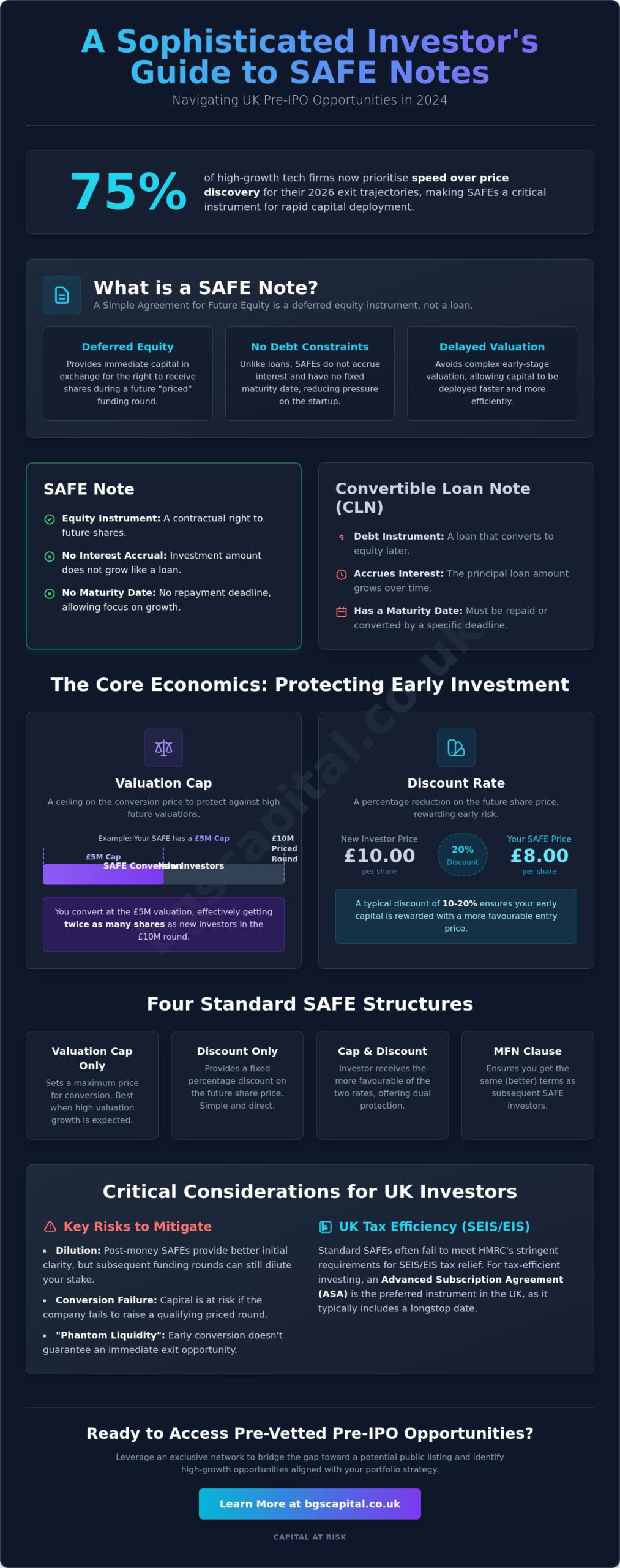

According to 2024 industry benchmarks, approximately 75% of high-growth tech firms prioritising 2026 exit trajectories now favour speed over immediate price discovery. For the sophisticated individual, understanding what is a safe note investment is now a prerequisite for accessing high-tier deal flow without the friction of complex equity negotiations. You’re likely aware that pinning a precise value on a pre-revenue company is often an exercise in speculation that delays capital deployment. CAPITAL AT RISK.

