For sophisticated UK investors, navigating the landscape of tax-efficient schemes presents a significant challenge. The distinctions between options like EIS, SEIS, and a Venture Capital Trust (VCT) are often nuanced, leading to uncertainty about risk, liquidity, and regulatory complexity. Understanding these differences is critical for making strategic investment decisions that align with your financial objectives and risk appetite.

This guide provides a comprehensive and direct analysis of the VCT structure. We will detail the substantial tax incentives available, including up to 30% income tax relief on investments up to £200,000 per tax year. Furthermore, we will dissect the inherent risks associated with backing early-stage companies, clarify the rules governing VCTs, and provide an objective comparison against other government-approved venture capital schemes. The objective is to equip you with the information required to assess if a VCT is a suitable component of your investment portfolio.

Key Takeaways

- Grasp the fundamental structure of a Venture Capital Trust and its role in funding high-growth, unlisted UK companies.

- Identify the substantial tax reliefs offered by the UK government that make investing in a VCT a tax-efficient strategy.

- Appreciate the high-risk nature of these investments and the critical importance of understanding that your capital is at risk.

- Learn the key differences between VCT, EIS, and SEIS to make an informed decision on which scheme aligns with your objectives.

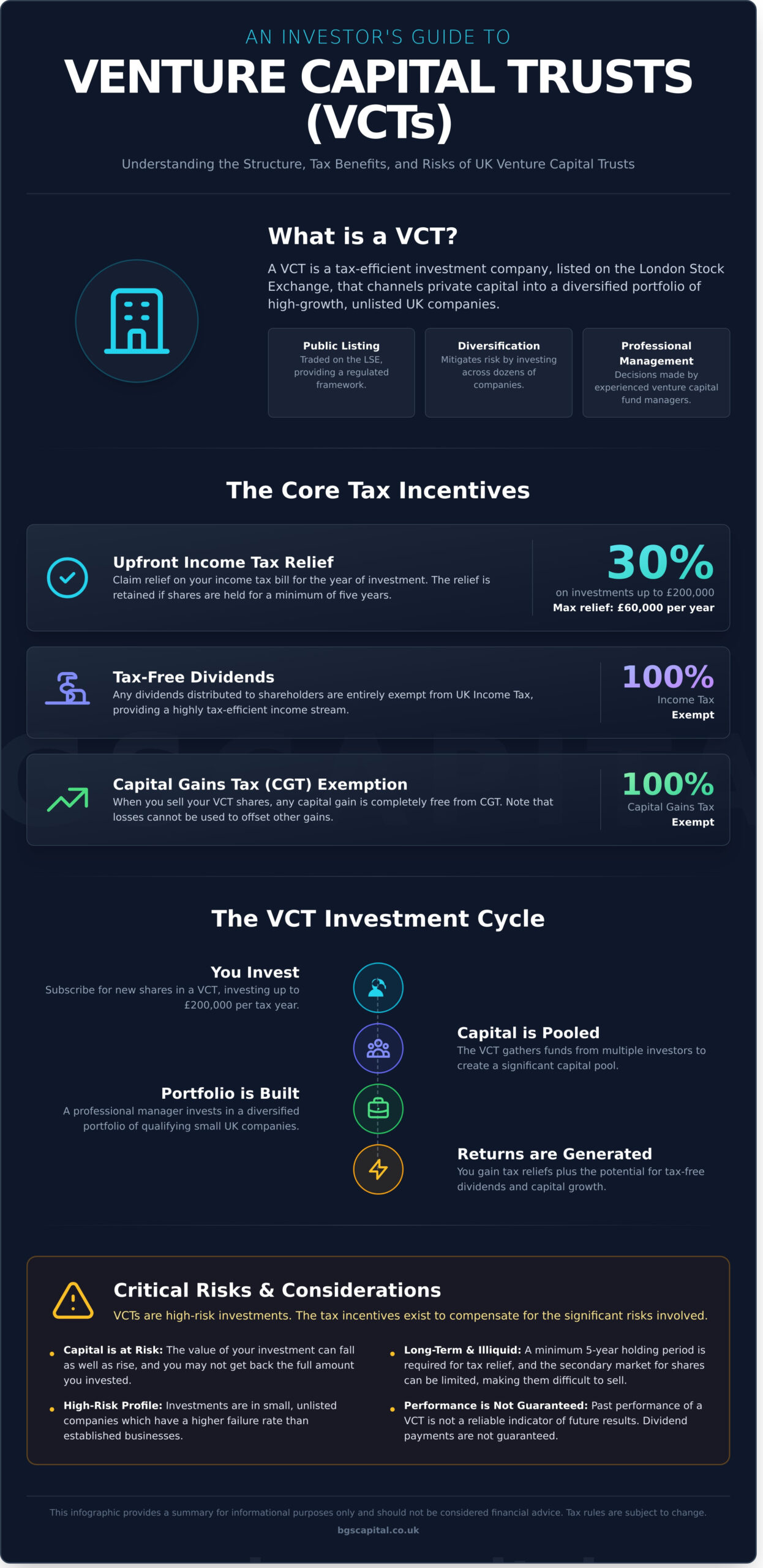

What is a Venture Capital Trust (VCT) and How Does it Work?

