The 30% income tax relief provided by the Enterprise Investment Scheme isn’t a guaranteed windfall. It’s a specific reward for investors who successfully navigate the UK’s most stringent regulatory frameworks. You likely understand that while the potential for 100% Capital Gains Tax exemption is significant, the complexity of HMRC rules creates a genuine risk of relief clawback. Identifying genuine EIS eligible companies requires more than a cursory glance at a pitch deck. It demands a rigorous assessment of the statutory “risk to capital” gateway and the £12 million lifetime funding limit.

This 2026 guide provides the technical clarity needed to identify high-growth UK companies that meet every qualifying requirement. You’ll discover how sophisticated investors use specific criteria to filter out high-risk failures and access exclusive pre-IPO opportunities. We’ll break down the 7 year age limit for trades and the essential “knowledge intensive” status that can extend eligibility for certain firms. This analysis ensures you don’t overlook the technicalities that separate a tax-efficient growth engine from a compliance nightmare. CAPITAL AT RISK.

Key Takeaways

- Understand the 2026 UK economic landscape and why the government maintains the Enterprise Investment Scheme as a vital engine for startup growth and 30% tax relief.

- Master the “Risk to Capital” gateway and the £15 million gross asset limit required to identify legitimate EIS eligible companies for your portfolio.

- Identify the updated list of excluded sectors, including banking and property development, to ensure prospective investments remain compliant with HMRC standards.

- Learn professional due diligence techniques to assess a firm’s business potential and the quality of its Investor Relations team during the pre-IPO phase.

- Discover how to connect with a database of qualified opportunities through BGS Capital’s role as a specialist investment introducer for sophisticated investors.

The 2026 Landscape for EIS Eligible Companies

The 2026 UK economy relies on high-growth sectors to drive national productivity. The Enterprise Investment Scheme (EIS) remains the cornerstone of the UK venture capital ecosystem. Following the government’s 2023 commitment to extend the scheme’s sunset clause to 2035, the 2026 fiscal year sees record levels of deployment into EIS eligible companies. This stability allows founders to plan long-term cycles without the threat of expiring tax incentives.

The government continues to back EIS as a primary engine for startup growth because it addresses the “equity gap” for businesses seeking between £500,000 and £5 million. By April 2026, HM Revenue and Customs (HMRC) data shows that over £30 billion has been raised through the scheme since its inception. The dual benefit remains unchanged; companies secure vital scale-up capital, while investors access a suite of tax efficiencies designed to mitigate the inherent dangers of early-stage backing.

