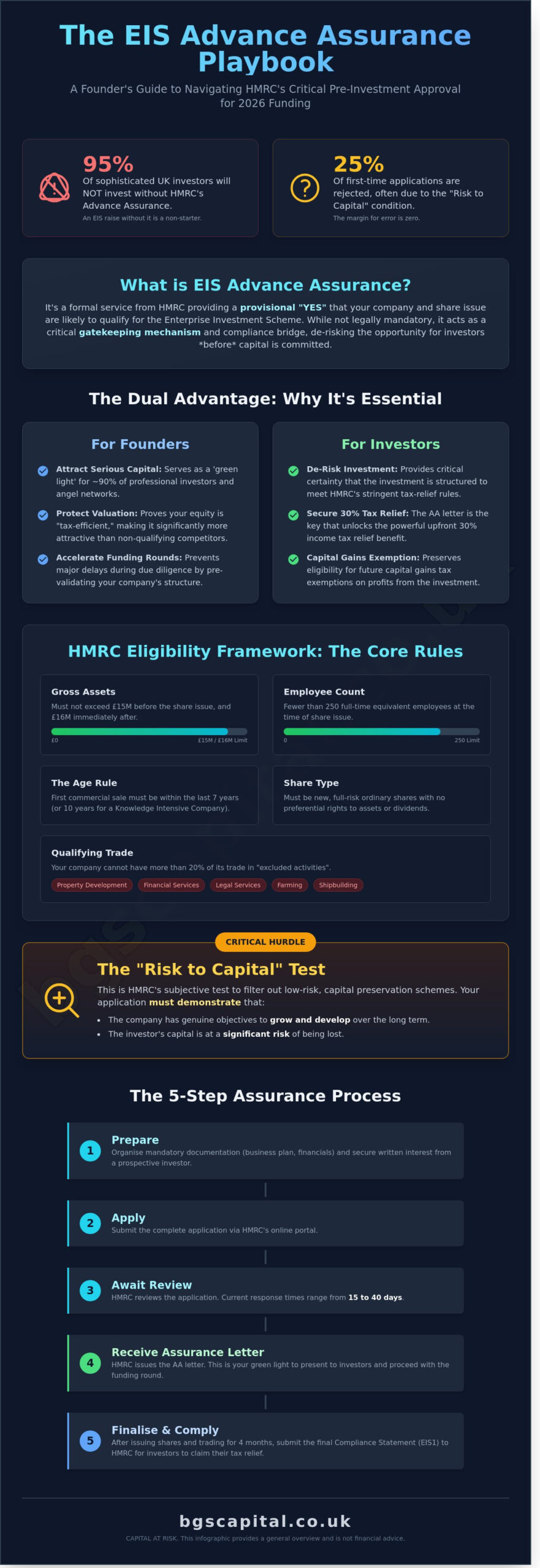

An Enterprise Investment Scheme (EIS) raise without formal HMRC confirmation isn’t just a risk; it’s a non-starter for 95% of sophisticated British investors. You’re likely aware that the EIS advance assurance process is now the industry standard for verifying tax eligibility before a single pound is committed. No confirmation; no investment. The administrative burden is increasing. With HMRC’s “Risk to Capital” condition contributing to rejections for 25% of first-time applicants, the margin for error has disappeared.

Securing your assurance letter shouldn’t be a 12-week guessing game that stalls your growth. This guide provides the technical framework to de-risk your 2026 funding round and satisfy high-net-worth individuals. We’ll examine specific documentation requirements, current 15-day to 40-day response timelines, and the precise wording needed to clear the “Risk to Capital” hurdle. We also address the mandatory evidence for “relevant investments” to ensure your application meets the 2026 compliance threshold. You’ll gain the clarity required to secure your EIS status and close your round with confidence. CAPITAL AT RISK.

Key Takeaways

- Secure HMRC’s provisional confirmation to de-risk your investment round for high-net-worth individuals and sophisticated British investors.

- Identify the stringent eligibility requirements for “Qualifying Companies” and “Full-risk” ordinary shares to ensure compliance for the 2026 tax year.

- Navigate the subjective “Risk to Capital” test by demonstrating genuine long-term growth objectives over simple capital preservation schemes.

- Master the EIS advance assurance process by organising mandatory documentation and securing the required prospective investor interest before submission.

- Discover how to leverage your Advance Assurance status on investor introduction platforms to attract sophisticated capital and professional wealth managers.

What is the EIS Advance Assurance Process and Why is it Essential in 2026?

