UK Inheritance Tax (IHT) Thresholds: A Guide for Investors 2024/2025

Navigating the complexities of UK Inheritance Tax (IHT) is a critical component of strategic wealth preservation for any serious investor. The potential for a 40% tax rate to erode the value of an estate is a significant risk, yet confusion over complex rules and the treatment of investment portfolios often leads to inaction. This uncertainty can result in substantial, and frequently avoidable, tax liabilities for beneficiaries. A clear and current understanding of the inheritance tax threshold is the mandatory starting point for any effective estate planning strategy.

This guide provides a direct, functional analysis for the 2024/2025 tax year. We will define the precise IHT thresholds, including the main nil-rate band and the Residence Nil-Rate Band. Furthermore, we will examine the critical reliefs and exemptions that directly impact an investor’s liability, with a specific focus on Business Property Relief (BPR) and its application to qualifying assets. The objective is to provide the foundational knowledge required to assess your estate’s exposure, understand how your portfolio is impacted, and initiate a strategic approach to mitigating your IHT liability.

Key Takeaways

- Establish the current standard Inheritance Tax threshold for the 2024/2025 tax year and understand the conditions under which it can be increased.

- Identify key government-approved allowances and exemptions that can be strategically applied to reduce the taxable value of your estate before IHT is calculated.

- Discover how Business Property Relief (BPR) can provide up to 100% relief from IHT on qualifying business assets, a critical tool for founders and investors.

- Explore advanced estate planning strategies designed for high-net-worth portfolios that require professional financial consultation to implement effectively.

