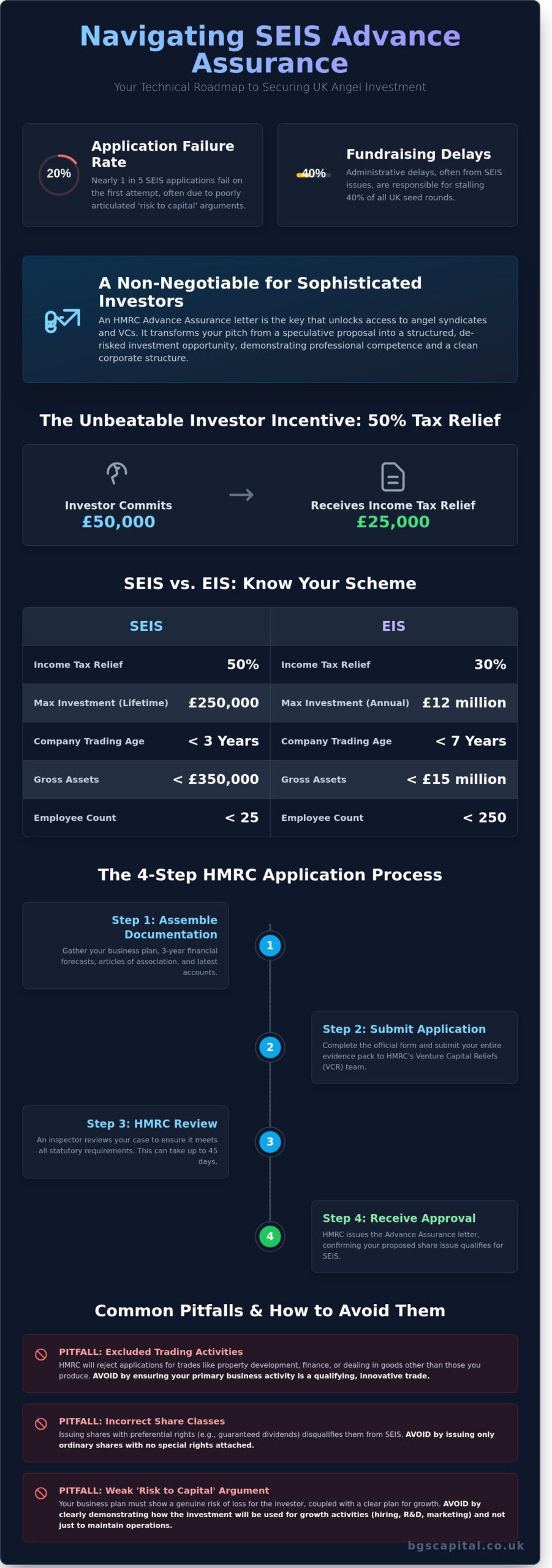

Why would a sophisticated investor commit £150,000 to your early-stage venture without a formal guarantee from HMRC? For most high-net-worth individuals, the absence of an approval letter is an immediate deal-breaker. Our SEIS advance assurance guide provides the technical roadmap required to navigate these stringent regulatory hurdles. HMRC data from the 2023/24 period indicates that nearly 20% of applications fail to secure approval on the first attempt, often due to poorly articulated ‘risk to capital’ arguments. You can’t afford to be part of that statistic when your funding round is on the line.

You likely already know that securing Seed Enterprise Investment Scheme (SEIS) status is the most effective way to de-risk your proposition for UK investors. This guide promises to deconstruct the 2026 compliance requirements, ensuring you master the complexities of the application and avoid the administrative delays that stall 40% of seed rounds. We’ll provide a step-by-step breakdown of the process, from gathering essential governing documents to receiving your final HMRC approval letter.

Key Takeaways

- Understand why HMRC provisional confirmation is a non-negotiable requirement for securing angel interest in the 2026 UK startup ecosystem.

- Navigate the HMRC application process using this SEIS advance assurance guide to correctly draft ‘Risk to Capital’ statements and essential financial forecasts.

- Identify common pitfalls, including excluded trading activities and share class errors, to prevent formal application rejection and delays.

- Leverage SEIS status to enhance investor appeal by clearly communicating tax relief benefits to high net worth individuals and sophisticated investors.

- Transition from SEIS readiness to active fundraising by featuring your business to BGS Capital’s network of accredited investment firms and wealth managers.

What is SEIS Advance Assurance and Why is it Non-Negotiable in 2026?