This guide provides a technical breakdown of the Simple Agreement for Future Equity (SAFE) within the UK regulatory framework. It’s designed to help you master the mechanics of valuation caps and discount rates while evaluating how these instruments compare to traditional Convertible Loan Notes (CLNs). We’ll also address critical concerns regarding HMRC tax treatment and potential dilution risks. You’ll gain the specific knowledge required to determine if a SAFE aligns with your portfolio strategy and how to identify these exclusive pre-IPO opportunities.

Key Takeaways

- Define what is a safe note investment as a deferred equity instrument and understand its role in securing future shares without debt-related constraints like interest or maturity dates.

- Master the mechanics of valuation caps and discount rates to ensure your entry price effectively rewards the early-stage risk of pre-IPO ventures.

- Navigate the UK legal landscape by distinguishing between standard SAFEs and tax-efficient Advanced Subscription Agreements (ASAs) for SEIS and EIS compliance.

- Assess the critical risks of dilution and “phantom liquidity” that sophisticated investors must mitigate when committing capital to high-risk instruments.

- Discover how to leverage an exclusive network to access pre-vetted pre-IPO opportunities and bridge the gap toward a potential public listing.

Defining the SAFE Note Investment in 2026

A Simple Agreement for Future Equity (SAFE) serves as a streamlined vehicle for capital injection into high-growth companies. For sophisticated investors, understanding what is a safe note investment requires a shift from traditional debt-based logic. It isn’t a loan. It’s a deferred equity instrument. The investor provides immediate capital in exchange for the right to receive shares during a future “priced” funding round. Unlike Convertible Loan Notes (CLNs), SAFEs don’t accrue interest and lack a fixed maturity date. This structure eliminates the pressure of repayment deadlines while allowing the company to focus on scaling before setting a formal valuation.

The primary objective of this instrument is to delay the valuation process. By deferring the valuation until a qualifying event occurs, both the founder and the investor avoid the complexities of pricing a company that may still be in the pre-revenue or early-growth phase. In the current UK market, this efficiency is a prerequisite for rapid capital deployment.

The Evolution from Y Combinator to Global Standard

Y Combinator introduced the SAFE in 2013 to replace complex debt instruments that often bogged down early-stage deals. By 2026, the UK market has adopted this model for more than just seed rounds. It’s now a standard for pre-IPO bridge rounds where speed is critical. A significant shift occurred with the transition from “Pre-money” to “Post-money” SAFEs. The post-money version provides investors with immediate clarity on their ownership percentage before new capital enters the round. This transparency is vital for wealth managers and high-net-worth individuals managing diversified portfolios.

The Core Mechanism: Capital for Future Equity

An investor holding a SAFE is not a shareholder at the time of the transaction. They don’t have voting rights or dividend entitlements initially. These rights only materialise during a “Trigger Event,” typically a Series A or a qualifying financing round of at least £1,000,000. A SAFE note is a contractual right to future equity, not a debt obligation. This distinction is critical for tax planning and risk assessment. When asking what is a safe note investment, one must recognise that capital is at risk until the conversion event occurs.

The 2026 market operates using four standard SAFE structures:

- Valuation Cap only: Sets a maximum price at which the investment converts into shares, protecting the investor against high future valuations.

- Discount only: Provides a percentage reduction, often 20%, on the future share price compared to new investors.

- Valuation Cap and Discount: The investor receives the more favourable of the two rates during conversion.

- Most Favoured Nation (MFN): Ensures the investor receives the same terms as subsequent SAFE holders if those terms are more advantageous.

Understanding the Economics: Valuation Caps and Discount Rates

The economic value of what is a safe note investment depends on two primary levers: the valuation cap and the discount rate. These mechanisms ensure that early capital is compensated for the high risk associated with seed-stage ventures. Sophisticated investors must model these variables to understand their potential equity stake upon conversion, particularly during high-growth phases where valuations can shift rapidly between rounds.