Understanding the Core UK Inheritance Tax Thresholds

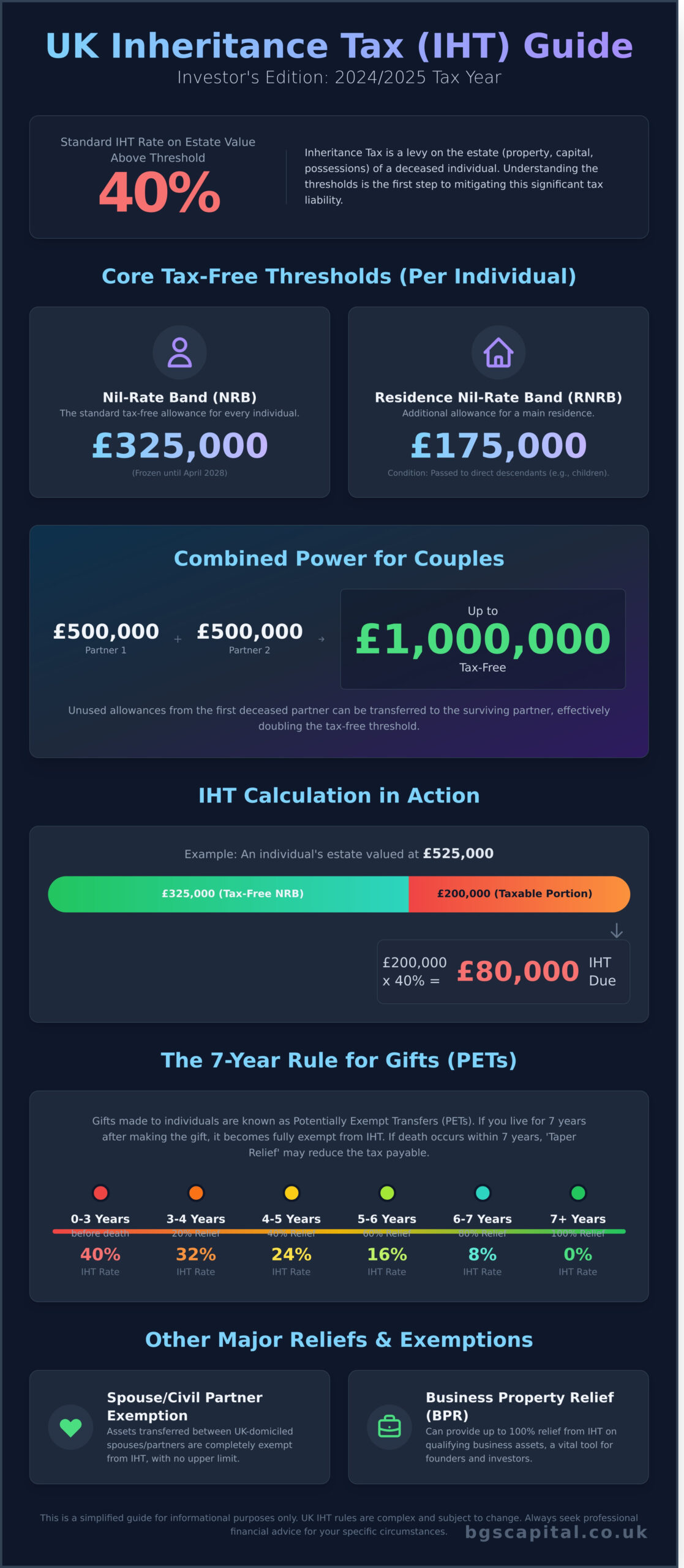

Inheritance Tax (IHT) is a UK levy on the estate-comprising property, capital, and possessions-of an individual who has died. The structure of the modern UK Inheritance Tax System is built around core thresholds designed to exempt a certain value from taxation. Any value above these thresholds is typically taxed at a standard rate of 40%.

Understanding these allowances is the first step in effective estate planning for High Net Worth (HNW) investors. The primary inheritance tax threshold, known as the Nil-Rate Band, is £325,000. Any portion of an estate’s value exceeding this amount may be subject to IHT.

For example, if an individual’s estate is valued at £525,000, the first £325,000 is tax-free. The remaining £200,000 would be subject to a 40% tax, resulting in an IHT liability of £80,000.

The Nil-Rate Band (NRB): The Standard £325,000 Threshold

The Nil-Rate Band (NRB) is the foundational tax-free allowance available to every individual. The current NRB is set at £325,000 and has been frozen at this level until April 2028. This allowance applies to the total value of all assets within an estate, which can include:

- Cash and savings

- Property and land

- Investment portfolios (stocks, shares, funds)

- Personal possessions of value

The NRB is an individual allowance, meaning each person is entitled to their own £325,000 threshold.

The Residence Nil-Rate Band (RNRB): An Extra £175,000 for Property

In addition to the NRB, the Residence Nil-Rate Band (RNRB) provides a further £175,000 allowance. Its application is conditional: it is only available when a main residence is passed directly to children (including adopted, foster, or step-children) or other direct descendants like grandchildren. For HNW estates valued at over £2 million, the RNRB is tapered, reducing by £1 for every £2 the estate’s net value is above this limit.

Combining Thresholds: How Couples Can Pass on up to £1 Million

A key principle in estate planning for married couples and civil partners is the ability to transfer unused IHT allowances. When the first partner dies, any unused portion of their NRB and RNRB can be transferred to the surviving partner’s estate. This mechanism can effectively double the available tax-free amount. The maximum potential allowance is calculated as (£325,000 NRB + £175,000 RNRB) x 2, resulting in a combined threshold of £1,000,000 for the surviving spouse’s estate.

Key Allowances and Exemptions That Reduce Your Taxable Estate

Effective estate planning involves using legitimate, government-approved methods to reduce the taxable value of your estate before Inheritance Tax (IHT) is calculated. These strategies include both lifetime gifts, which may become exempt over time, and assets that are exempt upon death. Diligent record-keeping of all gifts is critical for executors to accurately report to HMRC. Strategically using these allowances can significantly lower the portion of an estate that is subject to the standard inheritance tax threshold. For a detailed breakdown of all regulations, investors should consult the Official IHT Thresholds and Rules published by the UK government.

Spouse or Civil Partner Exemption

One of the most significant IHT exemptions is the ability to transfer assets between spouses or civil partners. These transfers, whether made during your lifetime or as part of your will, are completely exempt from IHT, with no upper limit. This rule applies provided the recipient spouse or partner is domiciled in the UK. If the receiving spouse is not UK-domiciled, the rules are more complex and the lifetime exemption is capped.

The 7-Year Rule and Potentially Exempt Transfers (PETs)

A Potentially Exempt Transfer (PET) is a lifetime gift made to an individual that becomes fully exempt from IHT if you live for seven years after making it. If death occurs within this seven-year period, the gift’s value is counted against your nil-rate band. For gifts that exceed the inheritance tax threshold, tax may be due, but ‘taper relief’ can reduce the amount payable if the gift was made between three and seven years before death.

Taper Relief Scale:

- Years between gift and death 3 to 4: Tax paid is reduced by 20%

- Years between gift and death 4 to 5: Tax paid is reduced by 40%

- Years between gift and death 5 to 6: Tax paid is reduced by 60%

- Years between gift and death 6 to 7: Tax paid is reduced by 80%

Annual Gift Allowances

Several annual allowances permit you to make IHT-free gifts each tax year:

- Annual Exemption: You can give away a total of £3,000 worth of gifts each tax year. This can be given to one person or split among several. Any unused portion can be carried forward, but for one year only.

