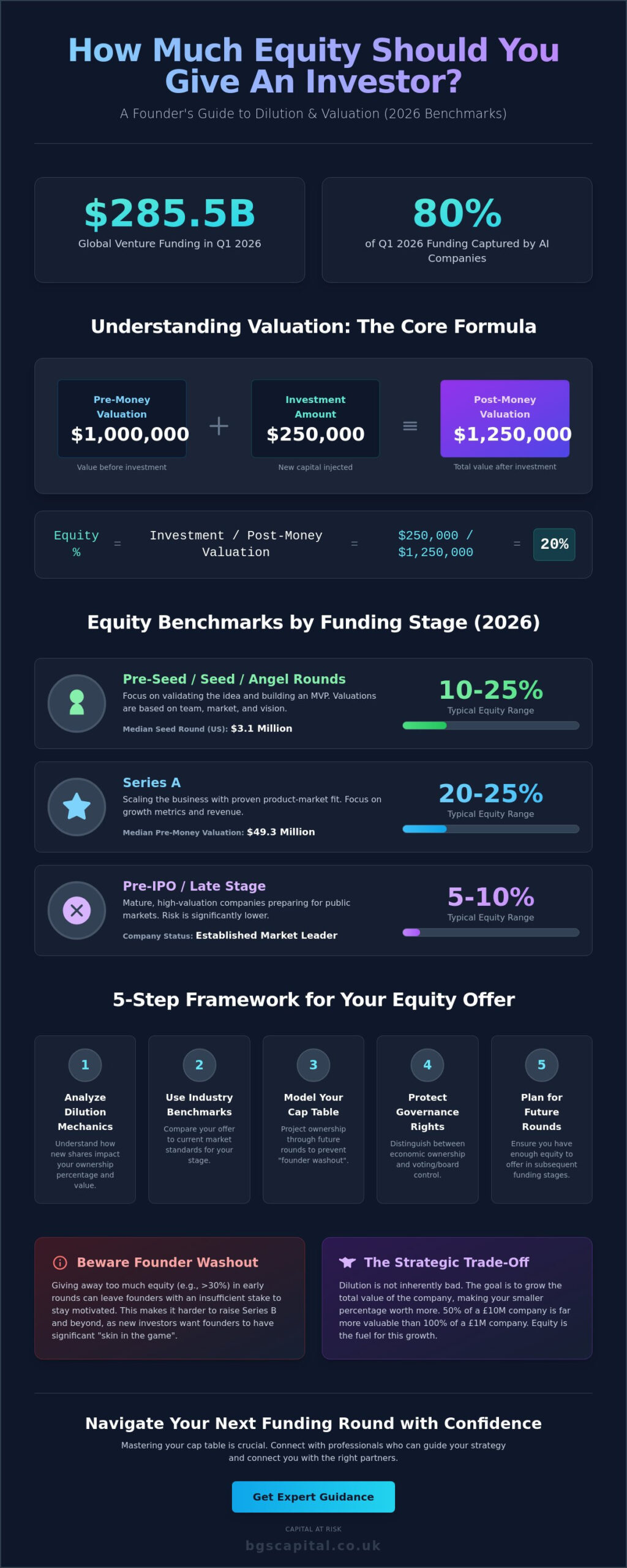

In Q1 2026, AI-related companies captured 80% of the $285.5 billion in global venture funding. This concentration of capital forces founders to ask exactly how much equity should I give an investor to remain competitive without sacrificing control. You likely understand that equity is your most expensive currency. It’s difficult to weigh the need for liquidity against the risk of losing majority governance, especially when median Series A pre-money valuations reached $49.3 million in late 2025.

This guide provides the benchmarks and formulas required to master equity dilution at every stage of growth. You’ll find the standard ranges for your next round, from the 10-20% typical of pre-seed funding to the 20-25% expected at Series A. We’ll also cover how to calculate precise offers using pre-money and post-money valuations while ensuring your cap table remains compliant with UK-specific tax requirements. CAPITAL AT RISK.

Key Takeaways

- Analyze the technical mechanics of equity dilution to ensure your valuation accurately reflects the ownership percentage granted.

- Determine how much equity should I give an investor by utilizing 2026 industry benchmarks to prevent founder washout.

- Implement a 5-step framework to transition from capital requirements to a finalized cap table supported by professional financial modeling.

- Distinguish between economic ownership and governance rights to protect your board control and long-term founder interests.

- Understand the shifting equity requirements for pre-IPO rounds and the strategic role of professional introducer networks in these transactions.