Advance Assurance (AA) is the formal, provisional confirmation from HM Revenue & Customs (HMRC) that a company’s proposed share issue meets the statutory requirements of the Seed Enterprise Investment Scheme (SEIS). It’s not a legal guarantee, but it functions as a critical validation of your company’s structure and trade. In 2026, the UK startup ecosystem is defined by heightened risk aversion. This SEIS advance assurance guide highlights that obtaining this letter is the first milestone of any serious seed-stage raise. Without it, you aren’t just missing a tax break; you’re effectively locked out of the sophisticated investor market.

Sophisticated investors and angel syndicates rarely commit capital without seeing the HMRC approval letter first. Capital is expensive in 2026, and investors demand certainty. The AA letter provides that certainty by confirming that the company is a qualifying entity and the shares are eligible for relief. It eliminates the administrative anxiety that often stalls early-stage deals. If you don’t have your AA in place, you’re asking an investor to take a 100% risk on your business while also taking a 100% risk on the tax treatment. Most won’t do it.

The Core Benefits for Your Fundraising Strategy

Securing AA transforms your pitch from a speculative proposal into a structured investment opportunity. The primary draw is the 50% income tax relief available to UK taxpayers. If an individual invests £50,000, they can immediately reduce their tax bill by £25,000. This massive downside protection is the most effective tool in your arsenal. Beyond the tax math, holding an AA letter signals professional competence. It shows venture capital networks that your cap table and corporate structure are clean and “investment ready.” It significantly shortens the due diligence process for accredited investment firms. They can skip the basic eligibility checks and focus entirely on your commercial traction and unit economics.

SEIS vs. EIS: Determining Your Eligibility

Understanding the boundaries between Seed and Enterprise schemes is vital for your application. The SEIS limit currently stands at £250,000, a figure updated in April 2023 to support early-stage growth. To qualify for this “Seed” status, your company must have been trading for less than 3 years. There are strict ceilings on your internal resources: your gross assets must be under £350,000 and your total employee count must be fewer than 25 full-time equivalents.

- The 3-Year Rule: Your clock starts from the date of your first commercial sale, not your incorporation date.

- Gross Asset Cap: This includes all cash in the bank and physical assets before liabilities are deducted.

- Simultaneous Applications: Many founders apply for both SEIS and EIS assurance at the same time. This is standard practice if you intend to raise more than £250,000 in a single round.

If your company exceeds any of these thresholds, you must pivot your strategy toward the Enterprise Investment Scheme (EIS), which offers 30% relief but allows for much larger raises. Using this SEIS advance assurance guide as your starting point ensures you don’t waste months pursuing the wrong scheme. Accuracy at this stage prevents HMRC rejections that can take up to 45 days to resolve, potentially causing you to miss your funding window.

The HMRC Application Process: A Step-by-Step Technical Guide

Applying for Seed Enterprise Investment Scheme (SEIS) status requires technical precision. HMRC scrutinises every detail of your submission to ensure compliance with the Income Tax Act 2007. This SEIS advance assurance guide outlines the specific requirements for a successful application. You must submit your application before you issue any shares. Failure to do so disqualifies the investment from tax relief immediately, regardless of the company’s merit.

Essential Documentation Checklist

The Venture Capital Reliefs (VCR) team requires a comprehensive evidence pack. Your pitch deck must be the current version shown to potential investors. It should clearly outline the commercial proposition and the market opportunity you’ve identified. Financial projections must cover at least three years. These forecasts need to demonstrate a genuine intention to grow the trade. HMRC expects to see a headcount increase or a significant rise in turnover. You also need to identify potential investors. HMRC mandates that you provide names and addresses for individuals planning to invest at least 30% of the total raise. This requirement prevents speculative applications from businesses that haven’t begun their fundraising efforts. For full details on the submission portal, refer to HMRC’s official advance assurance application guide.

You must also include the latest Articles of Association and any shareholder agreements. HMRC checks these for “disqualifying arrangements” or “preferential rights” that might violate the risk criteria. If your articles provide investors with a guaranteed exit or priority on assets during liquidation, the application will likely fail. Every document must reflect a standard commercial arrangement without artificial protections for the investor’s capital.

Navigating the ‘Risk to Capital’ Condition

The ‘Risk to Capital’ condition, introduced in April 2018, is the most common point of failure for UK startups. An inspector must be satisfied that the company has long-term objectives to grow and develop. There must be a significant risk that the investor will lose more capital than they gain as a net return. You must avoid the capital preservation trap. This occurs when a business model is structured to protect the investor’s initial outlay through asset-backing or guaranteed income streams. If your company looks like a special purpose vehicle for a single project, expect a rejection.