The EIS advance assurance process is a formal service provided by HM Revenue & Customs (HMRC) that offers a provisional opinion on whether a proposed share issue will qualify for tax relief. It isn’t a legal requirement, yet it functions as a critical gatekeeping mechanism in the UK venture capital ecosystem. By submitting specific details about your business model and investment structure, HMRC confirms if your company meets the strict criteria of the Enterprise Investment Scheme (EIS). This confirmation is vital because it provides a layer of certainty before any capital changes hands.

For high net worth individuals and sophisticated investors, Advance Assurance (AA) is the primary tool for de-risking an entry into early-stage equities. Without it, an investor risks losing the 30% upfront income tax relief and the subsequent capital gains tax exemptions. The AA letter serves as a compliance bridge; it’s the preliminary "yes" from HMRC that precedes the final Compliance Statement (form EIS1), which you can only submit after shares have been issued and the company has traded for four months.

2026 stands as a pivotal year for the UK investment landscape. Following the government’s decision in the 2023 Autumn Statement to extend the EIS sunset clause to April 2035, the 2026 period represents the first full cycle of the renewed scheme. This extension has stabilised the market, but it has also led to more rigorous scrutiny of "capital-at-risk" requirements. Investors in 2026 are prioritising regulatory certainty more than in previous decades.

The Strategic Advantage for UK Founders

Securing AA functions as a green light during the due diligence phase. Data from UK business angel networks suggests that approximately 90% of professional investors refuse to review a pitch deck unless the EIS advance assurance process is already complete. It validates your company’s structure and prevents delays during a funding round. Having this letter in your data room can protect your valuation; it proves your opportunity is “tax-efficient,” making your equity significantly more attractive than a non-qualifying competitor.

Who Can Apply: Eligibility Boundaries

- Gross Assets: Your company’s assets must not exceed £15 million before the share issue and £16 million immediately after.

- Employee Count: You must have fewer than 250 full-time equivalent employees at the time of the share issue.

- The 7-Year Rule: Usually, your first commercial sale must have occurred within the last 7 years. Exceptions exist for “Knowledge Intensive Companies” (KICs), where the limit extends to 10 years.

- Excluded Activities: You won’t qualify if more than 20% of your trade involves “non-qualifying” activities. This includes property development, financial services, legal services, and shipbuilding.

HMRC requires a “relevant person” to have a UK permanent establishment to facilitate the claim. If your firm operates as a group, these limits apply to the entire consolidated entity. Accessing the scheme requires a clear “risk to capital” demonstration, showing the company intends to grow and develop its trade over the long term.

The Eligibility Framework: Meeting HMRC’s Stringent Criteria

HMRC’s criteria for the 2026 tax year remain exceptionally rigid. To qualify, your company must have gross assets under £15 million before the share issue and fewer than 250 full-time equivalent employees. The EIS advance assurance process requires clear evidence that the company is unquoted and operates a “qualifying trade.” While most sectors are eligible, HMRC excludes “excluded activities” such as financial services, property development, and farming. If more than 20% of your trade involves these activities, your application will likely face rejection.

The shares issued must be “full-risk” ordinary shares. They cannot carry preferential rights to the company’s assets or dividends. If an investor receives a fixed dividend or priority over other shareholders during a liquidation event, HMRC will disqualify the entire round. The shares must be paid for in cash, up-front, and cannot be part of any reciprocal arrangement. CAPITAL AT RISK is the fundamental principle here; if the investor’s downside is protected by anything other than the company’s performance, the relief is void.

The “Qualifying Purpose” test is the most subjective hurdle in the application. You’ve got to prove the investment will be used for the long-term growth and development of the trade. This isn’t a box-ticking exercise. You must submit a detailed business plan and financial forecasts through HMRC’s online application portal that demonstrates a genuine risk to the investor’s capital. HMRC looks for a two-part test: the company must have objectives to grow and develop over the long term, and there must be a significant risk that the investor will lose more capital than they gain.

Independence is equally vital. Your company can’t be a 51% subsidiary of another entity, nor can it be controlled by another company. This independence must be maintained throughout the three-year “relevant period.” If there are “arrangements” in place for another company to take control, even if they haven’t been triggered yet, the assurance will be denied.

The Knowledge-Intensive Company (KIC) Advantage

KIC status offers significant flexibility for high-growth tech and life-science firms. It increases the annual fundraising limit from £5 million to £10 million, with a lifetime cap of £20 million. To qualify, your company must meet the “operating costs” test, proving that R&D spending accounted for at least 10% of total operating costs in one of the three years preceding the EIS advance assurance process application. KIC status also extends the age limit for the initial investment from 7 years to 10 years. You can check your company’s eligibility for these higher limits before starting the formal submission.