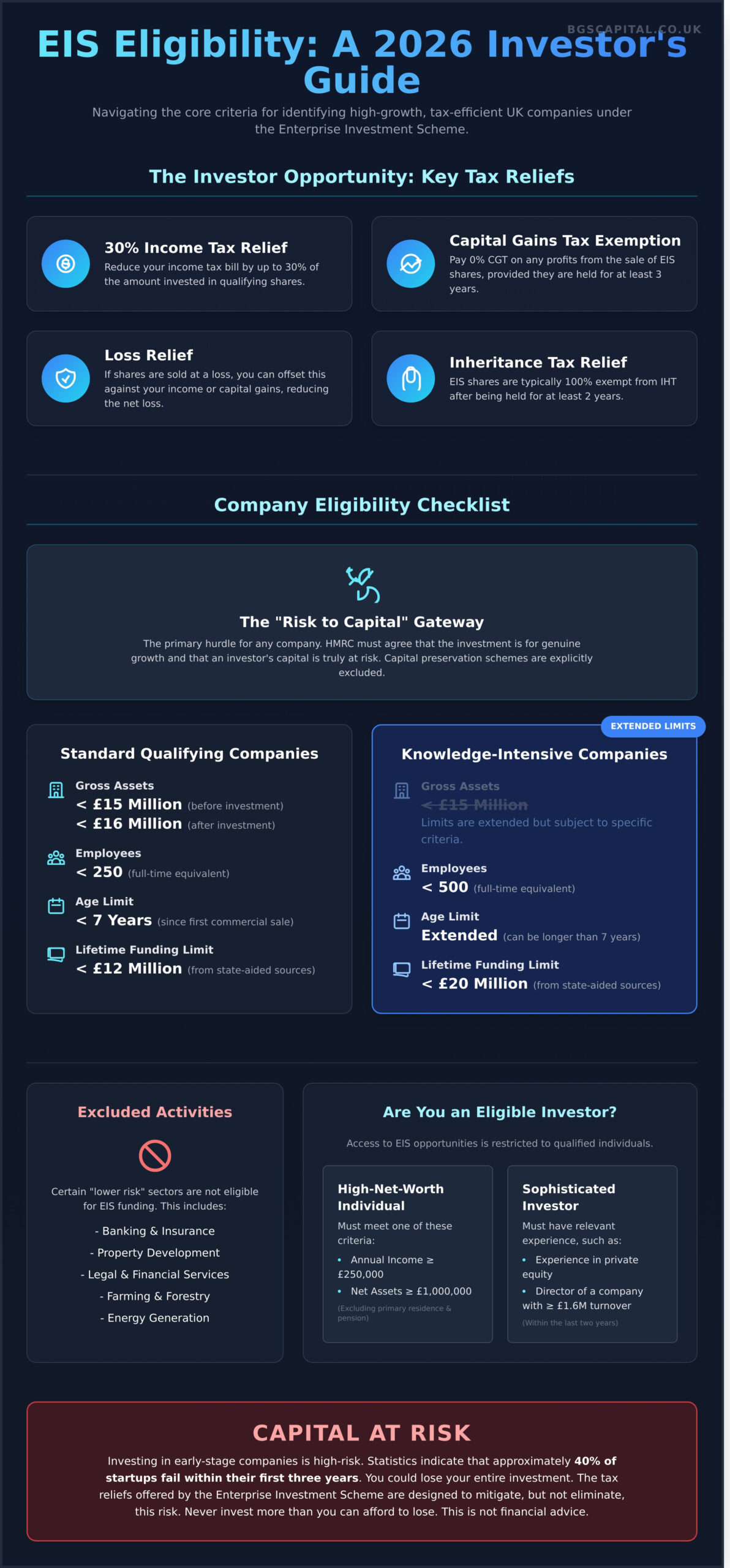

- 30% Income Tax Relief: Investors can reduce their tax bill by 30% of the amount invested.

- Capital Gains Tax (CGT) Exemption: Any profit made on the disposal of EIS shares is tax-free if held for at least three years.

- Loss Relief: If the company fails, investors can offset the loss against their income tax or CGT.

- Inheritance Tax (IHT) Relief: Shares are generally 100% exempt from IHT after two years of ownership.

The Role of EIS in Pre-IPO Investing

EIS eligibility is a critical precursor to successful IPO listings on the London Stock Exchange. In 2026, companies stay private for longer; the average time to go public now reaches 11 years. Sophisticated investors prioritize EIS eligible companies because the “risk to capital” gateway enforced by HMRC acts as a rigorous third-party validation of a firm’s growth intent. Securing EIS status suggests a company is structured for aggressive scaling rather than lifestyle management. This makes it a staple for portfolios targeting significant pre-IPO capital appreciation.

Am I Eligible? The Investor Qualification

BGS Capital is an introducer, not a broker or advisor. Access to our network is restricted to individuals who meet specific regulatory criteria. For the 2026/27 tax year, you must qualify under one of two primary categories. A High-Net-Worth Individual is defined as someone with an annual income of £250,000 or more, or net assets exceeding £1 million excluding their primary residence. Alternatively, a Self-Certified Sophisticated Investor must have experience in private equity or have been a director of a company with a £1.6 million turnover within the last two years.