- Small Gifts Exemption: You can make unlimited gifts of up to £250 per person per tax year, as long as you have not used another exemption on the same person.

- Wedding Gifts: Parents can each gift up to £5,000, grandparents up to £2,500, and anyone else up to £1,000.

- Gifts from Normal Expenditure: For HNW individuals with substantial surplus income, this is a valuable tool. Regular gifts made from your income are immediately exempt, provided they do not affect your standard of living.

Business Property Relief (BPR): A Vital Tool for Founders and Investors

For high-net-worth business owners and investors, Business Property Relief (BPR) is one of the most effective instruments for mitigating Inheritance Tax (IHT). Its primary purpose is to ensure that a trading business can be passed down to the next generation without being sold or broken up to cover an IHT liability. The relief can reduce the value of a relevant business property by either 50% or 100%. To qualify, the assets must typically be held for a minimum of two years prior to death.

What Assets Qualify for 100% BPR?

For sophisticated investors, the 100% relief category is of primary interest. It applies to business assets that carry a higher degree of risk and are central to the UK’s enterprise economy. Key qualifying assets include:

- Shares in an unlisted company: This includes shares in private limited companies and pre-IPO businesses, which are a core focus for investors seeking high-growth opportunities.

- A controlling interest in a listed company: Holding more than 50% of the shares in a company listed on a main exchange.

- Shares traded on the Alternative Investment Market (AIM): Most, but not all, AIM-listed shares qualify for BPR, making it a popular market for estate planning.

Understanding the Conditions and Exclusions

Qualification for BPR is not automatic. The fundamental condition is that the company must be a ‘trading’ entity. Businesses engaged wholly or mainly in dealing with investments, such as stocks, shares, land, or buildings, are explicitly excluded. Furthermore, even in a qualifying trading company, assets not used for the purpose of the business-known as ‘excepted assets’ like significant cash balances beyond operational needs-can result in a partial restriction of the relief. Correctly structuring business activities is therefore critical to securing and maintaining BPR status.

How BPR Impacts Your IHT Threshold

The strategic power of BPR lies in how it interacts with the standard inheritance tax threshold. Qualifying assets are deducted from the total value of the estate before any IHT calculation is made. This means BPR-eligible assets do not use up the Nil-Rate Band (£325,000) or the Residence Nil-Rate Band.

For example, consider an estate valued at £2.5 million, which includes a £1 million shareholding in a qualifying AIM-listed company. The £1 million business value receives 100% BPR and is removed from the estate, leaving a chargeable value of £1.5 million. The full Nil-Rate Band is then applied to this remaining sum. The mechanics are further defined in the UK government’s official Inheritance Tax guidance. This mechanism makes BPR an essential component of estate planning for individuals with significant business interests.

Advanced IHT Planning for High-Net-Worth Portfolios

For high-net-worth investors whose estates are projected to substantially exceed the standard nil-rate bands, basic allowances are often insufficient. Advanced IHT planning moves beyond simple gifting to incorporate structured, long-term strategies designed to preserve wealth and build a tax-efficient legacy. The objective is not tax avoidance, but legitimate and meticulous planning to mitigate IHT liabilities on complex portfolios.

These strategies are complex and carry significant financial implications. It is imperative to seek professional financial and legal advice tailored to your specific circumstances before implementation.

Using Trusts for Estate Planning

Trusts are a foundational tool in sophisticated estate planning, allowing you to legally transfer assets out of your name while retaining a degree of control over their management and distribution. By placing assets into a trust, they can be removed from your estate for IHT purposes after seven years. Different structures, such as bare trusts and discretionary trusts, serve distinct purposes. Be aware that setting up certain trusts can trigger an immediate tax charge, making expert guidance essential.

Investing in Tax-Advantaged Schemes (EIS & SEIS)

Certain investments that qualify for Business Property Relief (BPR) can provide 100% relief from IHT. Shares in companies qualifying for the Enterprise Investment Scheme (EIS) or Seed Enterprise Investment Scheme (SEIS) typically benefit from BPR. Once held for a minimum of two years, these shares become fully exempt from inheritance tax. This presents a dual benefit for investors: supporting UK growth companies with high-growth potential while simultaneously executing an effective IHT mitigation strategy. Explore vetted, high-growth investment opportunities.

