Can a single sentence in your legal documentation strip you of 80% of your vested equity? In the 2024 UK venture landscape, sophisticated founders know that a headline valuation is merely a distraction if the underlying clauses are predatory. You’ve likely felt the pressure to sign quickly to maintain momentum, but protecting your stake requires a clinical approach to the fine print. This term sheet negotiation checklist uk is designed to help you navigate these complexities while maintaining the professional standing required to close with top-tier firms.

It’s possible to secure the capital you need without losing control of your board or your vision. You’ll gain the specific knowledge needed to counter aggressive liquidation preferences and restrictive leaver provisions that often surprise founders during an exit. This guide previews the five most critical negotiation pillars, from drag-along rights to anti-dilution triggers, ensuring you move from offer to completion with total clarity and institutional alignment.

Key Takeaways

- Distinguish between non-binding commercial summaries and the legally binding obligations that govern exclusivity and confidentiality.

- Protect your equity by understanding how pre-money valuations and the “Option Pool shuffle” directly impact founder dilution.

- Maintain operational control by strategically negotiating board composition and the specific list of actions requiring investor approval.

- Use this professional term sheet negotiation checklist uk to ensure SEIS/EIS tax efficiency and cap potential warranty liabilities.

- Access a network of sophisticated investors through BGS Capital to ensure your funding round is supported by qualified, high-level partners.

Understanding the UK Term Sheet: Binding vs Non-Binding Elements

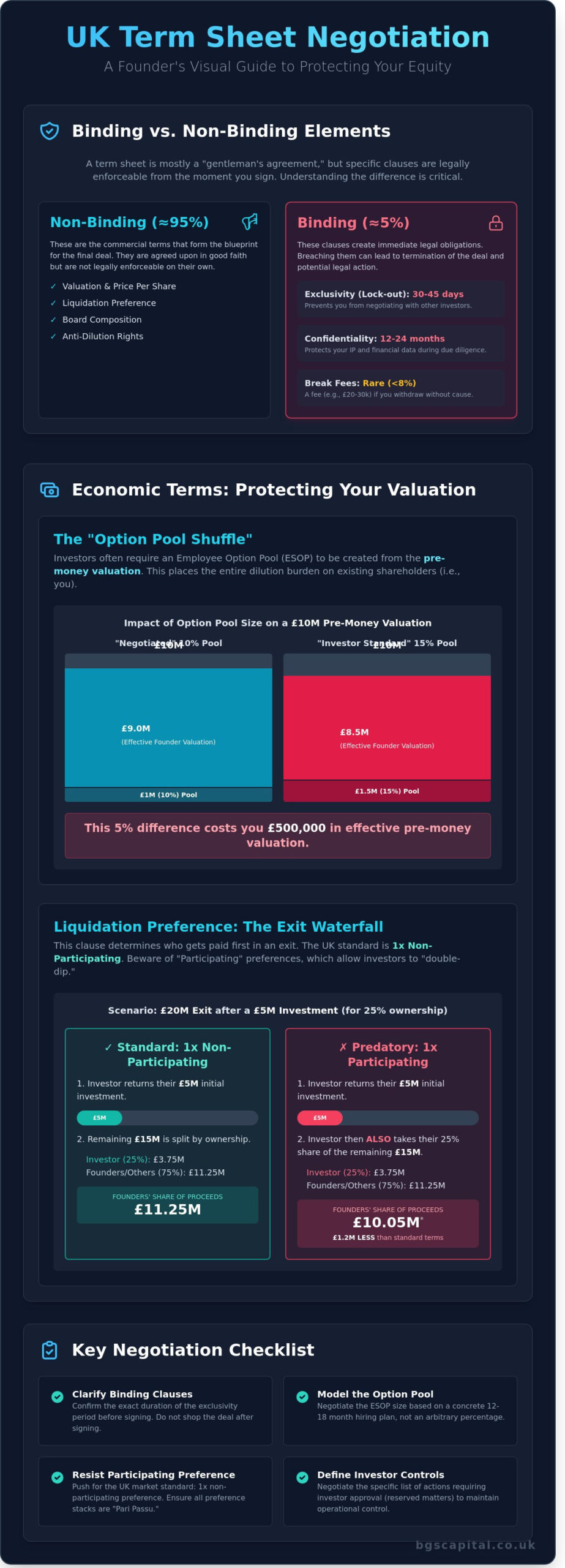

A term sheet is a non-binding summary of the principal terms of a proposed investment. It acts as the foundational blueprint for the definitive legal documents that follow. While approximately 95% of the document is not legally binding, specific clauses create immediate and enforceable obligations. Sophisticated founders using a term sheet negotiation checklist uk must distinguish between the commercial roadmap and the legal handcuffs that take effect the moment signatures are exchanged.