We require all users to complete a self-certification process before we disclose specific company details or offer documents. This ensures compliance with Financial Conduct Authority (FCA) standards. If you don’t meet these requirements, you won’t be able to view our exclusive EIS listings. Our role is to connect qualified investors with vetted opportunities; we don’t facilitate the raises ourselves or handle client funds directly.

Core Criteria: What Makes a Company EIS Eligible?

The “Risk to Capital” gateway is the first hurdle. HMRC implemented this test in April 2018 to ensure that EIS eligible companies use the funds for genuine entrepreneurial growth. The company must show it has a long-term objective to increase its turnover and customer base. This requirement excludes “capital preservation” schemes where the downside is artificially protected. If the investment structure looks like a debt instrument rather than equity, it’ll fail the test. The focus is entirely on businesses that need external capital to scale operations or enter new markets.

EIS eligible companies must meet strict size and asset constraints. At the time of the share issue, the company’s gross assets cannot exceed £15 million. This limit increases to £16 million immediately following the investment. Additionally, the firm must have fewer than 250 full-time equivalent employees. For knowledge-intensive companies, these thresholds are higher; they can have up to 500 employees and receive up to £20 million in lifetime funding. You can find more details in this British Business Bank guide to EIS which outlines these specific parameters for different business types.

The company must also carry out a qualifying trade. Most sectors qualify, but HMRC excludes activities like property development, financial services, legal services, and energy generation. The business must be a small, independent entity. It can’t be controlled by another company, and it must not have more than 50% of its shares owned by another firm. This independence ensures that the tax relief supports genuine SMEs rather than subsidiaries of larger corporations.

Unquoted status is a non-negotiable requirement. The company cannot be listed on the London Stock Exchange Main Market. However, shares traded on the Alternative Investment Market (AIM) or the Aquis Stock Exchange (AQSE) are eligible. HMRC views these as unquoted for tax purposes. If a company moves to the Main Market before the investment is finalised, eligibility for that round is voided.

The Three-Year Rule for Share Retention

Investors must hold their shares for at least three years from the date of issue or the start of trade. If you sell shares before this window closes, HMRC will “claw back” the 30% income tax relief. This rule ensures capital stays within the business. Consequently, EIS investments are illiquid. Investors often use an eligibility checker to ensure their portfolio aligns with these long-term requirements.

Advance Assurance: The Gold Standard of Eligibility

Advance Assurance is a provisional HMRC ruling on a company’s qualifying status. It provides investors with confidence that tax reliefs will be available. While not mandatory, it is a market standard. Companies provide business plans to prove they meet the requirements, including those related to the “sunset clause” recently extended to 2035. Without this assurance, the risk of HMRC rejecting the claim later is significantly higher.

Excluded Activities and the Knowledge Intensive Edge

HMRC restricts EIS access to ensure capital flows into genuine risk-taking ventures rather than asset-backed or low-risk operations. Businesses involved in “excluded activities” cannot qualify for the scheme. This list includes banking, insurance, money lending, and debt-related services. Farming, market gardening, and forestry are also barred. Property development and hotels are excluded because they rely on underlying asset value rather than operational innovation. Legal and accounting services do not qualify either. As of 2024, the government remains committed to these exclusions to prevent the scheme from being used as a tax-efficient vehicle for capital-preservation trades.

Knowledge Intensive Companies (KICs) represent the premium tier of EIS eligible companies. To achieve KIC status, a firm must meet specific research and development (R&D) expenditure requirements. This usually means spending at least 15% of operating costs on R&D in one of the last three years. Alternatively, the company must be creating intellectual property expected to be its main business activity. These firms access higher funding limits. They can raise up to £10 million annually, which is double the £5 million limit for standard companies. The total lifetime cap for KICs is £20 million, compared to £12 million for standard firms. Reviewing the UK Government EIS Eligibility Criteria provides the full technical framework for these designations.