The Valuation Cap: A Ceiling for Investor Protection

The valuation cap is a ceiling that sets the maximum price at which a SAFE will convert into equity. For example, if an investor enters at a £5m cap and the startup raises its next priced round at a £10m valuation, the SAFE holder converts their investment at the £5m limit. This effectively grants them twice as many shares for the same amount of capital compared to new participants. Post-money caps have become the standard in the UK market because they offer immediate clarity on ownership percentages before the next round occurs. This transparency prevents early backers from being priced out when a company’s valuation exceeds expectations. For a detailed SAFE Note definition and calculation, investors should review the specific mechanics of how these caps impact the price per share relative to the total capital raised.

The Discount Rate: Rewarding the Early Mover

In the 2026 UK venture market, discount rates typically range between 10% and 20%. This rate applies if the company’s valuation at the next round is lower than the valuation cap. It serves as a straightforward percentage reduction on the price paid by new investors. If the new round prices shares at £1.00, a 20% discount allows the SAFE holder to purchase those same shares at £0.80. The “lower of the two” rule is a standard provision in these agreements. It ensures the investor always receives the most favourable conversion price, whether that is driven by the valuation cap or the discount rate. This dual protection is essential when determining what is a safe note investment in a volatile economic climate.

The “Most Favoured Nation” (MFN) clause acts as an additional safeguard for early backers. If the company later issues SAFEs to other investors with more advantageous terms, such as a lower valuation cap, the MFN clause allows the original investor to adopt those better terms. This prevents early supporters from being disadvantaged by subsequent fundraising efforts. Sophisticated individuals looking to expand their portfolio should check their eligibility for current opportunities within our network.

SAFE Notes in the UK: Legal Nuances and Tax Efficiency

Sophisticated investors must understand that the standard US-style SAFE note investment often fails to meet UK regulatory standards. Specifically, these instruments frequently violate the “Risk to Capital” test required by HMRC for tax-advantaged schemes. If an investment carries any right to repayment, it is classified as debt. This classification prevents investors from accessing valuable tax reliefs that are critical to the risk-reward profile of early-stage ventures.

SAFE vs. Advanced Subscription Agreements (ASA)

Advanced Subscription Agreements (ASAs) function as the UK-optimised version of the SAFE note. While they share the goal of deferring valuation until a later funding round, their legal structures differ significantly. An ASA is purely an equity instrument. It cannot be refunded or treated as a loan. It must convert into shares within a specific timeframe, usually 6 to 12 months. Sophisticated individuals should refer to the EIS guide to see how ASAs fit into a diversified portfolio.

- No Repayment: ASAs do not allow for the original capital to be returned as cash.

- Mandatory Conversion: The agreement must lead to share issuance, ensuring the capital remains at risk.

- Long-stop Dates: These dates trigger automatic conversion if no funding round occurs.

Navigating SEIS and EIS Eligibility

When considering what is a safe note investment in the UK, the focus must be on SEIS and EIS compliance. HMRC requires that the investment is “Equity-only” from the outset. Any inclusion of a “maturity date” similar to a convertible loan note will disqualify the transaction from tax relief. Under HMRC guidelines, the capital must convert into shares within six months to guarantee eligibility for the Enterprise Investment Scheme.

Tax relief can significantly offset the “Capital at Risk” nature of these deals. For example, SEIS provides up to 50% income tax relief, while EIS offers 30%. These incentives are designed to encourage investment in high-growth, high-risk startups. However, a generic SAFE note without UK-specific modifications will likely result in the total loss of these benefits. Investors must distinguish between a generic SAFE and a UK-compliant ASA to protect their tax position. Compliance is not optional; it is a prerequisite for professional participation in the UK startup ecosystem.

The distinction between a loan and an equity subscription is absolute. If the contract allows the investor to demand their money back, it is a loan. HMRC will not grant SEIS or EIS relief on loans. Sophisticated investors ensure their contracts use specific “Equity-only” language to avoid this trap. Always verify that the long-stop date is set within the 6-month window to remain compliant with current HMRC interpretations.