The British Private Equity & Venture Capital Association (BVCA) provides the standard framework for most UK venture deals. Adhering to these templates reduces legal friction and accelerates the closing process. However, founders often make the mistake of over-indexing on valuation. Experienced leaders prioritize certainty of funds over the highest headline number. In a volatile market, where 15% to 20% of deals can stall during the documentation phase, a committed investor with a clear track record is more valuable than a high-valuation offer that lacks follow-through. CAPITAL AT RISK is a standard reality in these private equity transactions; therefore, the reliability of the counterparty is paramount.

The Exclusivity Period (Lock-out)

Exclusivity typically lasts between 30 and 45 days in the UK market. This lock-out period prevents you from negotiating with other capital providers while the lead investor finalizes their position. Don’t sign this agreement until the investor completes their preliminary “red flag” due diligence. If you shop the deal after signing, you risk immediate termination and significant reputational damage within the London venture ecosystem. Ensure your term sheet negotiation checklist uk includes a clear expiration date for this period to regain your freedom if the investor stalls.

Confidentiality and Break Fees

Confidentiality clauses protect your sensitive intellectual property and financial projections during the deep-dive due diligence phase. It’s standard practice to ensure this clause survives for at least 12 to 24 months after the term sheet expires or is terminated. Break fees remain rare in UK venture deals, appearing in fewer than 8% of seed and Series A transactions. When they do appear, they are usually capped at a specific figure, such as £20,000 or £30,000, to cover the investor’s legal out-of-pocket expenses if the founder unilaterally withdraws from the deal without cause.

Economic Terms: Protecting Your Equity and Valuation

Economic terms dictate your final proceeds. A robust term sheet negotiation checklist uk must prioritize the math of dilution over the headline valuation figure. Investors focus on their percentage ownership and downside protection; you must focus on the effective price per share after all adjustments.

Valuation Mechanics and the Option Pool

Pre-money valuation is the agreed value before new capital is injected. While the headline number looks attractive, the “option pool shuffle” often hides the true price. Investors typically require an unallocated Employee Stock Option Plan (ESOP) to be carved out of the pre-money valuation. This ensures their stake isn’t diluted by future hires. It places the entire dilution burden on the existing shareholders.

The size of this pool significantly impacts your ownership. If you agree to a 15% pool instead of a 10% pool on a £10 million valuation, you’re effectively lowering your pre-money valuation by £500,000. For a founder holding a 40% stake, this represents a direct hit to your personal equity before the investment even closes. Negotiate the pool size based on a concrete 12 to 18-month hiring plan rather than accepting an arbitrary percentage.

Liquidation Preference and Participation

The UK market standard for 2024 remains a 1x non-participating liquidation preference. This ensures investors get their initial capital back, or their pro-rata share of proceeds, whichever is higher. You should resist “participating preference” terms. These are often viewed as “double-dipping” because they allow investors to take their 1x return and then share in the remaining exit proceeds.

In a £20 million exit where £5 million was invested, a participating preference could cost founders an additional £1.2 million compared to standard non-participating terms. Ensure all preference stacks are “Pari Passu.” This means all investors across different rounds share the same priority level. It prevents later-stage investors from draining the exit pool before early backers and founders receive their share. You can check your eligibility to see how sophisticated networks structure these preferences for growth.

Anti-Dilution Protections

Anti-dilution clauses protect investors during “down rounds” where the company raises capital at a lower valuation than previous rounds. In the UK, the broad-based weighted average is the standard. This formula moderates dilution based on the amount of capital raised at the lower price. Avoid “full ratchet” clauses. A full ratchet reprices the investor’s entire previous stake to the new, lower price, which can aggressively wipe out founder equity during a market correction. Stick to BVCA (British Private Equity & Venture Capital Association) standards to ensure your term sheet negotiation checklist uk remains competitive and fair.

Control and Governance: Who Really Runs the Company?

Equity ownership does not always equate to operational control. In a professional investment context, governance rights allow investors to influence major decisions regardless of their share percentage. Your term sheet negotiation checklist uk should prioritize the balance between founder autonomy and investor oversight to prevent board-level gridlock.

The Board of Directors and Observer Rights

The board is the company’s ultimate decision-making body. For UK Seed and Series A rounds, a “2+1” structure is standard; this consists of two founders and one investor director. As you scale toward Series B, a “3+2” structure often emerges, adding an independent director and a second investor representative.

You must distinguish between a Director and a Board Observer. Directors hold fiduciary duties and voting rights. Observers attend meetings and receive board packs but cannot vote. Limiting the number of observers is vital; having more than two can lead to inefficient meetings and compromised confidentiality. Investor Director Consents shouldn’t apply to routine expenses. Setting a threshold, such as requiring consent only for capital expenditures exceeding £50,000, protects your ability to manage day-to-day operations without constant interference.

