For UK investors seeking to maximise returns from early-stage ventures, understanding the Seed Enterprise Investment Scheme is critical. However, navigating the official HMRC guidance can be a complex undertaking, leading to uncertainty about the real financial benefits and the risk of non-compliance. Many investors struggle to accurately calculate potential savings or confidently compare SEIS against its counterpart, the Enterprise Investment Scheme (EIS).

This guide provides a comprehensive and direct analysis of SEIS tax relief. We will deconstruct the powerful tax incentives available, including the 50% Income Tax relief, Capital Gains Tax exemption, and invaluable Loss Relief. You will gain the clarity required to make informed investment decisions, a functional framework for calculating your potential returns, and a clear understanding of the rules you must follow to remain compliant. The objective is to equip you with the knowledge to strategically leverage SEIS for optimal tax efficiency within your portfolio.

Key Takeaways

- Understand how to reduce your income tax liability by 50% on qualifying investments up to the annual limit of £200,000.

- Learn the distinction between the two types of Capital Gains Tax relief to defer or eliminate tax on capital gains.

- Discover how the full framework of seis tax relief provides a critical safety net by allowing you to offset investment losses against your income.

- Identify the essential compliance document—the SEIS3 certificate—that you must receive from a company before any tax benefits can be claimed.

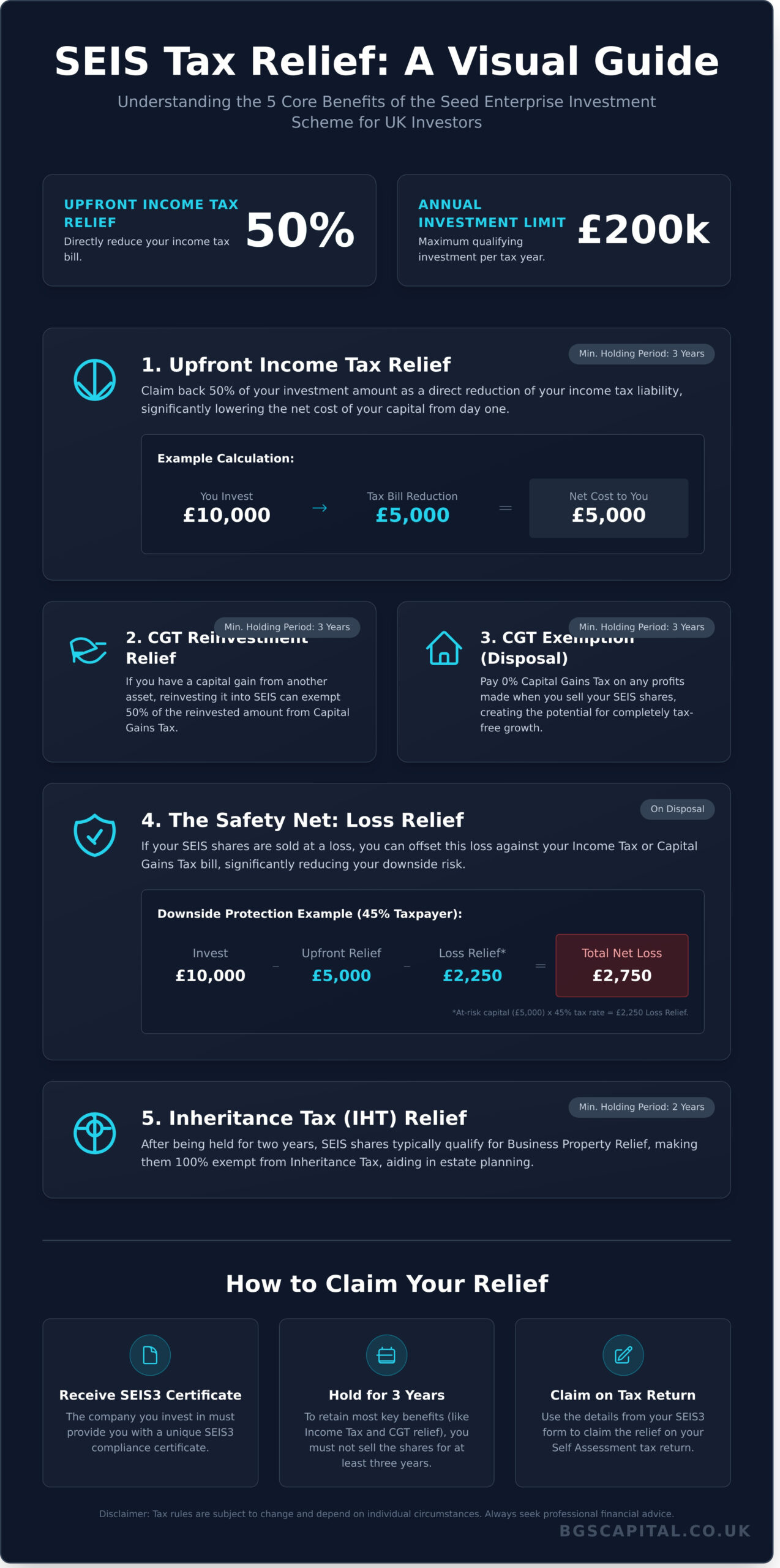

What is SEIS Tax Relief? The Five Core Benefits for Investors

The Seed Enterprise Investment Scheme (SEIS) is a UK government initiative designed to stimulate investment into high-risk, early-stage companies. To offset this risk, the scheme offers a suite of generous tax reliefs, making it one of the most tax-efficient investment vehicles available in the UK. Understanding the five core benefits of seis tax relief is fundamental for any investor considering this asset class. However, all benefits are contingent on the investor and the company meeting specific qualifying criteria and holding periods.

1. Upfront Income Tax Relief

The most immediate benefit is the 50% upfront income tax relief. Investors can claim back half of their investment, up to the annual maximum of £200,000, as a direct reduction of their income tax liability. For example, a £10,000 investment could result in a £5,000 reduction in your tax bill, effectively lowering the net cost of your capital from day one.

2. Capital Gains Tax (CGT) Reinvestment Relief

Investors who have realised a capital gain from selling other assets can benefit from CGT Reinvestment Relief. By reinvesting the gain into SEIS-qualifying shares, you can exempt 50% of that reinvested amount from your Capital Gains Tax bill. This provides a powerful tool for efficient tax planning within a financial year.

3. CGT Exemption (Disposal Relief)

Any profit generated from the sale of your SEIS shares is entirely exempt from Capital Gains Tax. This ‘disposal relief’ creates the potential for completely tax-free growth. To qualify, the shares must be held for a minimum of three years from the date of issue, directly rewarding long-term support of a startup through its critical growth phase.