Strategic Risks and Dilution: Evaluation for HNWIs

Dilution math presents another strategic challenge. Startups often “stack” multiple SAFE rounds before a Series A. For example, a company might raise £250,000 on a £5 million cap, then another £500,000 on a £10 million cap six months later. These layers of unpriced equity create a “dilution overhang.” When the priced round finally occurs, the cumulative impact can significantly reduce your ownership percentage. During this pre-conversion phase, you hold no voting rights and aren’t entitled to dividends. You’re a contract holder, not a shareholder.

Sophisticated investors need to understand what is a safe note investment in the context of their broader portfolio. It’s a bet on a future valuation event that may never happen. Without a maturity date, the founder has little pressure to trigger the conversion that grants you formal equity rights.

The Pro-Rata Trap and Investor Rights

Standard SAFE templates often exclude pro-rata rights. This means you don’t have the automatic right to participate in future rounds to maintain your ownership percentage. HNWIs should negotiate for side letters that include information rights and pro-rata participation. Without these, your stake can be diluted to insignificance by later-stage venture capital firms. Additionally, the “Liquidation Preference” only becomes relevant once the SAFE converts into preferred stock. Until that conversion, your legal standing is limited to the terms of the specific agreement.

Scenario Analysis: Liquidation vs. Dissolution

The outcome for your capital depends heavily on how the company exits. If a trade sale occurs before the next funding round, most SAFEs allow the investor to either receive their original investment back or convert the note into common stock at the valuation cap to participate in the proceeds. However, in a dissolution or “wind-down” scenario, SAFE holders are typically paid after secured creditors but before common shareholders. If the company’s assets are negligible, the recovery rate is often zero. Understanding where these instruments sit in the Startup Funding stages is vital for risk mapping.

Check your eligibility for exclusive investment access.

Navigating Pre-IPO Opportunities via SAFE Notes

Pre-IPO companies utilize SAFEs to secure bridge financing during the critical 12 to 24 months preceding a public listing. This capital often funds the final scaling phase or covers the significant administrative costs associated with an IPO on the London Stock Exchange or AIM. For those evaluating what is a safe note investment in this context, it represents a strategic entry point into high-growth firms before they reach the public markets. It’s a method to capture equity at a predetermined discount, providing a potential valuation advantage when the conversion event occurs.

Identifying High-Growth Potential

Successful investment requires identifying specific performance markers. Look for companies showing consistent revenue growth, often exceeding 40% year-on-year, within sectors benefiting from structural tailwinds like fintech or renewable energy. The management team’s history of scaling and exiting businesses is a primary indicator of future success. Founders interested in the mechanics of these raises should consult our guide on how to find investors to understand the rigorous standards sophisticated capital requires.

The BGS Capital Introduction Process

BGS Capital operates as a specialist introducer, connecting sophisticated capital with pre-vetted opportunities. Our database features companies seeking capital through SAFE or Advance Subscription Agreement (ASA) instruments. We don’t facilitate raises directly; instead, we provide the conduit for direct engagement with firm leadership. This process ensures transparency and allows for comprehensive due diligence before any commitment of funds.

Access to these opportunities is strictly limited to individuals who meet the UK financial promotions criteria. You must qualify as either a Certified Sophisticated Investor or a High Net Worth Individual (HNWI). This gatekeeping function ensures compliance with regulatory standards and confirms that participants understand the risks associated with illiquid, early-stage equity.

CAPITAL AT RISK. Investments in pre-IPO companies via SAFE notes are speculative. There’s no guarantee that a liquidity event will occur or that the shares will retain their value. Diversification is essential. If you meet the eligibility criteria, the next step is to register and verify your status. Once confirmed, you can begin reviewing current opportunities and connecting with Investor Relations teams to feature your capital in the UK’s next generation of high-growth firms.

- Review the “Am I Eligible?” criteria immediately.

- Access the database of pre-vetted SAFE and ASA opportunities.