A Venture Capital Trust (VCT) is a highly specialised, tax-efficient investment vehicle listed on the London Stock Exchange (LSE). Its core purpose is to channel private investment into small, unlisted UK companies that have significant growth potential. Established by the UK government, the scheme incentivises investors with substantial tax reliefs in exchange for providing long-term capital to these early-stage businesses. This structure creates a symbiotic relationship: innovative companies gain access to vital funding, and investors gain exposure to a high-growth asset class with tax advantages. For a more detailed breakdown of their history and regulatory background, the Venture Capital Trust (Wikipedia) page offers a comprehensive resource.

The Structure of a VCT

A VCT operates as a closed-ended investment company, meaning it raises a fixed amount of capital through an initial share offering. This capital is then managed by a professional venture capital firm responsible for identifying, evaluating, and managing a portfolio of investments. Key structural features include:

- Public Listing: VCT shares are traded on the LSE, providing a regulated framework. However, the secondary market for these shares can be illiquid, making them a long-term investment.

- Portfolio Diversification: By pooling funds from multiple investors, a VCT builds a diversified portfolio across dozens of qualifying companies, which helps to mitigate the inherent risk of venture capital investing.

- Professional Management: Investment decisions are made by an experienced fund manager with expertise in the early-stage and growth capital markets.

What are ‘Qualifying’ Companies?

To ensure the scheme supports genuine growth businesses, HMRC imposes strict rules on the types of companies a VCT can invest in. These ‘qualifying holdings’ must meet specific criteria regarding their size, age, and business activities. Generally, they are UK-based companies with fewer than 250 full-time employees and gross assets of less than £15 million at the time of investment. The focus is on innovative firms with high-growth potential, often in sectors such as technology, life sciences, healthcare, and renewable energy. This targeted approach is designed to fuel the UK’s most promising enterprises.

The Key Tax Benefits of Investing in a VCT

For many sophisticated investors, the primary motivation for allocating capital to a Venture Capital Trust (VCT) is the significant suite of tax reliefs offered by the UK government. These incentives are not arbitrary; they are specifically designed to compensate investors for the higher level of risk associated with backing smaller, unquoted UK companies. To qualify for and retain these benefits, certain conditions must be met, most notably a minimum holding period for the VCT shares.

Upfront Income Tax Relief

Investors can claim up to 30% relief on their income tax liability for the year of investment. This is applicable on new VCT share subscriptions up to a maximum of £200,000 per tax year, potentially reducing an income tax bill by as much as £60,000. It is crucial to note that the shares must be held for a minimum of five years to retain this initial relief. The claim is made through an individual’s Self-Assessment tax return. The complete rules governing Venture Capital Schemes tax relief are detailed by HMRC.

Tax-Free Dividends

A core component of the return profile for a vct is the payment of dividends. Any dividends distributed to shareholders are entirely exempt from UK income tax. This can provide a highly tax-efficient income stream, which contrasts sharply with dividends from standard company shares that are subject to dividend tax rates. However, investors must recognise that dividend payments are not guaranteed and are wholly dependent on the performance of the VCT’s underlying portfolio companies.

Capital Gains Tax (CGT) Exemption

When an investor disposes of their VCT shares, any capital gain realised is completely exempt from Capital Gains Tax (CGT). This is a substantial long-term benefit, as there is no upper limit to the amount of gain that can be sheltered from tax. This feature makes a VCT a powerful tool for wealth accumulation. It is important to note the inverse: if a loss is realised upon the sale of VCT shares, this loss cannot be used to offset capital gains from other investments.

Understanding the Risks and Considerations of VCTs

While the tax incentives associated with Venture Capital Trusts are compelling, they exist to compensate investors for undertaking a significantly higher level of risk compared to mainstream investments. It is imperative for investors to understand that VCTs are high-risk, long-term investments where capital is at risk. The value of your investment can fall as well as rise, and you may not get back the full amount you invested. Past performance is not a reliable indicator of future results.

Before committing capital, a thorough assessment of the following key risk categories is essential.

