Navigating the complexities of UK government venture capital schemes presents a significant challenge for both early-stage companies and sophisticated investors. The official guidance is often dense, the eligibility criteria are stringent, and the potential tax benefits can be difficult to quantify. For founders seeking crucial funding and investors targeting high-growth opportunities, a clear understanding of the seed enterprise investment scheme (SEIS) is not just beneficial-it is essential for strategic decision-making and capital efficiency.

This comprehensive guide is designed to demystify the SEIS. We will provide a direct, functional breakdown of how the scheme operates, detailing the precise rules a company must meet to qualify and the substantial tax reliefs available to investors. This article clarifies the key differences between SEIS and the Enterprise Investment Scheme (EIS), outlines the application process, and provides a professional assessment of the risks inherent in early-stage investing. The objective is to equip you with the critical information needed to confidently evaluate and leverage the SEIS framework.

Key Takeaways

- Understand the significant tax reliefs available to investors, including up to 50% income tax relief, to mitigate the high risks associated with early-stage ventures.

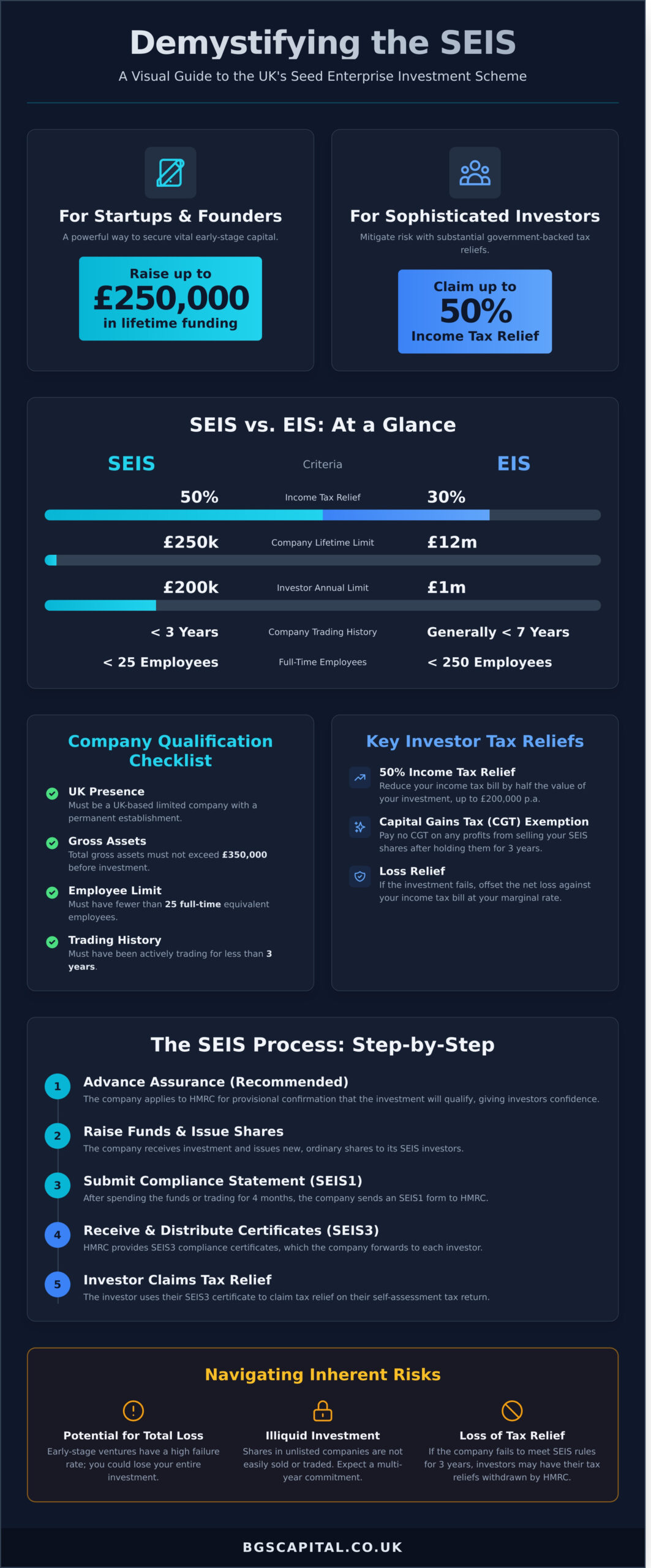

- Determine if your startup meets the strict eligibility criteria to raise up to £250,000 through the Seed Enterprise Investment Scheme.