- Connect directly with company directors for deep-dive due diligence.

- Monitor sector-specific tailwinds to align your portfolio with growth trends.

Strategic Capital Deployment in the 2026 Venture Landscape

As the venture market evolves into 2026, sophisticated investors must prioritise structural precision over simple capital allocation. Understanding what is a safe note investment involves more than just recognizing its speed; it’s a technical evaluation of valuation caps and discount rates to prevent future dilution during Series A rounds. In the UK, strict adherence to HMRC guidelines is vital. Data from the 2024 Venture Capital Trust statistics highlights that tax efficiency remains a primary driver for HNWIs, yet poorly drafted SAFEs can disqualify investors from EIS benefits. It’s essential to ensure every instrument aligns with current regulatory frameworks to protect long term yields.

BGS Capital operates as a specialist introducer for high-net-worth and sophisticated individuals. We provide access to a curated database of pre-IPO and IPO investment opportunities, ensuring our network stays ahead of significant market shifts. For qualified investors, we facilitate direct introductions to Investor Relations teams to streamline the due diligence process. Remember that your capital is at risk, and professional qualification is mandatory for access to these exclusive tiers.

Am I Eligible? Check your status to access pre-IPO opportunities.

Securing a position in high-growth companies starts with verifying your status today.

Frequently Asked Questions

Is a SAFE note considered debt or equity?

A SAFE note isn’t debt or equity at the point of issuance. It’s a deferred equity instrument that grants the investor a right to future shares. Unlike a loan, it doesn’t carry a repayment obligation or accrue interest. It only converts into equity during a qualifying event, such as a priced funding round.

What happens to a SAFE note if the company fails?

If a company enters liquidation, SAFE holders are typically paid after secured creditors but before common shareholders. You’d receive your original investment back only if assets remain after all senior liabilities are settled. CAPITAL AT RISK: In the majority of startup insolvencies, SAFE investors lose 100% of their capital.

Can I get SEIS or EIS relief on a SAFE note investment?

You can’t usually claim SEIS or EIS tax relief on a standard SAFE note. HMRC rules require shares to be issued at the time of investment to qualify for these incentives. Because a SAFE is a promise of future shares rather than an immediate purchase, it fails the strict eligibility criteria set out in the Income Tax Act 2007.

What is the difference between a SAFE and a Convertible Loan Note?

The main difference is that a SAFE isn’t a debt instrument. A Convertible Loan Note (CLN) has a maturity date and an interest rate, often between 4% and 10% per annum. A SAFE has neither. This makes the SAFE a simpler, more flexible option for founders who want to avoid the threat of a repayment deadline.

Do SAFE notes have a maturity date or interest rate?

No, SAFE notes don’t carry maturity dates or interest rates. This is the primary reason they’re popular with early-stage firms. While a CLN might require repayment after 18 or 24 months, a SAFE stays on the books indefinitely until a conversion trigger occurs. This removes the risk of a technical default for the business.

How is the share price calculated when a SAFE note converts?

The share price is determined by applying either the valuation cap or the discount rate to the price of the new round. You’ll always convert at the lower of the two prices. For example, if your what is a safe note investment has a £4 million cap and the next round is at £8 million, you’ll receive shares at half the price of new investors.

Are SAFE notes only for early-stage startups or can pre-IPO firms use them?

SAFE notes are almost exclusively used by early-stage startups. Pre-IPO firms with established revenues prefer priced rounds because their valuation is easier to verify. Data shows that 95% of SAFE transactions occur during seed or pre-seed stages. Sophisticated investors in later rounds usually demand the transparency of a fully priced equity structure.

What are the risks of a valuation cap being too high?

A high valuation cap risks significant dilution of your potential stake. If the cap is set at £15 million but the company only achieves a £7 million valuation in its next round, the cap provides no protection. You’ll convert at the same price as the new investors, minus any agreed discount, despite taking on more risk at an earlier stage.