Good Leaver vs Bad Leaver Provisions

Vesting protects the company from a founder exiting early with a large portion of the cap table. A standard UK term sheet requires a 4-year vesting period with a 12-month “cliff.” If you leave before the 12-month mark, you forfeit all unvested shares. After the cliff, 25% of your equity vests, with the remainder vesting monthly at a rate of 1/48th.

- Bad Leavers: Usually defined as individuals terminated for gross misconduct, fraud, or those who resign voluntarily within a short period, typically 12 to 24 months. They often lose all unvested shares and may be forced to sell vested shares at a nominal value or the lower of market value and cost.

- Good Leavers: These are founders who leave due to death, permanent ill health, or redundancy. They typically retain their vested shares and may have a portion of unvested shares accelerated depending on the negotiation.

Information rights are another critical component. Sophisticated investors will require monthly management accounts and annual audited financials. Ensure these requirements don’t become an administrative burden. Standard UK practice involves providing unaudited monthly reports within 21 days of month-end. Including these specificities in your term sheet negotiation checklist uk ensures you aren’t blindsided by compliance costs later.

CAPITAL AT RISK. All startup investments carry significant risk. Ensure you consult with a qualified UK legal professional before signing any binding agreements.

The Definitive Term Sheet Negotiation Checklist UK

A term sheet negotiation checklist uk serves as your primary defense against structural risks that could jeopardize your company’s future. Founders must scrutinize every clause to ensure alignment with long-term exit strategies. Start by confirming the drag-along and tag-along thresholds. In the UK market, these typically sit between 50% and 75%. If the threshold is too low, a minority investor might force a sale before you’ve reached your target valuation.

Review the “Conditions Precedent” list immediately. These are the requirements you must satisfy before the funds hit your bank account. Common deal-breakers include failing to secure HMRC advanced assurance or having unresolved intellectual property disputes. If a requirement takes longer than 14 days to resolve, it’ll delay your entire runway extension.

Tax Efficiency: SEIS and EIS Compliance

Sophisticated UK investors prioritize SEIS and EIS advanced assurance. Without this, 85% of angel investors won’t commit capital. You’ve got to ensure your company meets the “Gross Assets” test, which is under £350,000 for SEIS. The “Number of Employees” test is equally vital; you must have fewer than 250 full-time employees for EIS eligibility. Be wary of preference rights. Certain liquidation preferences or redemption rights can disqualify shares from these tax schemes, costing your investors their 30% or 50% tax relief.

Warranties and Disclosure

Founders often overlook the personal financial risk involved in warranties. You’ve got to cap these at the total investment amount or less. The disclosure letter is your legal shield. It lists every specific exception to the warranties you provide. Set a “de minimis” threshold, typically between £5,000 and £15,000. This prevents investors from bringing claims for minor administrative errors. Ensure the “Right of First Refusal” (ROFR) and co-sale rights don’t prevent existing shareholders from participating in future rounds, as this can lead to massive dilution.

Before signing any binding agreements, ensure your company structure meets investor requirements. Am I Eligible?

Verify that the term sheet includes a clear cap on legal fees. In the UK, it’s standard for the startup to pay the investor’s legal costs, but this should be capped at a specific figure, such as £10,000 to £20,000, depending on the round’s complexity. Uncapped fees can quickly erode your starting capital. Always confirm that board observer rights don’t grant voting power, as maintaining board control is essential for early-stage founders.

Connecting with Sophisticated Investors via BGS Capital

The success of your term sheet negotiation checklist uk depends heavily on the counterparty’s sophistication. High-quality investors reduce transaction friction because they’re already aligned with UK market standards, such as the BVCA model documents. BGS Capital functions as a specialist introducer, bridging the gap between qualified companies and a network of high-net-worth individuals, wealth managers, and family offices.

Working with sophisticated capital providers minimizes the risk of “re-trading” terms late in the process. In 2023, data indicated that deals involving accredited investment firms closed 22% faster than those with retail-heavy syndicates. BGS Capital ensures your business is positioned in front of investors who understand complex capital structures and secondary placings. This alignment ensures that the technical points in your term sheet negotiation checklist uk are met with professional scrutiny rather than unnecessary delays.

Feature Your Business for Capital Raising

BGS Capital acts as a strategic introducer for companies seeking pre-IPO and IPO opportunities. We don’t facilitate raises directly; we provide a platform for qualified businesses to gain visibility. To maintain the ecosystem’s integrity, every company must undergo a qualification process before being featured to our network of wealth managers and sophisticated investors. This gatekeeping ensures that the opportunities presented meet the high standards expected by institutional-grade capital.

- Access to a network of 5,000+ sophisticated investors and wealth managers.

- Focus on high-growth sectors and pre-IPO secondary markets.