The Fundamentals of Equity Dilution and Valuation

Equity isn’t just a number; it’s a permanent claim on your company’s future. Within the capital stack, equity sits behind debt but offers the highest potential for returns. For founders, the central question is how much equity should I give an investor to secure growth capital without compromising future rounds. This decision relies on an inverse relationship: as your company’s valuation increases, the percentage of equity required to secure the same investment amount decreases. Calculating how much equity should I give an investor requires a granular understanding of your current cap table and your projected capital needs over the next 18 to 24 months.

Investors view equity as a vehicle for risk. Every transaction involves a transfer of ownership in exchange for capital. It’s essential to recognize that all CAPITAL AT RISK remains the primary concern for the incoming party. If you dilute too aggressively during the pre-seed or seed stages, you risk “founder washout” before reaching Series B. This makes the initial valuation negotiation a critical pivot point for your long-term governance and exit strategy.

Pre-Money vs. Post-Money Valuation

The mathematical distinction between pre-money and post-money valuation determines your final ownership stake. Use the formula: Equity % = Investment / Post-Money Valuation. For example, if your company has a $1 million pre-money valuation and you accept a $250,000 investment, your post-money valuation becomes $1.25 million. The investor receives 20% of the company because $250,000 divided by $1,250,000 equals 0.20. Post-money valuation is the total value of the company after the cash injection. Failing to distinguish these figures often leads to founders inadvertently giving away more control than intended during early-stage negotiations.

The Dilution Effect: How Your Slice Changes

Dilution occurs whenever a company issues new shares. While your percentage of ownership decreases, the objective is to increase the total value of your remaining shares. Understanding The Fundamentals of Equity Dilution is vital for long-term planning. A 50% stake in a company valued at £10 million is objectively more valuable than 100% of a £1 million company. This process is a strategic trade-off where you exchange a portion of your upside for the capital required to scale operations. It’s helpful to consult a guide on equity definitions to understand how these stakes are treated under UK tax law. Managing dilution effectively ensures you retain enough “skin in the game” to stay motivated while providing investors with a meaningful entry point.

Benchmarking Equity by Funding Stage: 2026 Standards

Equity benchmarks are primarily determined by a company’s risk profile and its current growth stage. In the 2026 venture market, where Q1 global funding reached an unprecedented $285.5 billion, investors prioritize capital efficiency and scalable business models. Professional venture capital firms use these benchmarks to assess whether a founder’s strategic planning accounts for long-term sustainability. If you offer too much equity early, you risk “founder washout” by Series B, where your remaining stake may no longer provide sufficient incentive for high-level execution. Conversely, Pre-IPO rounds often see equity percentages drop to the 5-10% range as valuations move toward the hundreds of millions.

When determining how much equity should I give an investor, you must balance the immediate need for liquidity against your future governance requirements. A general guiding principle for equity offers suggests staying within the 10-20% range for pre-seed and seed rounds. Surpassing the 30% threshold in a single early round is dangerous; it leaves insufficient “dry powder” in your cap table for the 20-25% dilution typically expected at Series A. If you are preparing a high-growth business for its next round, consider how a professional business listing can help you reach the right accredited partners.

Seed and Angel Rounds: The 10% to 25% Range

For early-stage raises, 20% remains the industry “sweet spot” for lead investors seeking significant influence. While angel investors might provide bridge capital for smaller stakes, professional firms typically demand enough ownership to justify their operational involvement. In 2026, the median seed round in the U.S. reached $3.1 million, putting immense pressure on founders to justify their valuations. If your valuation is too high, you may struggle to meet the performance milestones required for a subsequent Series A. If it’s too low, you surrender control before the business has reached its full potential.

The UK Context: SEIS and EIS Implications

In the United Kingdom, EIS schemes significantly alter negotiation dynamics. These tax incentives make lower valuations more palatable for sophisticated investors by de-risking the capital at risk. However, strict regulations apply to these transactions. An individual investor cannot own more than 30% of the company’s ordinary shares to remain eligible for EIS tax relief. Consequently, many UK investors seek an equity percentage that maximizes their tax efficiency without breaching this regulatory ceiling. When deciding how much equity should I give an investor in a UK-based raise, align your offer with these limits to maintain investor interest and compliance.

How to Calculate Your Equity Offer: A 5-Step Framework

Moving from theoretical benchmarks to a concrete offer requires a rigorous financial model. Sophisticated investors will perform deep due diligence on your figures. They adopt an “Am I Eligible?” mindset when reviewing your cap table. They look for clean structures and sustainable founder stakes. If your calculations are flawed, you risk losing credibility before the term sheet is even drafted. Determining how much equity should I give an investor starts with a clear understanding of your capital requirements and a defensible valuation. All CAPITAL AT RISK must be justified by specific growth milestones and a clear path to the next funding round.