The “No Pre-arranged Exit” Rule

HMRC rejects applications where shareholder agreements or side letters imply a guaranteed exit. If your articles of association include mandatory redemption clauses or specific “put options” that allow investors to force a buy-back, you’ll fail the compliance check. Avoid complex “liquidation preference” language that guarantees a specific multiple return before other shareholders. Stick to standard 1x non-participating preferences. HMRC’s specialist venture capital unit scrutinises these documents for any language that suggests the investment is a loan in disguise rather than true equity.

The “Risk to Capital” Test: Why Applications Fail

The Risk to Capital condition is the most subjective hurdle in the EIS advance assurance process. HMRC introduced this test to disqualify “capital preservation” schemes where the tax relief, rather than commercial growth, provides the primary return. It’s a gatekeeping mechanism designed to ensure that CAPITAL AT RISK remains the fundamental principle of the Enterprise Investment Scheme. If an inspector decides your company’s structure prioritises the protection of investor funds over genuine commercial expansion, they’ll issue a rejection without hesitation.

The test consists of two distinct parts. First, the company must have objectives to grow and develop its trade in the long term. Second, there must be a significant risk that the investor will lose more capital than they could ever gain in net return, excluding tax reliefs. HMRC identifies “artificial” structures by looking for pre-arranged exit strategies or complex share classes that insulate investors from downside. The Risk to Capital test serves as the primary filter for HMRC’s 2026 compliance team to ensure only high-growth, high-risk ventures access tax relief.

Common Red Flags in Business Plans

HMRC inspectors are trained to spot business models that lack internal substance. A major red flag is an over-reliance on subcontracting. If 70% of your raised capital is diverted to a single third-party provider to deliver the core service, HMRC will argue you aren’t building internal value or intellectual property. They want to see that the company is hiring staff and creating an enduring corporate structure.

Low-risk business models that resemble asset-backed financing are also frequently targeted. If 80% of the company’s value is tied up in tangible assets like property, plant, or equipment, the investment doesn’t meet the spirit of venture capital. Your 3-5 year financial projections must demonstrate a clear “path to scale” where the investment leads to a 3x or 5x increase in turnover. Applications often fail when projections show slow, incremental growth that doesn’t justify the high-risk nature of the scheme.

Recent Trends in HMRC Rejections

Data from the 2025-2026 tax year shows a 15% increase in rejections based on the “Capital at Risk” emphasis. Inspectors now look beyond the numbers to the “Investor IRR” narrative in your application cover letter. You must explicitly state why the investment is risky and why the company couldn’t secure traditional bank debt. You should review the official HMRC advance assurance application guidelines to ensure your narrative aligns with current regulatory expectations.

To satisfy skeptical inspectors, you must provide evidence of “genuine commercial trade” through tangible documentation. Don’t rely on vague promises of future contracts. Provide signed Letters of Intent (LOIs), detailed market research, or evidence of a pilot programme. In 2025, approximately 22% of initial applications were delayed because they failed to prove that the trade was truly “new” or “innovative” under the latest HMRC definitions. Providing a detailed breakdown of how the £150,000 or £5 million will be deployed across specific growth activities is no longer optional; it’s a requirement for success.

Note: Access to EIS tax reliefs is restricted to qualified companies and investors. Always check your status before proceeding: Am I Eligible?

Step-by-Step: Navigating the HMRC Online Application

Completing the EIS advance assurance process requires precision. You must access the HMRC digital portal via a Government Gateway ID. The system is designed to filter out speculative applications. You cannot simply “test the waters” anymore. Since the 2018 Finance Act, HMRC mandates that you provide the names and addresses of prospective investors. These individuals or funds must have expressed a genuine interest in your current round. Applications submitted without named investors are typically rejected immediately.

The HMRC digital portal for venture capital schemes is a structured environment. You’ll need to upload several core documents to avoid a “Request for Further Information” (RFI). These include your latest business plan, three-year financial forecasts, and your current Articles of Association. Ensure your forecasts include a clear breakdown of how you intend to spend the investment. HMRC looks for “growth and development” spend. This means your capital must be used to increase turnover or headcount. It cannot simply pay off existing debt.