Life Insurance and Pensions

A simple yet effective strategy involves using a life insurance policy written ‘in trust’. This ensures that upon your death, the policy payout is made directly to your beneficiaries without entering your estate, thereby avoiding the 40% IHT charge. The funds can then be used by your beneficiaries to cover any IHT bill due. Furthermore, most modern defined contribution pensions fall outside of your estate and are not subject to IHT, making them a highly efficient vehicle for passing on wealth and a critical component to consider when assessing your total inheritance tax threshold exposure.

Strategic Estate Planning: Final Thoughts on IHT

Mastering the UK’s Inheritance Tax framework is a critical component of effective wealth preservation for any serious investor. Understanding the core inheritance tax threshold and associated nil-rate bands provides the foundation, but true optimisation often lies in advanced strategies. For business owners and high-net-worth individuals, leveraging powerful reliefs like Business Property Relief (BPR) can significantly reduce or even eliminate an IHT liability on qualifying assets.

Many BPR-qualifying opportunities are found within unlisted, high-growth UK companies. Gaining access to these investments requires a specialist network. As specialists in pre-IPO and growth-stage capital introductions, BGS Capital connects qualified investors directly with the founders of innovative companies and a network of accredited UK investment firms. By exploring these avenues, you can align your portfolio with your long-term estate planning objectives.

Am I Eligible to View Pre-IPO Investment Opportunities?

Proactive engagement with these strategies is the definitive step towards securing your financial legacy.

Frequently Asked Questions: UK Inheritance Tax

What is the current Inheritance Tax threshold in the UK for 2024/2025?

For the 2024/2025 tax year, the standard Inheritance Tax threshold, known as the Nil-Rate Band (NRB), is £325,000. This figure has been frozen by the government and is scheduled to remain at this level until April 2028. In addition to the NRB, qualifying estates can utilise the Residence Nil-Rate Band (RNRB) of £175,000 when a primary residence is passed to direct descendants, potentially increasing an individual’s total tax-free allowance to £500,000.

Can my unused IHT threshold be transferred to my spouse?

Yes, the transfer of unused allowances to a surviving spouse or civil partner is a fundamental component of estate planning. Any unused percentage of an individual’s Nil-Rate Band (NRB) and Residence Nil-Rate Band (RNRB) can be claimed by the estate of their surviving partner upon their death. This mechanism can effectively double the available tax-free threshold for the second partner’s estate to a potential maximum of £1 million, subject to all qualifying conditions being met.

Do I pay Inheritance Tax on gifts I receive from someone?

No, the recipient of a lifetime gift is not liable for Inheritance Tax. The potential tax liability falls upon the estate of the donor if they pass away within seven years of making the gift. These are known as Potentially Exempt Transfers (PETs). If the donor survives for seven years post-gift, its value becomes fully exempt from their estate’s IHT calculation. If not, the value of the gift is added back into the estate for IHT assessment.

How does the Residence Nil-Rate Band (RNRB) work if I sell my home and downsize?

The RNRB includes downsizing provisions to ensure individuals are not penalised for selling a more valuable home. If you sell a qualifying residence after 8 July 2015 and leave assets of an equivalent value to direct descendants, your estate can claim a “downsizing addition.” This allows the estate to benefit from the RNRB that would have been available on the former, more valuable property, ensuring the tax relief is not lost due to downsizing or moving into care.

Are company shares always exempt from Inheritance Tax?

No, exemption is not automatic. Certain company shares may qualify for 100% relief from Inheritance Tax through Business Property Relief (BPR). This typically applies to shares in unlisted trading companies, including those on the Alternative Investment Market (AIM), that have been held for a minimum of two years. Shares in companies listed on a main stock exchange or those primarily engaged in investment activities, such as holding property, generally do not qualify for BPR.

How are pensions treated for Inheritance Tax purposes?

Most modern defined contribution pension plans are held in a trust structure, placing them outside of an individual’s estate for Inheritance Tax calculations. This makes them a highly efficient vehicle for wealth transfer. If the pension holder dies before age 75, beneficiaries can typically inherit the fund tax-free. If death occurs at or after 75, beneficiaries will be liable for income tax at their marginal rate on any withdrawals from the inherited pension.

What happens to the IHT threshold if the government changes?

The Inheritance Tax threshold and its associated rules are legislated by the sitting government and are subject to change. A new administration may choose to alter tax policy, which could involve raising, lowering, or freezing the thresholds, or implementing wider reforms. Any such modifications are typically announced in a fiscal event like the Spring Budget or Autumn Statement. Consequently, robust estate planning must account for this political and legislative risk to remain effective over the long term.