Step 1: Determine Your 18-Month Capital Requirement

You should raise enough capital to cover 18 months of runway, plus a 20% buffer for unforeseen market shifts. Over-raising leads to unnecessary dilution; under-raising often forces founders into “down rounds” when cash runs low. Map every pound of capital to specific milestones like product launches or hitting a specific annual recurring revenue (ARR) target. In the Q1 2026 market, where the median U.S. seed round reached $3.1 million, investors expect to see precise allocation strategies before committing funds.

Step 2: Establish a Defensible Post-Money Valuation

Valuation is a negotiation, not a fixed science. When valuing your company by funding stage, use comparable company analysis (CCA) and discounted cash flow (DCF) methods to build a range of values. This data-driven approach allows you to justify your ask during high-stakes discussions. If you’re using convertible notes or SAFEs, pay close attention to “valuation caps.” These caps set the maximum price at which your debt converts into equity, directly impacting how much equity should I give an investor during the next priced round.

Step 3: Account for the Option Pool Shuffle

Professional investors usually require an unallocated option pool of 10% to 15% before they close the round. This is known as the “option pool shuffle.” It effectively lowers your pre-money valuation because the pool is created from the founder’s shares, not the investor’s. This process dilutes you further before the new capital even hits the bank. To protect your equity, negotiate the pool size based on your actual hiring plan for the next 18 months rather than accepting a generic industry percentage. A smaller, well-justified pool preserves more of your ownership while still satisfying investor requirements for talent acquisition.

Critical Factors That Influence Investor Equity Demands

Traction acts as the ultimate shield against excessive dilution. When asking how much equity should I give an investor, founders often overlook that equity is essentially a price paid for risk. High growth and consistent revenue reduce the perceived risk; this allows you to retain a larger portion of the business. In the first quarter of 2026, AI-related companies accounted for 80% of total global venture funding. This concentration of capital creates high-conviction deals where founders have significant leverage to negotiate lower equity grants. If your business shows a clear path to profitability, you’re in a stronger position to dictate terms.

The Management Team and Market Timing

The experience of your leadership team directly impacts your valuation. Second-time founders with successful exits typically give away 5-10% less equity in early rounds than first-time entrepreneurs. Investors pay a premium for a proven track record. Market timing also plays a decisive role. When a sector is “hot,” such as AI or aerospace in 2026, valuations rise and equity demands fall. For unproven or first-time teams, the CAPITAL AT RISK disclaimer is a functional reality. Investors in these scenarios demand higher equity stakes to compensate for the operational risks associated with an unvetted management structure.

Governance vs. Equity: Protecting Your Vote

Economic ownership doesn’t always equal control. You can lose control of your company with 40% equity or maintain it with 10% depending on your share classes. High-growth firms often use “Alphabet Shares” or Class A and B structures to separate voting rights from financial interest. This allows founders to raise capital while keeping board control. It’s critical to understand these nuances before signing a term sheet. Choosing the right partner is just as important as the percentage you offer. Review our strategic guide on finding investors to identify partners who align with your long-term vision. To increase your visibility to accredited firms, you can feature your business on our platform today.

Navigating Equity in Pre-IPO and IPO Rounds

Transitioning from private growth to a public listing requires a fundamental shift in how you value ownership. At this sophisticated stage, the question of how much equity should I give an investor is no longer about early-stage survival. It’s about cap table optimization for institutional scrutiny. Valuations at this level often exceed the $118.9 million median seen in Series B primary rounds in late 2025. Consequently, equity grants for new capital usually fall into the single digits. This phase also introduces secondary placings, allowing early stakeholders to liquidate portions of their holdings without additional corporate dilution.

BGS Capital functions as a specialist introducer in this high-stakes environment. We don’t facilitate raises ourselves or provide financial advice. Instead, we act as a network conduit, connecting qualified companies with accredited investment firms and wealth managers. Maintaining a clean cap table is essential for any firm seeking to attract this level of institutional interest. All CAPITAL AT RISK warnings must be clearly communicated to participants during these sophisticated transactions.