Before you hit submit, verify your documentation is organised. HMRC officials often handle dozens of cases simultaneously. A poorly structured application leads to delays. If you haven’t received a response within the standard 8-week Service Level Agreement (SLA), you should contact the Venture Capital Schemes (VCS) team. Note that 92% of applications are processed within this window; however, seasonal peaks can extend wait times.

If your application is complex, the digital portal allows for additional supporting evidence. This is where you include patent filings or commercial contracts that prove your market traction. Transparency is your greatest asset during this stage. Any ambiguity regarding your company structure or share classes will trigger an enquiry.

Preparing the Perfect Cover Letter

The cover letter is the most critical part of the EIS advance assurance process. It’s your opportunity to address the “Risk to Capital” condition directly. You must prove that your company is a genuine trading entity with a significant risk of loss for the investor. Don’t use marketing fluff. Stick to the facts. Disclose all previous funding rounds, including SEIS or VCT involvement. These figures impact your £12 million lifetime limit. If you’re claiming Knowledge Intensive Company (KIC) status, highlight it here. KICs enjoy higher lifetime limits of £20 million and extended age limits for their first commercial sale.

Post-Submission: Handling HMRC Enquiries

HMRC typically responds with either an approval or an RFI. If you receive an RFI, you usually have 15 business days to provide the requested data. Common enquiries focus on “disqualifying arrangements” or complex share rights. You might need professional tax advice if HMRC challenges your business model’s eligibility. This is common in sectors like property development or financial services where “excluded activities” are a risk.

A successful application results in a “Comfort Letter.” This document states that HMRC is satisfied that the proposed investment will qualify for relief based on the information provided. It’s not a legal guarantee. If your circumstances change between the assurance and the share issue, the relief may still be denied. The letter is an opinion based on the facts you disclosed. It’s valid as long as those facts remain true when the shares are issued. Always keep a copy of this letter for your investor data room. CAPITAL AT RISK.

Leveraging Advance Assurance to Secure Sophisticated Capital

Securing HMRC’s formal opinion through the EIS advance assurance process acts as a critical catalyst for fundraising. It transforms a speculative venture into a de-risked proposition for capital providers. Wealth managers and High-Net-Worth Individuals (HNWIs) often mandate this status before they even begin the due diligence process. Without it, your business is often invisible to the UK’s most active private equity networks. You should display your AA letter prominently on investor introduction platforms. When you list your opportunity, lead with your tax-efficient status to filter for investors specifically seeking UK tax-advantaged schemes.

Your pitch deck requires a dedicated slide for EIS eligibility. It’s not enough to mention it in the appendix. State clearly that the 30% upfront income tax relief is available for qualifying individuals. This incentive reduces an investor’s effective cost of entry. For example, a £100,000 investment effectively costs the investor £70,000 once the relief is applied. For a sophisticated portfolio, this 30% buffer serves as a vital hedge against the inherent risks of early-stage equity. Ensure your investor relations communications provide a clear timeline for when they can expect their EIS3 certificates.

Targeting Sophisticated Investors

Sophisticated investors prioritise EIS-eligible opportunities to achieve aggressive portfolio diversification. The psychological impact of the 30% upfront income tax relief is a primary driver for decision-making. It provides an immediate “return” on capital before the company reaches its first operational milestone. Wealth managers use these incentives to balance high-risk allocations across their client bases. By choosing to feature your business on BGS Capital to reach our network of sophisticated investors, you connect with a demographic specifically looking for pre-vetted EIS opportunities. This targeted approach ensures your outreach isn’t wasted on retail investors who lack the capital or the “sophisticated” status required for these raises.

Maintaining Compliance Post-Investment

Closing the investment round is just the start of your compliance journey. While the EIS advance assurance process confirms eligibility in principle, the actual tax relief is only triggered after the share issue. You must submit the EIS1 Compliance Statement to HMRC. This can only happen once you’ve traded for at least four months or spent at least 70% of the investment amount. Once HMRC accepts the EIS1, they issue a compliance certificate and a claim form (EIS3) for you to distribute to your investors. Investors cannot claim their 30% relief without this document.

The 3-year “holding period” rule is a non-negotiable requirement for maintaining relief. If an investor sells their shares within three years of the issue date, HMRC will claw back the tax relief. You must also remain vigilant against “disqualifying events.” These include changing your business trade to an excluded activity or being acquired by another company within the three-year window. Losing EIS status post-investment is catastrophic for investor relations. It often triggers “bad leaver” clauses or legal disputes if the loss of status resulted from management negligence. Your focus must remain on protecting your investors’ tax position as much as growing the business.

