Could a single clause in your investment agreement determine whether your equity remains intact or evaporates during a down round? While venture funding reached $425 billion in 2025, AI-focused companies captured 65% of all venture deal value, leaving non-AI sectors to face rigorous valuation scrutiny. You recognize that protecting your ownership percentage is a critical priority when market volatility strikes. This guide provides anti-dilution provisions explained for the professional investor who requires a technical understanding of cap table mathematics.

You’ll master the mechanics of Full Ratchet and Weighted Average protections to ensure your capital is insulated from dilutive events. We’ll examine how the May 19, 2026 SEC Registered Offering Reform, which proposed eliminating the one-year seasoning requirement for Form S-3, influences pre-IPO liquidity and your current negotiation leverage. This analysis provides a clear breakdown of 2026 market standards to help you secure superior terms in your next investment agreement.

Key Takeaways

- Identify the specific triggers of down rounds and how anti-dilution clauses serve as a primary risk management tool for private equity shareholders.

- Evaluate the technical differences between Full Ratchet and Weighted Average mechanisms to determine the most effective level of capital protection.

- Review the mathematical impact of narrow versus broad definitions of “outstanding shares” through the anti-dilution provisions explained in our technical breakdown.

- Analyze the strategic trade-offs between aggressive equity protection and the long-term investability of a company to avoid “death spiral” scenarios.

- Understand the nuances of IPO ratchets and ROI guarantees that protect your position during the transition to public markets.

What are Anti-Dilution Provisions in Private Equity?

Anti-dilution provisions are contractual mechanisms embedded in investment agreements to protect existing shareholders from equity devaluation. These clauses activate specifically during a “down round,” which occurs when a company issues new shares at a valuation lower than in previous funding cycles. For sophisticated investors, having anti-dilution provisions explained is less about understanding a definition and more about mastering a risk management tool. These provisions ensure that if a company’s market value contracts, the investor’s ownership percentage is adjusted to reflect the new price reality.

The primary beneficiaries of these protections are holders of convertible preferred shares. This group typically includes venture capital firms and high-net-worth private investors who require safeguards against the inherent risks of Stock Dilution. Without these clauses, an investor who provided capital at a $100 million valuation could see their stake significantly diminished if the company later raises funds at a $50 million valuation. These terms are foundational to venture capital deal structures, serving as a hedge against the volatility often found in high-growth sectors.

Why Investors Demand Anti-Dilution Protection

Volatility in private markets requires a robust defensive strategy. Investors demand these protections to ensure their original capital maintains a proportionate share of the eventual “exit pie.” During challenging market cycles, these provisions align founder and investor interests. They force a disciplined approach to valuation and provide a clear framework for how the cap table will rebalance if performance targets are missed. This alignment is critical for maintaining investor confidence when capital markets tighten.

The Legal Basis: Convertible Preferred Shares

The technical execution of these provisions relies on the conversion ratio. Most startup funding documentation specifies that preferred shares convert into ordinary shares at a 1:1 ratio. When an anti-dilution trigger is met, this ratio is adjusted. The investor receives more ordinary shares upon conversion, effectively lowering their average price per share. While “price-based” anti-dilution is the industry standard, some agreements include “contractual” anti-dilution, which may offer broader protections. Understanding these distinctions is vital for any professional reviewing term sheets or participating in private placements.

Full Ratchet vs. Weighted Average Anti-Dilution

The distinction between Full Ratchet and Weighted Average mechanisms is the most critical factor in determining an investor’s downside protection. These two methods represent opposite ends of the equity preservation spectrum. While one provides absolute protection against price drops, the other seeks a mathematical compromise. Having anti-dilution provisions explained through this comparison reveals how cap table dynamics shift during distressed funding events. For an in-depth analysis of anti-dilution provisions, legal and economic frameworks suggest that the chosen method dictates the long-term relationship between capital providers and founders.