The Role of Sophisticated and High-Net-Worth Investors

Sophisticated investors entering pre-IPO rounds prioritize stability and proven business fundamentals. While they may take smaller equity percentages than early-stage venture capitalists, their ticket sizes are significantly larger. Access to these exclusive opportunities is strictly controlled. Every prospective participant must pass an “Am I Eligible?” qualification gate to ensure they meet the regulatory requirements for high-level investing. If you’re leading a high-growth firm, you can feature your business on our platform to gain visibility among these accredited groups.

Preparing for the Exit: Equity and IPOs

A fragmented cap table can stall a public listing. Institutional investors and underwriters look for consolidated ownership structures that are easy to manage and audit. Legacy issues, such as small stakes held by early contractors or unallocated shares, create friction during due diligence. In the first quarter of 2026, 22 traditional IPOs raised over $9.4 billion, proving that the market remains open for companies with professionalized equity structures. To prepare for a liquidity event, you must ensure your answer to how much equity should I give an investor aligns with the expectations of late-stage institutional partners. Consolidating your cap table early prevents delays during the final transition to the public markets.

Feature your business with BGS Capital to connect with sophisticated investors.

Strategic Equity Management for Long-Term Growth

Securing capital while maintaining governance requires a data-driven approach to dilution. You’ve seen that 2026 benchmarks favor companies with high-conviction AI models and proven management teams. Whether you’re navigating a seed round or preparing for a $75 million Regulation A+ Tier 2 offering; the decision of how much equity should I give an investor determines your final exit value. Protecting your stake involves more than just valuation. It requires a clean cap table that passes institutional scrutiny. CAPITAL AT RISK.

BGS Capital operates as a specialized network conduit for qualified companies. We provide direct access to sophisticated and high-net-worth investors interested in pre-IPO and IPO opportunities. Our platform remains strictly compliant with UK financial regulations to ensure a professional environment for all parties. RAISING CAPITAL? FEATURE YOUR BUSINESS ON BGS CAPITAL to connect with our network of accredited investment firms. Your strategic growth deserves a partner that understands the mechanics of high-level finance. We look forward to seeing your business scale.

Frequently Asked Questions

Is 20% equity too much for a seed round in 2026?

A 20% equity grant is a standard benchmark for lead investors in a priced seed round. While some founders negotiate lower percentages in high-growth sectors like AI, professional firms typically require this stake to justify their operational involvement. If you give away more than 25% at this stage, you risk losing the flexibility needed for subsequent Series A dilution.

Can I give away equity to advisors instead of cash?

Issuing equity to advisors is a common practice for cash-constrained startups. Most advisor grants range from 0.1% to 1.0% of the total cap table, usually vesting over a 24-month period. Using a standard Founder Advisor Standard Template (FAST) helps define these expectations without the need for immediate liquidity or cash compensation.

How do I protect my majority control if I need significant capital?

Founders protect control by implementing dual-class share structures where founder shares carry ten votes for every one investor vote. This allows you to raise capital while maintaining governance. You should also focus on board composition rather than just ownership percentages, as board seats dictate the company’s strategic direction and major corporate actions.

What happens to my equity if the company has a ‘down round’?

In a down round, your equity is significantly diluted because new shares are issued at a lower price than previous rounds. If investors have full ratchet anti-dilution protection, they receive additional shares to maintain their value at your expense. This process can trigger a washout where founder stakes are reduced to negligible levels. CAPITAL AT RISK.

Do investors always require a board seat regardless of equity percentage?

Board seats are typically reserved for lead investors or those holding at least 10% to 15% of the company. Passive investors or those with smaller stakes may receive observer rights instead. These rights allow them to attend meetings and receive information without having a formal vote on corporate decisions or executive appointments.

How does the SEIS 30% rule affect how much equity I can give?

The SEIS and EIS 30% rule limits an individual investor’s stake to 29.9% to maintain their tax relief eligibility. When calculating how much equity should I give an investor in the UK, this threshold acts as a natural ceiling. If an investor exceeds this limit, they lose their 30% to 50% upfront income tax relief, making the deal less attractive.

What is an ‘option pool’ and why do investors insist on it?

An option pool is a block of shares set aside for future employees, typically representing 10% to 15% of the post-money cap table. Investors insist on this pool being created from the pre-money valuation to ensure their own stake isn’t diluted by your future hiring. When determining how much equity should I give an investor, you must factor in this pool shuffle as it directly reduces your ownership.

Can I buy back equity from early investors later?

Buying back equity is possible through secondary transactions or during a liquidity event. Sophisticated investors often check their eligibility for secondary buybacks to lock in early gains. Most term sheets include a Right of First Refusal (ROFR), which gives the company the first opportunity to buy shares from an investor who wants to exit. This process requires professional legal structuring.