To pass this subjective test, prove that the capital will be used for high-risk, high-growth activity. You’ll need to demonstrate that the company is taking on genuine commercial risk to enter new markets or develop new products. If you’re unsure about your company’s eligibility, you can check your status before starting the formal process.

Submission occurs primarily through the online G-form. You’ll need your company’s Unique Taxpayer Reference (UTR) and registered office details. While postal routes exist, they’re significantly slower and prone to administrative delays. Current HMRC response times fluctuate between 15 and 45 working days. Don’t believe myths about expediting an application. HMRC doesn’t fast-track submissions because a funding round is closing or a legal deadline is looming. They process applications in the order they arrive. Precise preparation is the only way to avoid delays caused by “further information requests” (FIRs). If an inspector asks for clarification, your timeline essentially resets as you move to the back of the queue.

Why HMRC Says No: Common Pitfalls and How to Avoid Them

HMRC rejected approximately 1,240 advance assurance applications across all venture capital schemes in the 2022-23 tax year. These rejections rarely stem from a lack of innovation. Instead, they’re the result of technical non-compliance or structural errors that trigger an immediate red flag. Using a comprehensive SEIS advance assurance guide helps founders identify these risks before they become permanent stains on a company’s funding record.

Identifying Non-Qualifying Trades

The “Excluded Activities” list is the primary filter HMRC uses to disqualify applicants. If your company operates in banking, insurance, money lending, or property development, you’re ineligible. This restriction extends to legal and accounting services, farming, and even certain types of hotels or nursing homes. The 20% rule is the critical threshold here. HMRC allows “incidental” excluded activity, provided it doesn’t exceed 20% of your company’s total trade, assets, or expenses. If 21% of your revenue originates from leasing equipment, your entire SEIS status is compromised.

For 2026, Fintech and Proptech founders must exercise extreme caution. HMRC has increased its scrutiny of platforms that might be perceived as providing a “financial service” rather than a technology solution. If your software facilitates trades or manages client funds directly, you must prove the trade isn’t “dealing in financial instruments.” Before submitting documents via HMRC’s official SEIS advance assurance application portal, ensure your business plan explicitly defines your revenue streams to avoid being categorised as an excluded trade.

Structural Red Flags in Your Governing Documents

Inconsistencies between your Articles of Association and your investment deck lead to 15% of all SEIS delays. HMRC requires absolute alignment. If your business plan suggests a rapid pivot into property investment but your Articles claim you’re a SaaS provider, the Inspector will reject the application for lack of clarity. Your governing documents must also confirm that all SEIS shares are issued for cash and are fully paid up at the time of issue. HMRC won’t accept “sweat equity” or shares issued in exchange for services.

Structural complications often arise from:

- Alphabet Shares: Creating Class A, Class B, and Class C shares often triggers an enquiry. If one class has a preferential right to dividends or assets during a winding-up, the shares don’t qualify. SEIS shares must be “ordinary” and non-redeemable.

- Pre-existing Agreements: Shareholders’ agreements that guarantee a return or offer “downside protection” invalidate the risk-to-capital requirement. If an investor’s risk is mitigated by a side deal, SEIS is void.

- The Subsidiary Trap: If your company owns more than 50% of another entity, that subsidiary must also be a “qualifying” company. Complex group structures with dormant or non-trading subsidiaries often lead to immediate rejection.

This SEIS advance assurance guide emphasises that simplicity is your greatest asset. HMRC prefers clean cap tables and straightforward Articles. If your structure includes “liquidation preferences” that favour certain investors over others, you’ve likely failed the “no preferential rights” test. Every share must carry the same risk. If it doesn’t, the tax relief won’t be granted. Verify that your cap table reflects 100% ordinary shares before proceeding with your application.

Maximising Investor Appeal: Using Advance Assurance to Close Your Round

Securing HMRC approval transforms your pitch from a speculative proposal into a de-risked financial product. When you feature your business on a BGS Capital business profile, you should lead with your AA status. It signals to our network of wealth managers and sophisticated investors that the preliminary tax due diligence is complete. Investors don’t want to fund a company only to discover later that a technicality in the Articles of Association disqualifies them from relief.