The Full Ratchet Mechanism

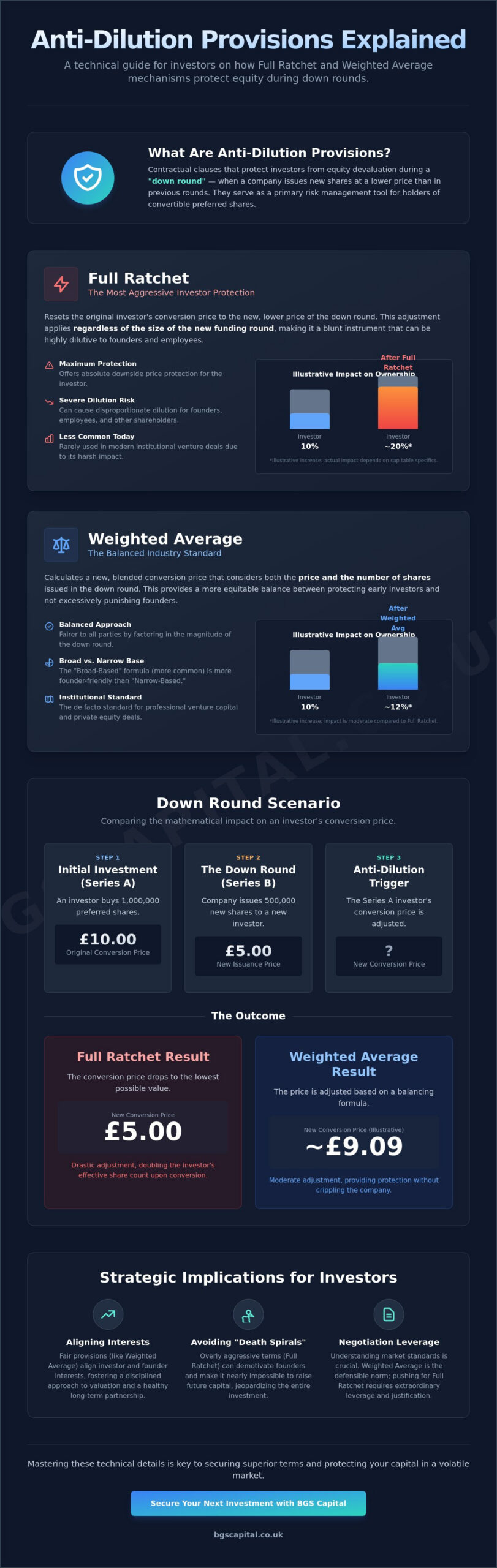

Full Ratchet is the most aggressive form of protection. It resets the investor’s conversion price to the lowest price offered in any subsequent round, regardless of the amount of capital raised. This is an “all-or-nothing” adjustment. Consider a scenario where an investor holds a 10% stake purchased at £10 per share. If the company later raises a small bridge round at £5 per share, the Full Ratchet provision resets the original investor’s conversion price to £5. The size of the round doesn’t matter. Even a tiny issuance of shares can trigger a massive adjustment, often causing severe dilution for founders and employees. It is a blunt instrument for protecting value.

The Weighted Average Approach

Weighted Average anti-dilution is the de facto standard for institutional-grade deals. It uses a formula to determine the new conversion price by considering both the price and the number of shares issued in the new round. This method balances the interests of new investors, old investors, and founders more equitably than a ratchet. It prevents excessive dilution from small, lower-priced rounds while still offering protection. Within this category, you must distinguish between Broad-Based and Narrow-Based formulas. Broad-Based is more common as it includes all common stock equivalents, resulting in a less severe adjustment for the company.

Current market standards among UK angel investors and VCs heavily favour the Broad-Based Weighted Average approach. It maintains the “investability” of the company for future rounds. Sophisticated participants use these terms to signal their technical proficiency and long-term commitment to the business. If you are looking to expand your portfolio with companies that adhere to these professional standards, you can view current business listings to identify qualified opportunities. Mastering these technicalities ensures you negotiate from a position of authority when reviewing term sheets in volatile markets.

Calculating the Impact: Formulas and Down Round Scenarios

Precision in documentation requires a firm grasp of the underlying mathematics. To have anti-dilution provisions explained effectively, one must look past the definitions and into the formulas that govern cap table rebalancing. These calculations determine exactly how many additional ordinary shares an investor receives when a down round occurs. We’ll use a hypothetical scenario where a company’s valuation drops from £50 million to £30 million to illustrate the diverging outcomes of these provisions. The resulting adjustment defines the power dynamic of the cap table for all subsequent funding rounds.

The Weighted Average Formula Explained

The Weighted Average formula represents the ratio of shares that should’ve been issued at the original price versus the shares actually issued at the lower price. The industry-standard formula is expressed as CP2 = CP1 * (A + B) / (A + C). In this equation, CP2 is the new conversion price and CP1 is the original price. The variable “A” represents the number of shares outstanding before the new issue. “B” is the number of shares that would’ve been issued if the new capital had been raised at the original price, while “C” is the actual number of new shares issued.

The definition of “A” is the most contested variable in technical negotiations. A Broad-Based Weighted Average includes all common stock equivalents, such as unissued options and warrants. This inclusive definition dilutes the impact of the adjustment, making it the preferred standard for founders. Narrow-Based formulas only count shares currently issued and outstanding. By excluding the option pool, Narrow-Based adjustments are significantly more punitive for founders and earlier employees. Sophisticated investors must verify which definition is being used in the shareholder agreement to accurately model their downside protection.