- Navigate the end-to-end SEIS process, from securing Advance Assurance from HMRC to issuing compliance certificates to your investors.

- Evaluate the inherent risks of SEIS investing, such as the potential for total capital loss and the illiquid nature of unlisted company shares.

What is the Seed Enterprise Investment Scheme (SEIS)?

The Seed Enterprise Investment Scheme (SEIS) is a UK government initiative designed to stimulate private investment into the nation’s earliest-stage companies. Its primary objective is to help startups and new businesses raise essential equity finance by offering significant tax advantages to investors. In essence, the scheme provides a powerful incentive for individuals to commit capital to high-risk, high-potential ventures that might otherwise struggle to secure funding.

The Seed Enterprise Investment Scheme operates on a clear trade-off: in exchange for taking on the considerable risk associated with investing in a startup, investors receive exceptionally generous tax reliefs. The process involves three key parties: the qualifying startup seeking capital, the individual investor providing the funds, and His Majesty’s Revenue and Customs (HMRC), which administers the scheme and grants the tax relief upon compliance. This structure makes SEIS a cornerstone of the UK’s venture capital landscape for seed-stage businesses.

SEIS vs. EIS: Key Differences

While often mentioned together, SEIS is distinct from its counterpart, the Enterprise Investment Scheme (EIS). SEIS is specifically targeted at the very beginning of a company’s life cycle.

- Investment Stage: SEIS is for ‘seed’ stage companies, typically pre-revenue or in their infancy. EIS is for larger, more established SMEs that are scaling up.

- Investor Limit: Under SEIS, an individual can invest a maximum of £200,000 per tax year. The EIS limit is £1 million (or £2 million for knowledge-intensive companies).

- Company Limit: A company can raise a lifetime maximum of £250,000 through SEIS. The EIS lifetime limit is £12 million.

- Income Tax Relief: SEIS offers a more generous 50% income tax relief on the amount invested, compared to 30% for EIS.

- Company Criteria: To qualify for SEIS, a company must have been trading for less than three years and have fewer than 25 full-time employees.

The Core Principles of the Scheme

To maintain its integrity and focus, the SEIS is governed by several fundamental principles. The “risk to capital” condition is paramount; the investment must represent a genuine risk to the investor’s capital, and the scheme cannot be used for capital preservation or low-risk ventures. Furthermore, the investment must be deployed in a qualifying trade-most sectors are eligible, but certain activities like banking, insurance, and property development are excluded. Finally, the funds raised must be used for the growth and development of the qualifying business, not for acquiring other businesses or assets.

For Companies: How to Qualify for SEIS Funding

For early-stage founders, the seed enterprise investment scheme provides a critical pathway to securing foundational capital. The scheme allows an eligible company to raise a lifetime maximum of £250,000. To attract sophisticated investors, a comprehensive business plan and detailed financial forecasts are not merely procedural; they are essential tools to demonstrate viability and a clear strategy for growth. Understanding the qualification criteria is the first step in leveraging this powerful government-backed initiative.

Securing investment is contingent on meeting strict HMRC rules. According to the official SEIS scheme background, these regulations are designed to ensure funds are directed towards genuine, high-risk, early-stage ventures. Furthermore, the company must continue to meet qualifying conditions for at least three years after the investment is made, otherwise your investors risk losing their valuable tax reliefs.

Company Eligibility Criteria

To qualify for the seed enterprise investment scheme, a company must satisfy several key conditions at the time of the share issue. The core requirements include:

- UK Presence: The company must be a UK-based limited company and be establishing a new, qualifying trade.

- Gross Assets: Total gross assets must not exceed £350,000 immediately before any SEIS shares are issued.

- Employee Limit: The company must have fewer than 25 full-time equivalent employees.

- Trading History: The company must have been actively trading for less than three years.

The Role of Advance Assurance

Advance Assurance is a provisional confirmation from HMRC that the company and its proposed share issue meet the scheme’s qualifying conditions. While not a mandatory requirement, it is highly recommended. Most experienced investors will not consider an SEIS opportunity without it, as it provides significant confidence that their investment will be eligible for tax relief. To apply, you will typically need to submit your business plan, financial forecasts, and details of the proposed investment.

