-Assessment tax return. It is also important to note that specific rules apply to non-UK residents who dispose of UK property or land, who may be liable for CGT regardless of their residency status.

Key Assets Subject to CGT for Investors and Founders

For founders and sophisticated investors, understanding which assets are subject to Capital Gains Tax (CGT) is fundamental to effective portfolio management and strategic exit planning. The default position under UK tax law is that any gain realised from the disposal of a ‘chargeable asset’ is potentially liable for tax unless a specific exemption or relief applies. The scope is broad, encompassing most forms of property and investments. For definitive rules and current allowances, investors should consult the official government guidance on Capital Gains Tax provided by HMRC.

Shares and Securities

This is the most common category of chargeable asset for investors. Any shares held outside of a tax-efficient wrapper, such as an ISA or a SIPP, fall within the scope of CGT. This applies equally to shares in publicly listed companies and unlisted securities in private companies-a critical consideration for those involved in pre-IPO and early-stage ventures. Calculating the gain can be complex due to HMRC’s ‘share pool’ and ‘matching’ rules, which are designed to prevent tax avoidance strategies like ‘bed and breakfasting’.

Business Assets

When selling all or part of a business, founders must consider the CGT implications on various assets. This includes tangible assets like land, buildings, plant, and machinery used in the trade. Furthermore, intangible assets are also chargeable. A significant example is goodwill, which represents the business’s reputation and customer base and can hold substantial value. The disposal of a stake in a business partnership is also a chargeable event for capital gains tax purposes.

Common Tax-Exempt Assets

While most assets are chargeable, several important exemptions exist that are crucial for strategic financial planning. Key tax-free assets include:

- Shares and other investments held within an Individual Savings Account (ISA) or a registered pension scheme (like a SIPP).

- UK government bonds (gilts) and certain corporate bonds.

- Winnings from betting, lotteries, or pools, including Premium Bonds.

- Your main private residence, provided it meets the conditions for Private Residence Relief (PRR).

- Private motor cars, regardless of their value.

Calculating Your CGT Liability: Rates and Allowances for 2024/2025

To effectively manage your investment portfolio as a founder, a precise understanding of how your Capital Gains Tax (CGT) liability is calculated is essential. The process involves applying the correct tax rates to your net gains after considering any available allowances and losses. The figures and rules detailed here are for the 2024/2025 UK tax year and are subject to change in future government budgets.

The Capital Gains Tax Annual Exempt Amount (AEA)

For the 2024/2025 tax year, every individual has an Annual Exempt Amount (AEA) of £3,000. This is the maximum amount of capital gain you can realise in a tax year without having to pay any tax. It is a ‘use it or lose it’ allowance; it cannot be carried forward to subsequent years. Notably, spouses and civil partners each receive their own separate £3,000 AEA, which can be a valuable tool in strategic tax planning for joint asset disposals.

CGT Rates: How Your Income Tax Band Matters

The rate of tax you pay on gains above your AEA is determined by your Income Tax band and the type of asset you have sold. To find the correct rate, your total taxable gains are added to your total taxable income. For the most current and detailed information, refer to the official government guidance on Capital Gains Tax rates and allowances. The rates are as follows:

- For basic rate taxpayers: You will pay 10% on gains from most chargeable assets (such as shares) and 18% on gains from residential property.

- For higher or additional rate taxpayers: You will pay 20% on gains from most chargeable assets and 24% on gains from residential property.

If your gains span across the basic and higher rate income tax bands, you will pay the corresponding rate for each portion of the gain.

Using Capital Losses to Reduce Your Bill

A capital loss occurs when you dispose of a chargeable asset for less than its acquisition cost. These losses are a powerful tool for reducing your overall tax liability. You can offset capital losses against capital gains from the same tax year, thereby reducing your net taxable gain. You must report the loss to HMRC, typically via your Self Assessment tax return. If your total losses exceed your gains in a year, the unused losses can be carried forward indefinitely to offset gains in future years.

Strategic Tax Reliefs for Business Owners and Investors

For founders and sophisticated investors, understanding the available tax reliefs is critical. These government-approved schemes are designed to incentivise entrepreneurship and investment into UK businesses by significantly reducing the effective rate of capital gains tax on qualifying assets. However, eligibility is dependent on meeting a series of strict conditions, making professional tax advice an essential component of any disposal or investment strategy.

Business Asset Disposal Relief (BADR)

Formerly known as Entrepreneurs’ Relief, BADR is a key relief for company founders. It reduces the rate of CGT to a flat 10% on gains from qualifying disposals, subject to a lifetime limit of £1 million in gains. For the disposal of company shares, the main conditions require the individual to be an employee or officer and hold at least 5% of the ordinary share capital for a minimum of two years leading up to the sale.

Investors’ Relief

Investors’ Relief extends a similar 10% CGT rate to external investors in unlisted trading companies. This relief has its own separate lifetime limit of £10 million. It is designed to encourage long-term investment from individuals who are not directly involved in the company’s operations. Key conditions include that the shares must be newly issued, subscribed for in cash, and held for a minimum of three years from the date of issue. This makes it particularly valuable for angel and early-stage investors.

SEIS and EIS Reinvestment Relief

The Seed Enterprise Investment Scheme (SEIS) and Enterprise Investment Scheme (EIS) offer a powerful mechanism for managing CGT liability. These schemes allow an investor to defer a capital gain made on any asset by reinvesting that gain into shares of a qualifying SEIS or EIS company. This is a deferral relief, not a permanent exemption; the original gain becomes chargeable when the SEIS/EIS shares are eventually sold. For serial investors, this is a highly effective tool for rolling over gains and strategically managing their tax position over the long term.

For those looking to leverage these advantages, identifying qualifying opportunities is the first step. Explore tax-efficient pre-IPO investment opportunities.