Sector Exclusions vs. Qualifying Trades

EIS prioritizes innovation-led sectors like SaaS, Biotech, and CleanTech. Land-intensive or financial-heavy businesses are excluded to ensure investors take on genuine “risk to capital.” If a business derives more than 20% of its turnover from excluded activities, it loses its status. This creates a clear divide between traditional asset-heavy businesses and modern, scalable technology firms.

| Feature | Standard EIS Company | Knowledge Intensive (KIC) |

|---|---|---|

| Annual Raise Limit | £5 Million | £10 Million |

| Lifetime Limit | £12 Million | £20 Million |

| Maximum Employees | 250 | 500 |

| Age Limit | 7 Years | 10 Years |

The 10-Year Rule for Older Companies

Age limits are a critical gatekeeping factor for EIS eligible companies. Standard firms must receive their first EIS investment within 7 years of their first commercial sale. KICs have a broader 10-year window. There’s an exception for companies entering a new geographic or product market. If the required investment exceeds 50% of the company’s average turnover for the previous 5 years, they may still qualify regardless of age. BGS Capital filters for companies within these critical growth windows. This ensures investors access firms that are established enough to scale but still within the tax-advantaged period. CAPITAL AT RISK.

Qualification isn’t a one-time event. Companies must maintain these standards throughout the three-year investment period. If a firm pivots into an excluded activity during this time, HMRC can claw back the tax relief from investors. Professional due diligence is the only way to mitigate this risk. We operate as an introducer to help you find these opportunities. Am I Eligible?

Due Diligence: Vetting EIS Opportunities in 2026

Identifying EIS eligible companies is merely the regulatory baseline for a sophisticated investor. By 2026, the UK’s early-stage ecosystem has matured, requiring a shift from tax-centric thinking to fundamental business analysis. You shouldn’t mistake tax relief for a safety net. If the underlying business model is flawed, a 30% upfront relief won’t compensate for a 100% loss of capital. Sophisticated investors must prioritize scalability and market fit over the tax wrapper itself.

A company’s Investor Relations (IR) team serves as a primary indicator of its pre-IPO maturity. In 2026, firms aiming for a public listing within 18 to 36 months must demonstrate institutional-grade communication. Professional IR teams provide quarterly updates, transparent cap tables, and clear KPIs. If a company lacks a dedicated point of contact for shareholders, it often indicates a lack of readiness for the rigours of the London Stock Exchange or the AIM market.

The “use of funds” section in any proposal requires strict scrutiny. HMRC mandates that EIS capital must be used for “growth and development” within a 24-month window. This includes activities like hiring 15 new engineers, expanding into the European market, or launching a specific product line. You must avoid companies that intend to use the capital for “capital preservation” or debt servicing. HMRC frequently disqualifies firms that attempt to use EIS for low-risk, asset-backed strategies that don’t meet the “risk to capital” condition. CAPITAL AT RISK.

Analyzing the Information Memorandum (IM)

An Information Memorandum (IM) is a legal document outlining the investment opportunity and associated risks. You must scrutinize the “Exit Strategy” section with precision. Look for detailed plans regarding an IPO, a secondary placing to private equity firms, or a trade sale to a named list of potential acquirers. Verify that the valuation is based on 2026 market multiples rather than speculative 2021-era peaks. Check the “Risk Factors” for specific sector threats rather than generic boilerplate text.

The Importance of an Introducer Network

Direct searching for EIS eligible companies is inefficient for High Net Worth (HNW) individuals. The sheer volume of startups makes manual vetting impossible. Most high-quality, pre-IPO opportunities don’t advertise on public forums; they circulate within closed networks. A curated database of IPO-ready businesses allows you to bypass the noise of seed-stage ventures that lack proven revenue streams. Accessing these opportunities requires a gateway that understands both the regulatory requirements and the commercial viability of the firm.