Issuing Shares and Compliance

The investment must be made in exchange for new, ordinary shares, which must be fully paid for in cash upon issue. Once the investment is received and shares are issued, the company has a statutory duty to manage compliance. This involves submitting a compliance statement (form SEIS1) to HMRC. After reviewing and approving the statement, HMRC will issue unique compliance certificates (forms SEIS3) for the company to provide to each of its investors, enabling them to claim their tax relief.

For Investors: Analysing SEIS Tax Reliefs and Risks

The Seed Enterprise Investment Scheme (SEIS) is specifically designed for sophisticated investors who are comfortable with the high-risk profile of early-stage ventures. While the potential for high returns exists, the primary appeal lies in the substantial, government-backed tax reliefs designed to mitigate the inherent risks of investing in startups. An individual can invest a maximum of £200,000 per tax year through the scheme. It is critical to understand that these investments are highly illiquid; shares are not publicly traded and must be held for a minimum of three years to retain the associated tax benefits. Your capital is at risk.

The Five Key SEIS Tax Benefits

The government offers a comprehensive suite of tax incentives to encourage investment into qualifying businesses. These reliefs significantly alter the risk-reward calculation for investors.

- Income Tax Relief: Investors can claim a 50% income tax credit on the amount invested. For a £100,000 investment, this translates to a £50,000 reduction in your income tax liability for that year.

- Capital Gains Tax (CGT) Exemption: If the shares are held for at least three years and then sold for a profit, the entire gain is 100% exempt from Capital Gains Tax.

- Loss Relief: Should the company fail and the shares become worthless, investors can offset the net loss (the initial investment minus the 50% income tax relief already claimed) against their income tax.

- CGT Reinvestment Relief: An investor can exempt 50% of a capital gain realised from the sale of any asset, provided the gain is reinvested into a qualifying SEIS company in the same tax year.

- Inheritance Tax (IHT) Relief: After a holding period of two years, SEIS shares may qualify for Business Property Relief, making them 100% exempt from Inheritance Tax.

Understanding the High-Risk Nature

Despite the generous tax incentives, the high-risk nature of the seed enterprise investment scheme cannot be overstated. Startups have a statistically high failure rate, and there is a significant chance of losing all invested capital. The shares are unquoted and illiquid, meaning they cannot be easily sold or transferred. Furthermore, all tax reliefs are conditional. They can be withdrawn by HMRC if the company fails to adhere to the strict SEIS rules for three years after the investment is made. Thorough due diligence is essential.

Investors must carefully assess their risk tolerance and financial position before committing capital. Connect with pre-vetted investment opportunities.

The SEIS Process: A Step-by-Step Walkthrough

Navigating the Seed Enterprise Investment Scheme requires a structured, multi-phase approach involving coordinated actions between the startup, the investor, and HMRC. This chronological overview outlines the critical path from initial company preparation to the investor’s successful tax relief claim.

Phase 1: Company Preparation and Fundraising

- Confirm Eligibility and Prepare Documentation: The company must first verify that it meets all strict SEIS qualifying criteria. This involves preparing a comprehensive business plan and detailed financial projections to present a viable investment case.

- Apply for Advance Assurance (Recommended): While not mandatory, applying to HMRC for Advance Assurance is a crucial step. It provides a provisional confirmation that the investment is likely to qualify for SEIS, giving potential investors significant confidence before they commit capital.

- Engage Investors and Secure Investment: With a solid plan and Advance Assurance in place, the company can actively engage with potential investors to secure funding commitments, up to the maximum SEIS limit of £250,000.

Phase 2: Investment and Compliance

- Investor Subscribes for Shares: The investor provides the agreed capital and subscribes for new, ordinary shares in the company. The payment must be made in full and in cash.

- Issue Shares and Deploy Funds: The company formally issues the shares to the investor. It must then use the invested funds for qualifying business activities as outlined in its business plan and within the scheme’s rules.

- Submit SEIS1 Compliance Statement: After trading for at least four months or having spent 70% of the invested funds, the company must submit a compliance statement (form SEIS1) to HMRC. This statement confirms all rules have been met.