Founders should adopt a ‘SEIS First’ strategy for their cap table. This involves allocating the first £250,000 of any raise specifically to SEIS-eligible investors before moving to EIS or standard equity. This prioritises the most tax-efficient capital. Since the 2023/24 tax year, the SEIS limit increased from £150,000 to £250,000; this 66% increase provides a larger window to attract early-stage backers with 50% income tax relief. This SEIS advance assurance guide highlights that timing is everything. Closing the SEIS portion of your round quickly creates momentum for the remainder of the raise.

The three-year holding rule serves as a functional tool for long-term alignment. Investors must retain their shares for at least 36 months to keep their tax benefits. This requirement filters out ‘flippers’ and ensures your early backers are committed to the business’s growth trajectory. It creates a stable shareholder base during the critical early stages of scaling. CAPITAL AT RISK.

The Sophisticated Investor’s Perspective

Private wealth managers view Advance Assurance as a regulatory safety net. It mitigates the risk of HMRC rejecting a claim after the capital is deployed. For High Net Worth (HNW) individuals, the Capital Gains Tax (CGT) reinvestment relief is often the primary driver. Reinvesting a gain from another asset into an SEIS-qualified company can exempt 50% of that gain from CGT. Additionally, loss relief acts as a vital downside protection narrative. If the venture fails, a 45% taxpayer can reduce their total loss to just 27.5p for every £1 invested. This makes the risk-reward ratio far more palatable for diversified portfolios.

Post-Approval Logistics: From AA to Compliance Certificates

Advance Assurance is the promise; the SEIS1 compliance statement is the delivery. You cannot submit the SEIS1 form until you’ve traded for at least four months or spent 70% of the funds raised. Once HMRC processes the SEIS1, they issue a unique claim code. You then issue SEIS3 certificates to your investors. These documents are what allow them to actually claim their relief on their self-assessment tax returns. Maintaining compliance is mandatory. Avoid ‘disqualifying events’ such as changing the nature of your trade or exceeding the £350,000 gross asset limit within the first three years. Failure to do so will result in HMRC clawing back the tax relief from your investors.

Ready to showcase your investment opportunity to a network of qualified investors? Feature your business with BGS Capital to connect with sophisticated capital providers.

Next Steps: Feature Your Business and Connect with Capital

Securing HMRC approval is a critical milestone for any UK startup. It transforms your proposition from a high-risk concept into a tax-efficient opportunity for sophisticated investors. This SEIS advance assurance guide has detailed the technical requirements. Now, the focus shifts to the commercial application of that status. Once your letter is in hand, you’ve removed a primary barrier to entry for early-stage capital. Sophisticated investors rarely consider seed-stage deals without this certification in place.

BGS Capital functions as a strategic bridge. We don’t provide tax advice or legal structuring. Instead, we operate as a specialist introducer. We connect companies that have completed their SEIS readiness with a network of high-net-worth individuals and wealth managers. In April 2023, the SEIS investment limit for companies increased from £150,000 to £250,000. This change made early rounds more substantial and competitive. Reaching the right audience with speed is now the priority for founders.

Leveraging the BGS Capital Network

Obtaining your Advance Assurance (AA) allows your business to be featured on our platform. This provides direct visibility to our investor relations teams. They manage a curated database of pre-IPO and early-stage opportunities. Qualified companies benefit from a streamlined introduction process. We ensure your documentation reaches individuals who understand the specific risk profile of the SEIS scheme. This isn’t a broad marketing exercise; it’s a targeted placement within a professional financial ecosystem.

- Direct exposure to accredited investment firms and family offices.

- Inclusion in a database used by wealth managers for secondary placings.

- Access to a network looking for pre-IPO opportunities with defined tax incentives.

- Efficient distribution of your pitch deck to verified, sophisticated investors.

Am I Eligible? The Qualification Gate

Not every business with Advance Assurance meets the criteria for our network. We maintain a strict qualification gate to ensure the quality of opportunities presented to our investors. You must demonstrate a clear path to growth and a robust business model beyond just tax eligibility. We act as a facilitator, not a financial advisor. We don’t manage funds or execute trades. Our role is to identify and introduce high-potential firms to the right capital sources. Following this SEIS advance assurance guide ensures you have the necessary documentation to pass the initial stage of our review.

If your company has secured its AA and you’re ready to scale, the next step is a formal assessment. We look for transparency and readiness. Our network expects professional-grade pitch decks and clear financial projections. If you meet these standards, you can RAISING CAPITAL? FEATURE YOUR BUSINESS by applying through our portal. We review applications based on sector, growth potential, and compliance status.