- Ensure all share certificates are issued within the timeframe specified in your AA.

- Monitor the “gross assets” test to ensure you don’t exceed the £15 million limit before the shares are issued.

- Provide regular updates to your wealth managers regarding compliance milestones.

Maintaining a compliant environment ensures your business remains attractive for future funding rounds. Sophisticated investors are more likely to provide follow-on capital if their initial tax relief remains secure and the administrative side of the investment is handled with professional precision.

Secure Your 2026 Growth Capital

Successfully navigating the EIS advance assurance process remains the most significant hurdle for UK companies targeting high-growth trajectories in 2026. HMRC’s stringent “Risk to Capital” test results in approximately 25% of applications failing at the first instance, often because firms don’t provide sufficient evidence of long-term scaling objectives. For companies seeking to attract sophisticated capital, this assurance isn’t a luxury; it’s a prerequisite. High Net Worth individuals and accredited investment firms rarely consider unassured rounds in the current regulatory climate.

BGS Capital acts as a specialist introducer, providing direct introductions to an exclusive network of HNW and sophisticated investors. We specialise in pre-IPO and high-growth UK capital raises, ensuring that qualified businesses gain visibility among accredited investment firms and wealth managers. Our network consists of professional investors who understand the complexities of tax-efficient schemes and are actively seeking robust opportunities. It’s time to validate your business model and position your company for a successful raise. CAPITAL AT RISK.

Am I Eligible? Feature your business and connect with sophisticated investors today.

Frequently Asked Questions

How long does the EIS advance assurance process typically take in 2026?

The EIS advance assurance process typically takes between 15 and 45 working days in 2026. HMRC’s Venture Capital Schemes team currently processes 85% of applications within this window. You should submit your documentation at least 8 weeks before your planned funding round. Delays often occur if the tax inspector requires additional clarification on your “risk to capital” status.

Can I apply for EIS advance assurance without having any investors lined up?

You can’t apply for advance assurance without identifying at least one prospective investor. HMRC updated its guidelines in 2018 to require the names and addresses of individuals or funds considering the investment. You don’t need a signed contract at this stage. However, you must provide evidence of serious intent, such as a signed term sheet or formal correspondence from a wealth manager.

What happens if HMRC rejects my application for advance assurance?

If HMRC rejects your application, they’ll issue a formal letter explaining why your company doesn’t meet the compliance criteria. You can’t technically appeal this decision because advance assurance is a non-statutory service. Instead, you must address the specific failures mentioned, such as the age of the trade or the “risk to capital” test, and submit a revised application. 12% of initial applications require these amendments.

Is there a fee to apply for EIS advance assurance from HMRC?

There is no fee to apply for EIS advance assurance from HMRC. The government provides this service free of charge to support the growth of UK startups. While the application itself costs nothing, most companies budget between £2,000 and £5,000 for professional tax advisors. These specialists ensure the 25 page submission is accurate, which reduces the risk of a time consuming rejection.

What is the difference between SEIS and EIS advance assurance?

The primary difference involves the investment limits and the age of your business. SEIS is for companies less than 3 years old raising up to £250,000, whereas the EIS advance assurance process applies to companies up to 7 years old raising up to £5 million annually. SEIS offers investors 50% tax relief, while EIS provides 30%. You can apply for both simultaneously using a single HMRC application form.

Can I raise money before I receive my advance assurance letter?

You can raise money before receiving the letter, but it’s commercially risky for your shareholders. Most sophisticated investors won’t transfer funds until they see the HMRC confirmation. If you issue shares and HMRC later decides your company is ineligible, the investors lose their 30% tax relief entirely. 90% of professional investment rounds are contingent upon the receipt of this assurance letter.

Do I need a new advance assurance for every funding round?

You should apply for a new advance assurance for every distinct funding round you undertake. HMRC’s approval is specific to the share issue and business circumstances described in your original application. If your business model or share structure has changed since your last raise 12 months ago, the previous letter is void. Keeping your assurance status current is vital for maintaining investor confidence and regulatory compliance.

Does advance assurance guarantee that my investors will get their tax relief?

Advance assurance doesn’t guarantee tax relief for your investors. It’s a provisional opinion based on the facts you provide. Relief is only confirmed after you issue the shares and submit form EIS1. CAPITAL AT RISK; if your company fails to follow the scheme’s rules for 3 years after the investment, HMRC will claw back the tax relief from your shareholders. You must remain a qualifying company throughout this period.