Phase 3: Investor Claims Tax Relief

- HMRC Issues SEIS3 Certificates: Following a successful review of the SEIS1 form, HMRC will authorise the company to issue compliance certificates (form SEIS3) to its investors.

- Investor Claims Tax Relief: The investor uses their unique SEIS3 certificate to claim their 50% income tax relief. This is typically done through their annual Self Assessment tax return.

- Maintain Compliance for Three Years: A critical final requirement of the seed enterprise investment scheme is that both the company and the investor must continue to meet the qualifying conditions for at least three years from the date the shares were issued. A breach of the rules can lead to the withdrawal of tax relief.

Understanding this regulated process is essential for participants. At BGS Capital, we provide a network for sophisticated investors to connect with qualifying high-growth companies. Discover opportunities by exploring our platform at bgscapital.co.uk.

Unlocking Growth with the Seed Enterprise Investment Scheme

The Seed Enterprise Investment Scheme is a powerful UK government initiative, offering a crucial pathway for early-stage companies to secure funding while providing investors with substantial tax reliefs. For founders, it represents a vital source of capital; for investors, it is a high-risk, high-reward opportunity mitigated by generous tax incentives. Successfully navigating the scheme’s strict requirements is fundamental for both parties to realise its full potential.

For qualifying growth-stage companies ready to secure investment, connecting with the right network is paramount. BGS Capital operates as an introducer, providing access to a network of high-net-worth and sophisticated investors. We facilitate direct introductions to investor relations teams, positioning pre-IPO and growth-stage companies in front of serious capital. Take the next step to accelerate your funding journey.

RAISING CAPITAL? FEATURE YOUR BUSINESS

Frequently Asked Questions

What is the difference between SEIS and EIS?

SEIS (Seed Enterprise Investment Scheme) is designed for very early-stage, high-risk companies, while EIS (Enterprise Investment Scheme) targets larger, more established ventures. The primary distinctions are in the tax reliefs and investment limits. SEIS offers 50% income tax relief on investments up to £200,000 per tax year. In contrast, EIS provides 30% relief on investments up to £1 million. Companies seeking SEIS funding must be under three years old and can raise a maximum of £250,000 under the scheme.

Can a company director invest in their own company under SEIS?

A director is generally prohibited from investing in their own company under SEIS due to being a “connected” individual. However, an exception exists if the individual is appointed as a director only after their shares have been issued. They cannot be a director or employee at the time of the share issue. The rules are stringent, and contravention can invalidate the tax relief. Seeking professional advice to ensure full compliance with HMRC regulations is strongly recommended.

What are ‘excluded trades’ under the Seed Enterprise Investment Scheme?

Certain business activities are deemed non-qualifying or ‘excluded trades’ under the Seed Enterprise Investment Scheme. These are typically lower-risk, asset-backed, or finance-based sectors. Examples include dealing in land or commodities, banking, insurance, money-lending, and providing legal or accountancy services. Additionally, property development, farming, forestry, and certain energy generation activities are also excluded. Companies must confirm their trade qualifies before seeking investment under the scheme.

How long do I need to hold SEIS shares to keep the tax relief?

To retain the full income tax relief granted under SEIS, an investor must hold the shares for a minimum period of three years from the date they are issued. Disposing of the shares before this three-year threshold has passed will typically result in the withdrawal, or “clawback,” of the tax relief by HMRC. This holding period is also a condition for qualifying for Capital Gains Tax (CGT) exemption on any profits realised upon the eventual disposal of the shares.

What happens if a company I invest in loses its SEIS status?

If a company fails to meet the SEIS qualifying conditions at any point during the three years following your investment, HMRC can withdraw your tax relief. This means you may be required to repay the 50% income tax relief you initially claimed. A company can lose its status for various reasons, such as engaging in an excluded trade, exceeding funding limits, or failing to use the invested funds for a qualifying business activity. Investor due diligence on the company’s ongoing compliance is crucial.

Is Advance Assurance a guarantee of SEIS eligibility?

Advance Assurance from HMRC is not a formal guarantee of SEIS eligibility. It is a provisional statement indicating that, based on the information supplied by the company, the investment is likely to qualify. However, HMRC reserves the right to withhold final certification if the information provided was inaccurate or misleading, or if the company fails to adhere to the scheme’s rules after the investment is made. It serves as a strong indicator for investors, but not a binding commitment.