Investment and Performance Risk

The primary risk stems from the nature of the underlying assets. VCTs invest in small, unlisted, or AIM-listed companies which are often early-stage and unproven. These businesses have a higher failure rate than established corporations. Consequently, the value of a VCT’s portfolio can be volatile and may fall significantly. The expertise of the fund manager is critical in selecting viable companies, and poor performance can directly lead to capital loss. Furthermore, smaller companies are often more vulnerable to economic downturns, which can disproportionately impact a VCT’s portfolio value.

Liquidity and Market Risk

Unlike shares in FTSE 100 companies, VCT shares are inherently illiquid. There is no guarantee of a ready buyer when you wish to sell, particularly within the minimum five-year holding period required for tax relief. The secondary market is limited, often resulting in a wide ‘spread’ between the buying and selling price. While many VCTs offer share buy-back schemes to provide an exit route, these are typically executed at a discount to the Net Asset Value (NAV) and are not guaranteed.

Legislative and Tax Rule Changes

The generous tax reliefs offered are a core attraction of any vct investment, but they are subject to government policy. Future legislative changes could alter, reduce, or even withdraw these tax incentives, impacting the investment’s overall return and appeal. Similarly, modifications to HMRC rules defining ‘qualifying holdings’ can force a VCT to adjust its investment strategy, potentially affecting its risk profile and performance potential. Investors must be aware that the regulatory landscape can change.

VCTs vs. EIS & SEIS: Key Differences for Investors

For UK investors seeking tax-efficient exposure to early-stage companies, Venture Capital Trusts (VCTs), the Enterprise Investment Scheme (EIS), and the Seed Enterprise Investment Scheme (SEIS) are primary considerations. While all three are government initiatives designed to stimulate investment into smaller, unlisted UK businesses, their structures, tax benefits, and risk profiles differ significantly. Understanding these distinctions is critical for aligning an investment with your financial objectives and risk tolerance.

Investment Structure and Diversification

The most fundamental difference lies in how capital is deployed. A vct operates as a fund, providing immediate diversification by investing your capital across a portfolio of 30-100 qualifying companies selected and managed by a professional fund manager. This structure mitigates single-company failure risk.

Conversely, EIS and SEIS involve direct investment into individual, qualifying companies. This approach requires the investor to build their own portfolio to achieve diversification, a process that demands significant time, research, and access to deal flow. While it offers more control over individual holdings, the risk is concentrated in each separate investment.

Tax Reliefs Compared

Each scheme offers a distinct package of tax incentives. The key reliefs are compared below. It is important to note that tax treatment depends on individual circumstances and may be subject to change in the future.

| Feature | Venture Capital Trust (VCT) | Enterprise Investment Scheme (EIS) | Seed Enterprise Investment Scheme (SEIS) |

|---|---|---|---|

| Income Tax Relief | 30% on up to £200,000 invested | 30% on up to £1,000,000 invested | 50% on up to £200,000 invested |

| Capital Gains | Dividends and capital growth are tax-free | Capital gains are tax-free after 3 years; CGT deferral available | Capital gains are tax-free after 3 years; CGT deferral and 50% reinvestment relief available |

| Loss Relief | Not available to the investor (held within the fund) | Available against income or capital gains | Available against income or capital gains |

| Minimum Holding Period | 5 years (to retain income tax relief) | 3 years | 3 years |

Risk Profile and Control

Due to its pooled structure, a VCT is generally considered less risky than a single EIS or SEIS investment. The fund manager’s expertise and the inherent diversification spread the risk of potential company failures. In contrast, EIS and SEIS investors assume concentrated risk with each investment, although this is partially offset by the generous loss relief available. This direct model, however, grants the investor greater control and a closer relationship with the companies they choose to back.

Ultimately, the choice depends on an investor’s preference for a managed, diversified fund (VCT) versus a hands-on, high-risk/high-reward portfolio of direct investments (EIS/SEIS). For those looking to explore direct venture opportunities, you can learn more about the EIS and SEIS schemes here.

How to Invest in a VCT: Rules and Process

Investing in a Venture Capital Trust requires adherence to specific rules and a structured process. For qualified investors, understanding these steps is critical to accessing the potential tax benefits and navigating the market for VCT offers. This section provides a functional guide to the subscription process.

Investor Eligibility and Subscription Limits

To qualify for the tax reliefs associated with a vct investment, an individual must meet several criteria set by HMRC. The primary requirements are:

- Age and Residency: You must be at least 18 years of age and a UK resident for tax purposes.

- Subscription Limit: The maximum investment on which you can claim income tax relief in any single tax year is £200,000.

- Independence: You cannot be ‘connected’ with the VCT, which typically means you are not an employee or director of the fund management company.