CAPITAL AT RISK

Investment in early-stage companies involves significant risks, including loss of capital, illiquidity, and lack of dividends. The tax treatments mentioned depend on individual circumstances and may change in the future. Professional guidance is essential before proceeding with any raise or investment. BGS Capital does not provide investment advice or recommendations. All users must perform their own due diligence or seek independent financial advice from an authorised professional. We operate strictly as an introducer and do not facilitate the underlying transactions.

Maximise Your 2026 Funding Potential

HMRC’s 2026 standards for SEIS are rigorous. This SEIS advance assurance guide clarifies that securing your confirmation isn’t just a tick-box exercise; it’s a strategic asset. Data indicates that UK startups with advance assurance close rounds 30% faster than those without it. You’ve seen the technical pitfalls to avoid, particularly regarding the “risk to capital” condition and the strict 2-year trading window. Precision in your application prevents the typical 45-day delay caused by HMRC follow-up queries.

Once your compliance is established, the next stage is connecting with the right liquidity. BGS Capital serves as a professional and compliant gateway to capital. We operate as a specialist introducer for pre-IPO and IPO opportunities. Our platform connects qualified businesses with a curated network of HNW and sophisticated investors who prioritise SEIS-eligible ventures. It’s time to leverage your tax-efficient status to secure the growth capital your business requires.

RAISING CAPITAL? FEATURE YOUR BUSINESS

Your 2026 roadmap is clear.

Frequently Asked Questions

Is SEIS Advance Assurance legally mandatory for a funding round?

No, it’s not a legal requirement under the Income Tax Act 2007. However, 95% of sophisticated investors and venture capital firms require it before committing capital to a seed-stage business. It acts as a formal provisional confirmation from HMRC that the company and the share issue meet statutory requirements. Without it, you’ll likely fail to secure investment from high net worth individuals seeking tax efficiency.

How long does HMRC take to process an SEIS Advance Assurance application in 2026?

HMRC typically processes applications within 15 to 45 working days. While the 2026 service standard remains 8 weeks, most well-prepared submissions receive a response in under 30 days. You should ensure your SEIS advance assurance guide checklist is complete to avoid delays. Incomplete documentation can extend this timeline by an additional 20 days if HMRC requests further clarification.

Can I apply for SEIS Advance Assurance if I have already started trading?

Yes, you can apply if your company has been trading for less than 3 years. The Seed Enterprise Investment Scheme is specifically designed for companies in their first 36 months of active trade. If your first commercial sale occurred more than 3 years ago, you’re ineligible. You must also ensure your gross assets don’t exceed £350,000 at the time of the share issue.

What happens if my SEIS Advance Assurance application is rejected?

HMRC provides a specific reason for the rejection, allowing you to appeal or resubmit with amended terms. In 2024, common rejection reasons included failing the “risk to capital” gateway or having disqualifying share structures. You have 30 days to appeal a formal decision. Alternatively, you can restructure the investment terms to address HMRC’s concerns and submit a fresh application for review.

Can I change my business plan after receiving Advance Assurance?

Minor operational adjustments are acceptable, but material changes to the company’s trade or share structure invalidate the assurance. If you pivot to a “non-qualifying” activity, such as property development or financial services, the prior assurance becomes void. You must notify HMRC if the nature of the business changes significantly before the shares are issued to ensure your compliance remains intact.

Do I need to have investors lined up before I apply for AA?

Yes, you must provide the names and addresses of at least one prospective investor. HMRC updated its guidelines in 2018 to prevent speculative applications. You don’t need a full cap table, but you must demonstrate a genuine commercial intention to raise capital. This requirement ensures that HMRC resources are focused on active funding rounds rather than hypothetical scenarios. Am I eligible? Check your investor list first.

How much does it cost to apply for SEIS Advance Assurance?

HMRC doesn’t charge a fee for processing an Advance Assurance application. It’s a free service provided to facilitate investment in UK startups. However, most companies spend between £1,500 and £5,000 on professional fees for accountants or specialist consultants. These experts ensure the application adheres to the strict “risk to capital” requirements and follows a comprehensive SEIS advance assurance guide.

Does receiving Advance Assurance guarantee that investors will get their tax relief?

No, it’s a provisional opinion based on the information provided at the time of application. Final tax relief depends on the company maintaining its qualifying status for at least 3 years following the investment. Investors only claim relief after the company submits form SEIS1 and receives SEIS3 certificates. CAPITAL AT RISK; tax treatments depend on individual circumstances and may change over the investment period.