- Streamlined introduction process to reduce lead-investor search time.

Am I Eligible? Check your eligibility to feature your business here.

Professionalism in the Investment Ecosystem

Capital raising requires a compliant, serious approach. BGS Capital operates strictly as an introducer within the UK financial ecosystem, ensuring that all interactions remain professional and transparent. We prioritize connections with accredited investment firms that take lead roles in funding rounds, providing the necessary price discovery and structural leadership for a successful raise. This professionalism is vital for founders who need to protect their equity while securing growth capital.

CAPITAL AT RISK. Engaging in high-level investment activities involves significant risk. The value of investments can go down as well as up. Founders and investors should seek independent financial advice before committing to any transaction. BGS Capital does not provide investment advice or direct brokerage services.

Strategise Your Next Funding Round

Navigating a seed or Series A round in the UK requires more than just a high valuation. You’ve got to balance binding confidentiality clauses with non-binding economic terms to protect your long-term equity. Sophisticated founders prioritize control rights and board seats to ensure they retain influence as the company scales. Using a comprehensive term sheet negotiation checklist uk helps you track these variables during high-pressure discussions with institutional funds. This determines the balance between a successful exit and the loss of operational control.

BGS Capital provides a professional, risk-aware platform designed for companies ready to accelerate. We offer access to a network of 1,200+ sophisticated investors and have 15 years of combined expertise in pre-IPO and IPO introductions. It’s vital to remember that capital is always at risk. Choosing the right partners is your most important decision this quarter. Our platform functions as a specialist facilitator, connecting qualified companies with high net worth individuals and wealth managers.

RAISING CAPITAL? FEATURE YOUR BUSINESS

Connect with a network that understands the technical complexities of the UK financial ecosystem. Take the next step toward your public listing today.

Frequently Asked Questions

Is a term sheet legally binding in the UK?

A term sheet is generally not legally binding in the UK, except for specific clauses regarding confidentiality, exclusivity, and governing law. These binding provisions typically remain in effect for 30 to 60 days while the parties conduct due diligence. All other commercial terms are marked “Subject to Contract,” meaning they’re indicative and depend on the execution of final long-form documents.

What is a “founder-friendly” term sheet?

A founder-friendly term sheet prioritizes operational autonomy and limits aggressive investor protections. It typically includes a 1x non-participating liquidation preference and utilizes the BVCA model documents, which were updated in 2023 to reflect current market standards. These terms ensure the founding team retains a 15% to 20% option pool without facing excessive interference from the board on daily decisions.

How long does it take to go from term sheet to completion in the UK?

The transition from a signed term sheet to completion usually takes between 4 and 12 weeks. The first 14 days are typically dedicated to financial and commercial due diligence, followed by 30 days of legal drafting. Delays often occur if the term sheet negotiation checklist uk wasn’t finalized early, leading to protracted disputes over the Shareholders’ Agreement or Articles of Association.

Do I need a solicitor to negotiate a term sheet?

You should engage a specialist solicitor before signing a term sheet to avoid committing to unfavorable commercial precedents. Legal fees for a UK Seed round typically range from £5,000 to £15,000 depending on complexity. While founders can handle high-level valuation discussions, a solicitor is required to review technical clauses like drag-along rights and restrictive covenants that impact your long-term control.

What are “Reserved Matters” in a UK investment deal?

Reserved Matters are a specific list of company actions that require prior consent from the investor or a 75% majority of shareholders. These usually include issuing new shares, selling the business, or taking on debt exceeding £50,000. They’re designed to protect the investor’s minority position. It’s vital to ensure these don’t prevent the board from making routine hires or making small operational pivots.

Can an investor withdraw after signing a term sheet?

An investor can withdraw at any point before the final investment agreement is signed because the term sheet isn’t a binding commitment to fund. Market data suggests that approximately 12% of deals fail during the due diligence phase after the term sheet is signed. Reasons for withdrawal include negative findings in the cap table or shifts in the investor’s internal strategy. CAPITAL AT RISK until funds are transferred.

What is the difference between a term sheet and a shareholders’ agreement?

A term sheet is a 3 to 5-page summary of the deal’s key principles, while the Shareholders’ Agreement is the comprehensive 50-page legal contract. The term sheet sets the framework for the investment. The Shareholders’ Agreement contains the granular detail, including warranties and specific governance rights. Using a term sheet negotiation checklist uk ensures that the final agreement doesn’t introduce unexpected or punitive legal requirements.

How much dilution is normal for a Seed round in the UK?

Dilution for a UK Seed round typically falls between 15% and 25% of the company’s post-money equity. According to 2023 market data, the median equity stake surrendered by founders in an initial priced round is 20%. This figure often includes the creation of an Employee Share Option Plan, which usually requires a 10% pool to be carved out before the investment is finalized.