Full Ratchet in Action

A Full Ratchet trigger disregards the volume of the new round and focuses entirely on the price floor. If your original conversion price was £1.00 and a new investor enters at £0.50, your conversion price immediately resets to £0.50. This creates an immediate jump in share count. For an investor holding 1,000,000 preferred shares, the conversion right moves from 1,000,000 ordinary shares to 2,000,000 ordinary shares. The size of the down round doesn’t matter; even a minor issuance at the lower price triggers the full reset.

This “reset” effect has a profound psychological impact on the founding team. In our £50 million to £30 million valuation drop scenario, a Full Ratchet treats the original investment as if it always occurred at the lower price. While this secures your capital value, it can decimate founder ownership. This often leads to a “death spiral” where the team loses the financial incentive to continue growing the business. Professional investors typically use the Full Ratchet as a high-leverage tool only in the most distressed scenarios.

Strategic Implications for Sophisticated Investors

Strategic investors view anti-dilution not merely as a shield but as a lever for governance and capital allocation. While the technical mechanics provide security, over-aggressive application can render a company “uninvestable” for subsequent rounds. If a cap table is heavily skewed toward preferred shareholders through aggressive ratchets, new institutional capital will likely demand a recapitalization before committing funds. With anti-dilution provisions explained as a mathematical necessity, you must balance these protections against the long-term viability of the business. A “death spiral” occurs when aggressive clauses demotivate the team, leading to a collapse in operational value that no amount of equity protection can offset.

Negotiation often involves trading the strength of these provisions for other rights. You might accept a Broad-Based Weighted Average in exchange for a 2x liquidation preference or enhanced veto rights on future debt issuance. These trade-offs are standard when you how to find investors or vet opportunities through professional networks. A sophisticated approach prioritizes a healthy capital structure that remains attractive to top-tier funds. You should focus on terms that protect your capital without stifling the company’s ability to raise the next $100M+ “mega-deal.”

The “Pay-to-Play” Provision

A “Pay-to-Play” clause is a strategic tool used by companies to ensure capital injection during liquidity crunches. It stipulates that an investor must participate in a down round to maintain their anti-dilution protection. If you don’t contribute your pro-rata share, your preferred stock may automatically convert to ordinary stock. This strips away your price protection and liquidation preferences. This forces a binary strategic choice: double down on the position to preserve rights or accept significant dilution. It’s a mechanism designed to eliminate “passive” investors during challenging cycles.

Impact on Employee Stock Option Pools

Anti-dilution adjustments primarily impact the common share pool, which includes the Employee Stock Option Pool (ESOP). When an investor’s conversion ratio increases, the relative value of employee options decreases. This creates a high risk of talent flight. Sophisticated investors often negotiate for an “ESOP top-up” alongside anti-dilution adjustments. This ensures the management team remains incentivized to drive the company toward an exit. Maintaining a motivated workforce is essential for protecting the underlying value of your investment post-correction. If you’re evaluating complex term sheets, you can access our exclusive business listings to identify companies with professional-grade governance structures.

Navigating Deal Terms in the Pre-IPO Landscape

Late-stage private equity requires a shift in defensive strategy as companies approach the public markets. While early-stage protections focus on survival through subsequent venture rounds, pre-IPO terms are designed to bridge the gap between private valuations and public market reality. Investors in this space face the specific risk of a “down-IPO,” where the initial offering price falls below the valuation of the final private funding round. Having anti-dilution provisions explained in this context involves moving beyond standard weighted averages and into the territory of structured guarantees and price-protection mechanisms that trigger upon listing.

The IPO Ratchet: A Late-Stage Speciality

The IPO ratchet is a specialized provision that protects late-stage investors against public market volatility. Unlike standard price-based adjustments, an IPO ratchet often guarantees a specific return on investment (ROI) or a minimum share count upon the company’s debut. If the IPO price does not meet a predetermined threshold, the company must issue additional shares to the protected investors to ensure their equity value matches the agreed-upon floor. IPO ratchets are common in “Unicorn” level pre-IPO deals. These clauses provide a safety net for capital providers entering at peak valuations, ensuring they aren’t disadvantaged by the technical pricing shifts that often occur during the transition to public trading.

Accessing Exclusive Opportunities

Securing clean, well-structured deal terms requires access to professional networks that prioritize institutional-grade governance. BGS Capital operates as a specialist conduit, facilitating investor introductions for sophisticated participants who require high-transparency opportunities. By utilizing a network that vets business listings for structural integrity, you can avoid the “toxic” terms that often plague less disciplined deals. Access to these opportunities is restricted to those who meet specific financial or professional qualifications. This gatekeeping ensures that the ecosystem remains exclusive to investors capable of navigating the technicalities of late-stage equity protection.