4. Loss Relief

Given the high-risk nature of early-stage ventures, SEIS provides a crucial safety net. If an investment fails and shares are sold at a loss, you can offset this loss against either your Income Tax or Capital Gains Tax bill. For a higher-rate taxpayer, this relief significantly reduces the net cost of a total loss to a fraction of the initial capital.

| Relief Type | Benefit Summary | Minimum Holding Period |

|---|---|---|

| Income Tax Relief | Reduce your income tax bill by 50% of the amount invested. | 3 Years |

| CGT Reinvestment Relief | Exempt 50% of a separate capital gain when reinvested into SEIS. | 3 Years |

| CGT Exemption | Pay 0% Capital Gains Tax on profits from the sale of SEIS shares. | 3 Years |

| Loss Relief | Offset losses against your Income Tax or Capital Gains Tax bill. | N/A (on disposal) |

| Inheritance Tax (IHT) Relief | Shares are 100% exempt from IHT. | 2 Years |

It is essential to note that accessing these benefits requires strict adherence to HMRC rules. The three-year holding period is critical for most reliefs, and both the investor and the company must maintain their qualifying status. Professional advice should always be sought to ensure the scheme aligns with your individual financial circumstances.

Deep Dive: 50% SEIS Income Tax Relief

The primary incentive of the Seed Enterprise Investment Scheme (SEIS) is the substantial upfront income tax relief it offers. This is not a deferral or a complex deduction; it is a direct reduction of your income tax liability, providing immediate value to your investment portfolio. For sophisticated investors, this feature significantly mitigates the inherent risks of investing in early-stage companies.

Under current HMRC rules, an individual can invest up to a maximum of £200,000 per tax year into SEIS-qualifying companies. This allowance provides the potential for a significant tax reduction, making it one of the most generous tax-efficient investment schemes available in the UK. This powerful tool is designed to encourage investment into the UK’s most innovative startups.

Calculating Your Income Tax Relief

The calculation for seis tax relief is straightforward. The relief is valued at 50% of the cost of the shares you subscribe for. It is crucial to note that you can only claim relief up to the amount of your total income tax liability for the year.

- Investment Amount: £50,000

- Relief Rate: 50%

- Calculation: £50,000 x 50% = £25,000

In this example, the investor would reduce their income tax bill for the relevant tax year by £25,000, provided their liability was at least that amount. If their tax bill was only £20,000, the relief would be capped at £20,000.

Using the ‘Carry Back’ Provision

The SEIS framework includes a ‘carry back’ provision, which adds a layer of strategic flexibility for tax planning. This feature allows you to treat an investment made in the current tax year as if it were made in the preceding tax year. This is particularly useful if you had a higher income tax liability in the previous year or if you have insufficient liability in the current year to make full use of the relief.

To utilise this provision, you must make a specific claim on your Self Assessment tax return. The carry back applies to the entire investment amount; it is not possible to split the relief for a single investment across two tax years.