Finding and Choosing a VCT

New VCT share offers are not typically available on mainstream retail investment platforms. Access is usually facilitated through professional channels such as independent financial advisers (IFAs) and wealth managers. Some specialist platforms may also list current offers.

Thorough due diligence is essential. Before committing capital, investors should:

- Analyse the Manager: Scrutinise the fund manager’s track record, investment strategy, and sector focus.

- Review Key Documents: Carefully read the VCT’s prospectus and the Key Information Document (KID). These documents detail the investment objectives, risk factors, and charges.

Crucially, given the complexity and high-risk nature of these investments, seeking independent financial advice is strongly recommended to ensure the opportunity aligns with your personal financial circumstances and risk tolerance.

The Investment Process

Once a suitable opportunity has been identified, the investment process is straightforward. Most new investments are made during a specific fundraising period, either through a new share offer or a ‘top-up’ offer for an existing fund. The process involves completing an application form and transferring the subscription funds. Following the successful allotment of shares, you will receive two key documents: a share certificate confirming your ownership and a tax certificate. This tax certificate is the official document required to claim your 30% income tax relief from HMRC via your self-assessment tax return.

For sophisticated and high-net-worth investors seeking access to a range of venture capital opportunities, networks like BGS Capital can provide connections to relevant firms.

VCTs: A Strategic Tool for the Sophisticated UK Investor

Venture Capital Trusts represent a compelling, albeit high-risk, proposition for eligible UK investors. The key takeaways are clear: they offer substantial tax efficiencies, including up to 30% upfront income tax relief and tax-free dividends, in exchange for funding the UK’s most promising early-stage companies. However, investors must remain cognisant of the inherent risks, including the potential for capital loss and the long-term, illiquid nature of these investments. Understanding these dynamics is crucial for making an informed decision.

While a vct offers a fund-based approach to venture capital, many sophisticated investors also seek direct access to individual growth opportunities. For those looking to build a more direct portfolio of pre-IPO and unquoted businesses, accessing a network of vetted deals is paramount. BGS Capital operates as an introducer, providing introductions to qualified companies seeking capital via our network of accredited investment firms.

If you are an eligible investor, you can gain access to our network at no cost. Explore vetted pre-IPO and high-growth investment opportunities. Position yourself at the forefront of UK enterprise and innovation.

Frequently Asked Questions

What are the typical annual fees and charges for a VCT?

Investors should anticipate several charges. An initial charge can be up to 5.5%, though often reduced by platforms. The Annual Management Charge (AMC) typically ranges from 1.5% to 2.5% of net asset value. Additional costs can include performance fees, administration fees, and custodian charges. It is imperative to review the Key Information Document (KID) for a comprehensive breakdown of all costs associated with a specific VCT before investing capital.

Can I hold a VCT within a SIPP or ISA?

No. A Venture Capital Trust is a tax-efficient investment wrapper in its own right and is not eligible to be held within other tax-advantaged accounts like an Individual Savings Account (ISA) or a Self-Invested Personal Pension (SIPP). The unique tax reliefs, such as 30% upfront income tax relief and tax-free dividends, are only applicable when the VCT is held directly by the investor.

What happens to a VCT investment upon death?

Upon the death of an investor, the VCT shares become part of their estate. While VCTs are not automatically exempt from Inheritance Tax (IHT), they may qualify for 100% relief via Business Property Relief (BPR) if held for at least two years. The tax-free status of any dividends paid is passed on to beneficiaries, but the initial income tax relief is not transferable. Professional advice should be sought for estate planning.

How often do VCTs typically pay dividends?

Most VCTs aim to provide a regular income stream to investors by paying tax-free dividends. Payments are commonly made on a semi-annual or annual basis. The target yield often ranges from 5% to 10% of the Net Asset Value (NAV) per annum. However, dividend payments are not guaranteed and are entirely dependent on the performance and successful realisations of the underlying portfolio companies.

Are VCTs suitable for retail investors or only sophisticated investors?

VCTs are high-risk, long-term, and illiquid investments. They are therefore considered suitable for sophisticated or high-net-worth investors who understand the risks of investing in small, unquoted companies and can withstand a total loss of capital. Due to the complexity and risk profile, a VCT is generally not appropriate for inexperienced retail investors or those with a low-risk tolerance. Eligibility checks are standard practice.

What is the difference between a generalist and a specialist VCT?

A generalist VCT invests across a diverse range of industries, spreading investment risk and avoiding concentration in a single sector. This diversification is a key part of its strategy. Conversely, a specialist VCT focuses its capital on a specific sector, such as financial technology or healthcare. This concentrated approach offers the potential for higher returns if the sector performs well, but it also carries a significantly higher level of sector-specific risk.