Before executing any term sheet in 2026, you must conduct a final technical audit. The following three questions are essential for protecting your capital in the current regulatory environment:

- Does the “Outstanding Shares” definition include the entire unallocated option pool? Verify if the Broad-Based formula is truly inclusive to minimize founder washout.

- Is the IPO ratchet structured as a price reset or a guaranteed IRR? Understand whether you’re protected against a simple price drop or if you’re entitled to a specific yield upon listing.

- Are there “Pay-to-Play” requirements attached to the anti-dilution rights? Confirm whether your downside protection is contingent on future capital injections during distressed rounds.

Mastering these anti-dilution provisions explained throughout this guide allows you to negotiate from a position of technical authority. Are you a sophisticated investor looking for vetted opportunities? You must verify your status to access our current business listings and network introductions.

Strategic Equity Protection in Volatile Markets

Mastery of these technicalities ensures your capital remains insulated from the mathematical shifts of a down round. You now understand how Broad-Based Weighted Average formulas preserve founder motivation while Full Ratchet mechanisms provide absolute price protection. These anti-dilution provisions explained in this guide serve as your framework for evaluating complex term sheets and managing risk in the 2026 pre-IPO landscape. Professional investors must prioritize these safeguards to maintain their ownership percentage as companies approach liquidity events.

BGS Capital facilitates introductions between sophisticated investors and companies maintaining institutional-grade deal structures. Our professional network provides a gateway to vetted opportunities where governance and equity protection are strictly enforced. Are you qualified to participate in high-level private equity transactions? Access Exclusive Pre-IPO Investment Opportunities to leverage these insights in your next transaction. Secure your position in the next generation of market leaders today.

Frequently Asked Questions

What is the most common type of anti-dilution provision in the UK?

The broad-based weighted average is the standard for institutional-grade deals in the UK. It offers a balanced adjustment that considers both the price and the volume of the new funding round. Most sophisticated investors prefer this method because it maintains the company’s appeal for future capital injections while providing a reasonable hedge against valuation volatility.

How does a down round trigger anti-dilution clauses?

A down round triggers these clauses when a company issues new equity at a lower price per share than in previous rounds. This discrepancy activates the adjustment mechanism defined within the shareholder agreement. The conversion ratio then shifts to grant existing preferred shareholders additional ordinary shares upon conversion, effectively lowering their average entry price to reflect the new market reality.

Can anti-dilution provisions be waived by investors?

Investors can and do waive these rights during strategic negotiations. This typically occurs during complex recapitalizations or when a new lead investor requires a cleaner cap table as a condition for a major capital injection. A majority vote of the protected class is usually sufficient to execute a waiver that binds all shareholders within that specific class.

Is a Full Ratchet clause considered “market standard” in 2026?

No, the Full Ratchet remains a non-standard, aggressive protection tool. In early 2025, approximately 80% of venture deals utilized weighted average ratchets rather than full ratchets. This trend has continued into 2026, with Full Ratchet provisions largely reserved for highly distressed scenarios or high-risk bridge rounds where investors demand maximum downside protection.

What is the difference between broad-based and narrow-based weighted average?

The difference lies in the definition of the “outstanding shares” variable used in the formula. Broad-based formulas include all common stock equivalents, such as unissued options and warrants. Narrow-based formulas only account for shares currently issued and outstanding. This makes narrow-based adjustments significantly more dilutive for founders and common shareholders because the denominator in the calculation is smaller.

How do anti-dilution provisions affect the company’s cap table?

These provisions reallocate equity ownership from common shareholders to preferred shareholders following a down round. When the conversion price is adjusted downward, the preferred class becomes entitled to a higher volume of ordinary shares upon conversion. This effectively increases the investor’s percentage of the company while diluting the holdings of the founding team and the employee option pool.

Are anti-dilution clauses the same as pre-emption rights?

No, they are distinct contractual rights. Pre-emption rights grant you the opportunity to maintain your ownership percentage by purchasing new shares in a subsequent round. In contrast, anti-dilution provisions adjust the value or share count of your existing holdings without requiring a new capital injection. Having anti-dilution provisions explained in this manner highlights the difference between a right to invest and a right to price protection.

Do ordinary shareholders benefit from anti-dilution provisions?

Ordinary shareholders almost never benefit from these protections. Anti-dilution clauses are specific to preferred share classes typically held by venture capitalists and sophisticated private investors. When these provisions activate, the resulting adjustment usually dilutes the ordinary share pool. This means that founders and employees often see their ownership percentages decrease to satisfy the contractual requirements of the preferred investors.