Understanding the Two Types of SEIS Capital Gains Tax Relief

Beyond the initial income tax reduction, the Seed Enterprise Investment Scheme (SEIS) offers investors two powerful forms of relief against Capital Gains Tax (CGT). It is crucial to distinguish between them, as they serve different purposes within an investment strategy. One mitigates tax on gains from other assets, while the other eliminates tax on the profit from the SEIS investment itself.

Understanding how to leverage both is key to maximising the financial efficiency of your portfolio. These reliefs work independently but can be used in combination for substantial tax advantages.

CGT Reinvestment Relief Explained

Reinvestment Relief is designed to reduce your CGT liability from the disposal of other assets. When you realise a capital gain—for instance, from selling property, art, or shares in a publicly-listed company—you can defer and reduce the tax owed by reinvesting that gain into SEIS-qualifying shares.

- Mechanism: Up to 50% of the amount you reinvest into an SEIS venture is exempt from Capital Gains Tax.

- Example: An investor sells a portfolio of stocks and realises a taxable gain of £80,000. They reinvest the full £80,000 into an SEIS-qualifying company. They can then claim Reinvestment Relief, making 50% of that amount (£40,000) exempt from CGT.

CGT Disposal Relief (Tax-Free Growth)

Disposal Relief is the primary long-term benefit of a successful SEIS investment. It ensures that 100% of the profit you make from selling your SEIS shares is free from Capital Gains Tax, provided certain conditions are met. This is a significant incentive that rewards the high-risk nature of early-stage investing.

- Conditions: To qualify, you must have held the SEIS shares for a minimum of three years and have claimed the initial SEIS Income Tax relief on the investment.

- Example: An investor subscribes for £50,000 of shares in an SEIS startup. After four years, the company is acquired, and their shares are sold for £200,000. The entire £150,000 profit is completely free from CGT.

A Combined Scenario

The true power of SEIS tax relief becomes evident when an investor utilises both CGT reliefs. Consider an investor who sells a second property and realises a £100,000 capital gain. They decide to reinvest this full amount into a qualifying SEIS company. Immediately, they can claim Reinvestment Relief, exempting £50,000 of their property gain from CGT. They also claim the 50% Income Tax relief. After holding the SEIS shares for three years, the investment has grown and is now worth £300,000. Upon selling the shares, the £200,000 profit is entirely exempt from CGT due to Disposal Relief. This strategic use of the scheme addresses both an existing tax liability and a future one.

The Safety Net: Loss Relief and Inheritance Tax Benefits

Investing in early-stage companies carries inherent risk. The UK government acknowledges this through the Seed Enterprise Investment Scheme by providing significant downside protection. While the 50% income tax relief is the primary incentive, the Loss Relief facility is arguably the most critical component for capital preservation, acting as a powerful safety net should an investment fail. This, combined with potential Inheritance Tax advantages, makes the overall seis tax relief structure a highly efficient vehicle for sophisticated investors.

How SEIS Loss Relief Works in Practice

If your SEIS shares are disposed of at a loss (or become worthless), you can elect to offset this loss against either your income tax bill for that year or the previous year, or against your capital gains tax bill. The relief is calculated on your net loss—the amount of capital truly ‘at risk’ after accounting for the initial 50% income tax relief.

Consider this example for an additional rate (45%) taxpayer:

- Initial Investment: £10,000

- Upfront Income Tax Relief (50%): £5,000

- Net Capital at Risk: £5,000

If the company fails and the shares become worthless, the £5,000 at-risk capital can be offset against your income. The Loss Relief would be £5,000 x 45% = £2,250. The total relief received is £5,000 (upfront) + £2,250 (loss relief) = £7,250. Therefore, the actual net loss on the original £10,000 investment is only £2,750.

Inheritance Tax (IHT) Relief

A further significant benefit of the seis tax relief framework is its value in estate planning. SEIS-qualifying shares may also be eligible for Business Property Relief (BPR). Provided the shares have been held for a minimum of two years at the time of death, they can potentially be passed on to beneficiaries completely free from Inheritance Tax. This makes SEIS a valuable tool for individuals structuring their long-term wealth succession. However, estate planning is a complex area, and it is imperative to seek professional advice from a qualified financial or tax advisor.

How to Claim SEIS Relief: Rules and Compliance

Securing the significant tax advantages of the Seed Enterprise Investment Scheme is contingent on a precise and compliant claims process. Both the investor and the investee company must adhere to strict HMRC regulations. Understanding these rules is not merely procedural; it is fundamental to ensuring your relief is granted and, crucially, retained.

The entire process for an investor hinges on receiving a single, critical document from the company in which you have invested. Without it, no claim can be made.