Reporting and Paying CGT: Key Deadlines and Procedures

Understanding your liability is critical, but compliance with HMRC’s reporting and payment protocols is non-negotiable for founders and investors. Failure to adhere to these procedures can lead to significant penalties, undermining your investment returns. This guide outlines the essential steps to ensure you remain compliant.

How to Report Your Capital Gains

There are two primary methods for reporting gains to HMRC, depending on the asset type. For most disposals, including shares and other business assets, you must declare the gain on the supplementary pages (SA108) of your annual Self Assessment tax return. However, a separate, accelerated process applies to the disposal of UK residential property. These gains must be reported and the estimated tax paid via HMRC’s ‘real time’ Capital Gains Tax service, even if you are not otherwise in Self Assessment.

To complete any report, you will require precise information, including:

- The asset description and the dates of acquisition and disposal.

- The disposal proceeds and the original acquisition cost.

- Details of all allowable costs associated with buying and selling the asset.

Payment Deadlines

Meeting payment deadlines is fundamental to avoiding financial penalties. The standard deadline for paying your capital gains tax bill through Self Assessment is 31st January following the end of the tax year in which you made the gain. For example, a gain made in the 2023/24 tax year must be paid by 31st January 2025.

The deadline for UK residential property disposals is significantly shorter. The tax must be reported and paid within 60 days of the sale’s completion date. Late reporting and payment attract immediate penalties and interest charges from HMRC.

The Importance of Good Records

Accurate calculation and reporting are entirely dependent on meticulous record-keeping. As a founder or investor, it is your responsibility to maintain a comprehensive file for every asset. HMRC can request these records during an enquiry to verify your calculations. Essential documents to retain include:

- Contract notes confirming purchase and sale prices and dates.

- Invoices for transaction costs, such as broker fees, stamp duty, or legal fees.

- Evidence supporting any claims for tax reliefs.

- For property, records of capital improvement costs.

Robust records provide the necessary evidence to calculate your gain correctly and substantiate your tax position if challenged by HMRC.

Navigating Capital Gains Tax to Secure Your Returns

Navigating the complexities of UK capital gains tax is a critical discipline for any serious investor or founder. As we’ve detailed, a comprehensive understanding of your liabilities, the full utilisation of the Annual Exempt Amount, and the strategic application of reliefs are fundamental to protecting your returns. Adhering to HMRC’s strict reporting and payment deadlines is equally crucial for maintaining full compliance and avoiding unnecessary penalties.

While diligent tax planning preserves wealth, strategic investment is the engine that creates it. For sophisticated and high-net-worth investors seeking their next venture, accessing properly vetted opportunities is paramount. BGS Capital provides a direct conduit to exclusive pre-IPO and IPO deals, facilitating direct introductions to investor relations teams and connecting you with a network of qualified market participants.

Take the next decisive step in building your portfolio. Connect with pre-vetted investment opportunities. By mastering both your tax obligations and your investment strategy, you position yourself to build a more robust and successful financial future.

Frequently Asked Questions

What is the 30-day rule for Capital Gains Tax on shares?

The 30-day rule is an anti-avoidance provision to prevent ‘bed and breakfasting’-selling shares to realise a loss and immediately repurchasing them. If you sell shares at a loss and repurchase the same class of shares within 30 days, the loss cannot be immediately claimed. Instead, the loss is added to the cost basis of the newly acquired shares, deferring the tax benefit until the new shares are eventually sold. This rule also applies to purchases made by a spouse.

Do I have to pay Capital Gains Tax if I gift an asset to my children?

Yes, gifting an asset to a ‘connected person,’ including children, is a disposal at market value for tax purposes. You are liable to pay capital gains tax on any gain, calculated as the market value at the time of the gift minus your original acquisition cost. This applies even though you receive no cash proceeds. Certain reliefs may be available, and transfers between spouses or civil partners are typically exempt. Professional advice is recommended to manage this liability effectively.

How does Capital Gains Tax work when someone dies?

Upon an individual’s death, assets are revalued to their market value at that date. This creates a ‘capital gains-free uplift,’ meaning the beneficiary inherits the assets at their current value, and any historic gain is not subject to CGT. No Capital Gains Tax is due on death, although the estate may be subject to Inheritance Tax. If the beneficiary later disposes of the asset, their cost basis for calculating future gains will be the market value at the date of death.

Can I offset property losses against gains from shares?

Yes, in the UK, capital losses can be offset against capital gains from any type of asset in the same tax year. A loss realised from the disposal of a property can be used to reduce a taxable gain from the sale of shares, thereby lowering your overall CGT liability. If your total losses exceed your total gains in a tax year, the net loss can be carried forward indefinitely to offset against future gains, provided the loss is reported to HMRC within the time limit.

What are the CGT implications of employee share options (EMI scheme)?

Exercising Enterprise Management Incentive (EMI) options does not typically trigger a Capital Gains Tax charge. The taxable event occurs upon the eventual sale of the shares acquired through the scheme. When these shares are sold, CGT is calculated on the gain-the difference between the sale price and the exercise price. Provided specific conditions are met, these gains may qualify for Business Asset Disposal Relief, which reduces the effective CGT rate to 10% on qualifying gains.

Is cryptocurrency subject to Capital Gains Tax in the UK?

Yes, in the UK, cryptoassets like Bitcoin and Ethereum are treated as property for tax purposes. Disposing of cryptoassets is a taxable event and is subject to Capital Gains Tax. A disposal includes selling for fiat currency (e.g., GBP), exchanging one cryptoasset for another, or using them to pay for goods or services. Any profit realised from these disposals above the annual exempt amount must be declared to HMRC and is liable for capital gains tax at the relevant rate.