BGS Capital operates as a specialist facilitator in this space. We connect sophisticated investors directly with qualifying companies that have already passed initial internal filters. This model ensures that you only review businesses with a structured path toward a liquidity event. Instead of managing dozens of fragmented relationships, you can leverage a centralized network to find opportunities that align with your specific risk profile and sector interests.

Determine your status to access exclusive pre-IPO and EIS opportunities. Am I Eligible?

- Growth Focus: Ensure £1.5m+ annual recurring revenue for pre-IPO targets.

- Timeline: Verify the 2-year deployment plan for all EIS capital.

- Exits: Prioritize companies with a 3-to-5-year liquidity horizon.

It’s vital to remember that EIS investments are long-term commitments. You’re typically locked in for a minimum of three years to retain tax benefits, but the actual path to an exit often takes five to seven years. In 2026, the most successful investors are those who look past the immediate tax deduction and focus on the company’s ability to dominate its niche. High-level investing requires a detached, analytical approach to every Information Memorandum you receive.

Connecting with Qualified Opportunities via BGS Capital

BGS Capital operates as a specialist introducer in the UK equity market. We bridge the gap between sophisticated investors and high-growth, pre-IPO firms. Our platform functions as a professional conduit; we don’t facilitate the raises ourselves or provide financial advice. Instead, we offer a streamlined environment where qualified individuals can identify and evaluate EIS eligible companies. This approach ensures that both investors and founders interact within a framework of professional transparency. CAPITAL AT RISK.

The platform provides free access to a curated database of opportunities. This database is not open to the general public. It is a restricted resource designed for those who understand the risks and rewards of early-stage investing. By centralising these opportunities, we allow wealth managers and private investors to compare different sectors and growth stages in one location. This efficiency is vital for those looking to deploy capital before the end of the current tax year.

How to Access the BGS Capital Database

The process to gain entry is direct and compliant. Prospective users must first answer the question: Am I Eligible? This involves a self-certification process to confirm your status as a High Net Worth (HNW) or Sophisticated Investor. These classifications are defined by FCA regulations; they ensure that participants have the financial resilience or experience required for illiquid investments. Once you complete this step, you gain full access to the database.

The platform facilitates direct introductions to Investor Relations teams. We believe in removing unnecessary intermediaries. When you identify a firm that fits your portfolio, you can request a direct connection. This allows you to receive investment memorandums and technical data directly from the source. It also enables you to conduct your own due diligence without filtered communication. Start the qualification process today to see active placements in the green energy, technology, and healthcare sectors.

For Companies: Raising Capital through EIS

For UK businesses, the Enterprise Investment Scheme is a powerful tool for scaling. Since its inception, thousands of firms have used the scheme to secure over £30 billion in total investment. Featuring your business on BGS Capital puts your proposition in front of a network of accredited wealth managers and HNW individuals. This visibility is essential for companies aiming to reach their £5 million annual EIS limit. It is a transactional environment focused on results.

To attract serious capital, you must showcase your HMRC Advance Assurance. This document is a critical marker of professional readiness. It tells potential investors that your company has been pre-screened by HMRC for tax relief eligibility. In a competitive market, this assurance can be the deciding factor for an investor. Feature your business and connect with qualified investors to accelerate your funding round and gain access to our network of capital providers.

Your 2026 tax planning must align strictly with EIS rules. The 30% income tax relief and capital gains tax exemptions are significant, but they require total compliance with HMRC’s “risk to capital” gateway. BGS Capital remains a specialist facilitator; we provide the data and the connections, but the responsibility for final compliance rests with the parties involved. Ensure your documentation is robust before seeking an introduction to our network.

Secure Your Position in the 2026 EIS Market

The 2026 investment landscape demands a rigorous approach to identifying EIS eligible companies. The UK government’s commitment to extending the sunset clause to 2035 provides long-term certainty for those seeking 30% income tax relief on qualifying investments. Focus your strategy on Knowledge Intensive Companies to access higher annual investment limits of £2 million per tax year. Success in this sector depends on verifying that a firm meets the “risk to capital” condition and operates outside excluded sectors like asset management or property development.