The SEIS3 Certificate: Your Key to Claiming

You cannot initiate a claim for seis tax relief until you have received a SEIS3 compliance certificate from the investee company. The company can only apply to HMRC for these forms after it has been trading for at least four months or has spent 70% of the capital raised. This certificate officially confirms that both the company and your specific share issuance qualify under the scheme’s rules. Once received, you can claim the relief by entering the details on your Self Assessment tax return in the ‘Additional information’ pages (form SA101), under the section for ‘Other tax reliefs’.

Critical Investor Rules to Follow

To successfully claim and retain your tax relief, you as the investor must meet several key qualifying conditions. Failure to comply, particularly within the initial holding period, can result in HMRC withdrawing the relief, requiring you to repay any tax reduction you have received. Adherence is mandatory.

- Minimum Holding Period: You must retain the shares for a minimum of three years from the date of issue. Disposing of them earlier will typically lead to the withdrawal of the tax relief.

- No Employee Relationship: You cannot be a paid employee of the qualifying company at any point during the period from the date of share issue to the third anniversary of that date. Directorships are sometimes permitted, provided they are not accompanied by employment contracts.

- No Substantial Interest: You must not hold more than a 30% stake in the company’s ordinary share capital, voting rights, or assets. This rule applies for a period beginning two years before the share issue and ending three years after.

Navigating these compliance requirements is essential for any serious investor. Find compliant SEIS investment opportunities through our network.

SEIS Tax Relief: A Strategic Advantage for UK Investors

The Seed Enterprise Investment Scheme provides a compelling, government-backed framework designed to de-risk investment in the UK’s most promising early-stage ventures. As this guide has detailed, the core benefits for sophisticated investors are substantial: an immediate 50% income tax reduction on investments up to £200,000 per tax year, complete exemption from Capital Gains Tax on profits from shares held for three years, and valuable loss relief to mitigate potential downside risk against your income.

Understanding the mechanics of seis tax relief is the first step; the next is identifying qualifying high-growth companies with the potential for significant returns. BGS Capital acts as an introducer, connecting our network of sophisticated investors and funds with pre-vetted, pre-IPO businesses actively raising capital. To apply your knowledge to tangible prospects and gain direct access to these opportunities, we invite you to explore pre-vetted SEIS investment opportunities. Take the next step in building a robust, tax-efficient portfolio today.

Frequently Asked Questions

What is the difference between SEIS and EIS tax relief?

The Seed Enterprise Investment Scheme (SEIS) is designed for very early-stage companies, while the Enterprise Investment Scheme (EIS) supports slightly larger, more established businesses. SEIS offers more generous incentives, including 50% income tax relief on investments up to £200,000 per tax year, compared to 30% for EIS on investments up to £1 million.

Additionally, SEIS provides a full Capital Gains Tax (CGT) exemption on profits from the shares, whereas EIS offers CGT deferral relief.

What happens to my tax relief if I sell my SEIS shares within three years?

If you dispose of your SEIS shares within the three-year qualifying period, any income tax relief you claimed will be withdrawn by HMRC. This process is often referred to as “clawback.” The amount withdrawn is typically proportional to the amount of shares sold. Furthermore, you will lose any Capital Gains Tax exemption that would have applied to the profits from those shares, making the gain potentially liable for CGT.

Can I claim SEIS relief if I am not a UK resident?

Eligibility for SEIS relief is contingent on having a UK income tax liability, not on UK residency status. Therefore, a non-resident individual who has a liability to UK income tax (for instance, from UK-based employment or rental income) can claim the relief against that specific liability. The claim is made through a UK self-assessment tax return. It is the UK tax liability, not your physical location, that is the determining factor.

How long does it typically take to receive the SEIS3 certificate from a company?

A company can only apply to HMRC for compliance certificates (SEIS3 forms) after it has been trading for at least four months or has spent 70% of the funds raised. Once the company submits its application, HMRC processing can take from several weeks to a few months. After approval, the company receives the SEIS3 forms and distributes them to its investors, who then use them to claim their seis tax relief.

Can I invest in an SEIS company through a nominee service?

Yes, it is permissible to invest in an SEIS-qualifying company via a nominee service. In this structure, the nominee holds the legal title to the shares, but you remain the beneficial owner. As the beneficial owner, you are the individual entitled to claim the associated tax reliefs. The nominee structure simplifies the administration for the company, and the SEIS3 certificate will still be issued for you to make your personal tax claim.

What are the main risks of investing in SEIS-qualifying companies?

The primary risk is the potential for a total loss of capital. These are high-risk, early-stage ventures with a significant failure rate. Another key risk is illiquidity; shares in private companies are not publicly traded and can be very difficult to sell. Finally, the availability of seis tax relief is not guaranteed and depends on both the investor’s circumstances and the company maintaining its qualifying status for the full three-year period.