BGS Capital facilitates this process by providing sophisticated and high net worth investors with exclusive access to pre-IPO and IPO opportunities. Our network offers direct introductions to company Investor Relations teams while maintaining strict adherence to UK compliance standards. It’s essential to remember that all capital is at risk. By following a structured due diligence framework, you can align your portfolio with UK enterprises positioned for growth in the coming years.

Am I Eligible? Check your qualification to access EIS opportunities

Frequently Asked Questions

What are the main tax benefits of investing in EIS eligible companies?

Investing in EIS eligible companies offers 30% upfront income tax relief on investments up to £1 million per tax year. You pay zero Capital Gains Tax on profits made from these shares if you hold them for at least 3 years. If the business fails, you can claim loss relief against your income tax or capital gains. Shares also qualify for 100% Inheritance Tax relief via Business Property Relief after a 2 year holding period.

Can a company lose its EIS eligibility after I’ve invested?

A company loses its status if it breaches HMRC compliance rules within the 3 year relevant period. This happens if the business changes its trade to an excluded activity or exceeds the £15 million gross asset limit. If eligibility is withdrawn, HMRC will claw back your 30% income tax relief. Investors should monitor the company’s ongoing adherence to HMRC requirements. CAPITAL AT RISK.

What is the maximum amount I can invest in EIS companies per tax year?

The standard maximum investment is £1 million per tax year for individual investors. This limit increases to £2000000 if at least £1 million of that total is invested in knowledge-intensive companies. You can use carry back provisions to apply the relief to the previous tax year’s liabilities. This flexibility allows sophisticated investors to manage tax obligations across two fiscal periods. Check your status to confirm: Am I Eligible?

Do AIM-listed companies qualify for EIS?

Specific AIM-listed companies qualify for EIS because HMRC doesn’t classify AIM as a recognized stock exchange. To be eligible, the firm must maintain fewer than 250 full-time employees and have gross assets under £15 million at the time of share issue. Investing in these EIS eligible companies provides a route to liquidity while retaining significant tax advantages. Not all AIM stocks qualify; you must verify the company’s trading status first.

How long must I hold my EIS shares to avoid Capital Gains Tax?

You must hold your EIS shares for a minimum of 3 years to maintain the Capital Gains Tax exemption. Selling or gifting the shares before this 36 month period ends triggers a mandatory repayment of your initial 30% income tax relief. The 3 year clock starts specifically from the date the shares are issued, not the date you sent the funds. This duration ensures the capital remains committed to the growth of the UK enterprise.

What is the difference between SEIS and EIS eligible companies?

SEIS targets startups in their first 3 years of trading with fewer than 25 employees and assets under £350,000. It offers 50% income tax relief on investments up to £200,000 per year. EIS is for more established firms with up to 250 employees and £15 million in assets. While SEIS provides higher percentage relief, EIS allows for much larger capital allocations into businesses that have already cleared the initial startup phase.

Is there a limit on how much an EIS company can raise in its lifetime?

Most companies face a lifetime funding limit of £12 million from all venture capital schemes, including EIS and VCTs. For knowledge-intensive companies, this lifetime cap rises to £20 million. Additionally, a firm cannot raise more than £5 million in any single 12 month period. These restrictions ensure the tax relief supports small and medium-sized enterprises rather than large corporations. Exceeding these limits voids the company’s eligibility for the scheme.

How do I claim EIS tax relief on my self-assessment return?

You claim relief by completing the Additional Information pages of your self-assessment tax return using the figures from your EIS3 certificate. The company issues this certificate after HMRC authorizes the claim, which usually takes 3 to 6 months post-investment. If you’re a PAYE taxpayer, you can ask HMRC to adjust your tax code once you receive the certificate. This provides the tax benefit during the current year rather than waiting for the annual return cycle.