The mandate for Making Tax Digital (MTD) from HMRC introduces a significant operational shift for UK businesses. Navigating the phased deadlines for VAT and Income Tax Self Assessment (ITSA), selecting compliant software, and mitigating the risk of penalties for non-compliance are critical concerns for directors and sole traders alike. The complexity of the rules can lead to operational disruption and financial risk if not managed with precision.

This definitive guide provides a direct, functional framework for achieving full compliance. We will detail precisely who MTD applies to, outline the critical deadlines you must meet, and analyse the criteria for selecting the correct software for your operations. By following this guide, you will gain the clarity required to transition your business to MTD efficiently, securing your compliance and positioning your company for continued strategic growth without disruption.

Key Takeaways

- Identify your specific MTD compliance deadline to mitigate the risk of penalties and ensure timely preparation.

- Follow an actionable, step-by-step checklist to streamline your business’s transition to digital tax submissions.

- Understand the software requirements for making tax digital and learn how to select a solution that enhances operational efficiency.

- Discover how to leverage MTD compliance as a strategic opportunity to improve financial oversight and support business growth.

What is Making Tax Digital (MTD)? The Essentials Explained

Making Tax Digital (MTD) is a fundamental change to the United Kingdom’s tax administration system, initiated by HM Revenue & Customs (HMRC) to create a modern, fully digitised process. The primary objective of this initiative is to make tax administration more effective, efficient, and simpler for taxpayers. For a detailed background, the Wikipedia entry on What is Making Tax Digital? provides a comprehensive overview. It is critical to understand that MTD is not a new tax; it is a new, mandatory method for recording and reporting tax information to HMRC through digital means.

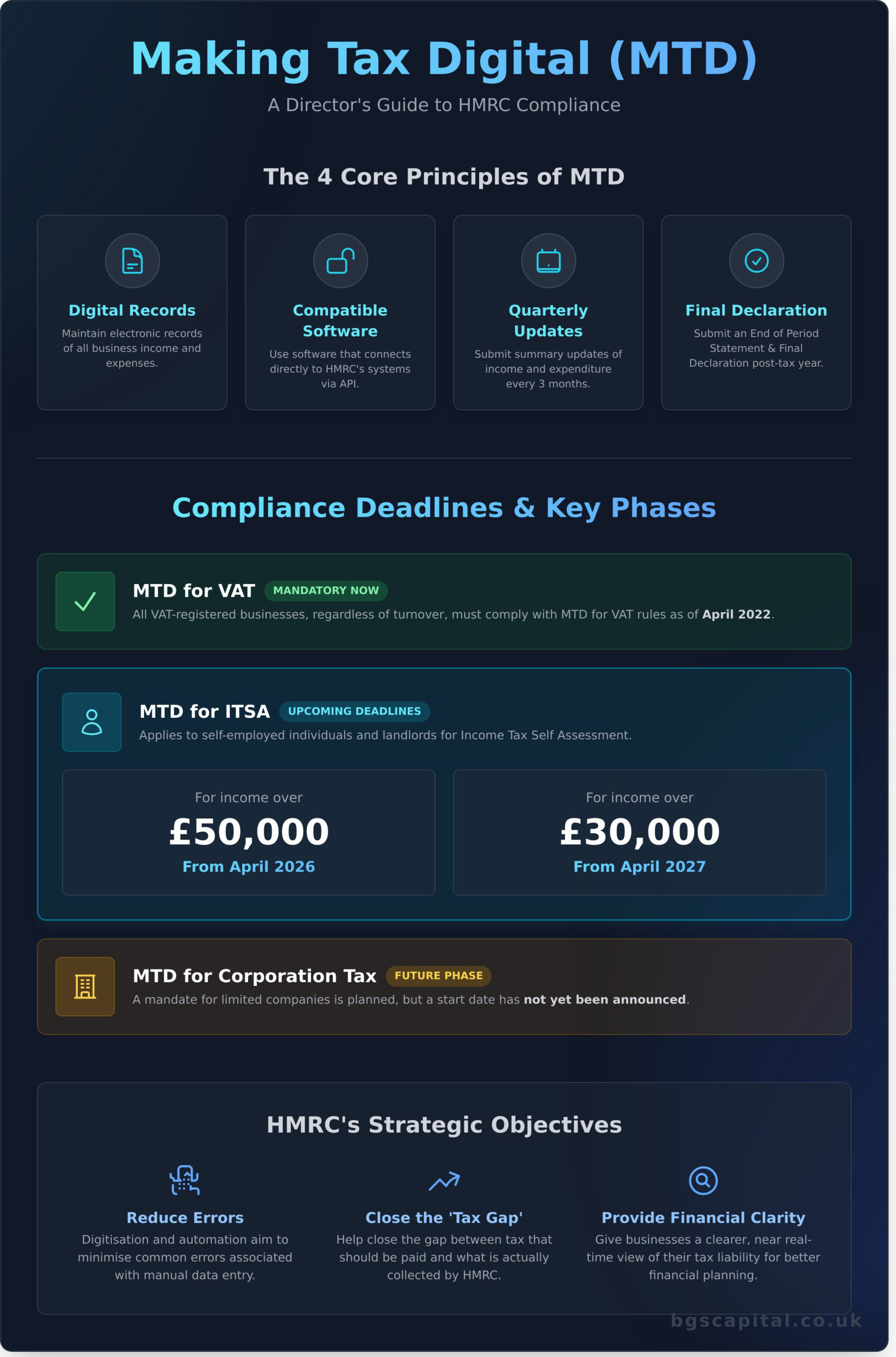

The Core Principles of MTD

Compliance with the making tax digital framework is built upon four key components that businesses must integrate into their accounting processes:

- Digital Records: Businesses are required to maintain specific financial records electronically. This includes data on business income and expenses, stored within a compatible software program or spreadsheet.

- Compatible Software: All submissions must be made using functional, compatible software that can connect directly to HMRC’s systems via an Application Programming Interface (API). Manual submission through the HMRC portal is no longer permitted for in-scope entities.

- Quarterly Updates: Businesses must submit summary updates of their income and expenditure to HMRC at least every three months. These updates provide a more current view of a business’s tax position.

- End of Period Statement (EOPs) and Final Declaration: Following the tax year, businesses must submit an End of Period Statement to finalise their taxable profit for the period, followed by a Final Declaration to confirm all tax liabilities.

Who Does MTD Apply To?

The MTD rollout is phased, with different business types brought into the system over time. The key groups affected are:

- VAT-Registered Businesses: MTD for VAT is now mandatory for all VAT-registered businesses, regardless of turnover.

- Self-Employed Individuals and Landlords: MTD for Income Tax Self Assessment (ITSA) will apply to individuals with business or property income above a specified threshold, with implementation scheduled in the coming years.

- Limited Companies: MTD for Corporation Tax is planned for the future, although a specific start date has not yet been mandated.

HMRC’s Stated Objectives for MTD

HMRC has outlined several strategic goals for implementing this system-wide change, focused on improving the accuracy and efficiency of the UK tax system:

- Reduce Errors: By digitising records and automating submissions, HMRC aims to minimise the common errors associated with manual data entry and complex calculations.

- Close the ‘Tax Gap’: The initiative is designed to help close the tax gap-the difference between the amount of tax that should be paid and what is actually collected.

- Provide a Clearer Tax Position: Regular digital updates give businesses a more accurate, near-real-time understanding of their tax liability, enabling better financial planning and cash flow management.

MTD Deadlines and Key Phases: Who Needs to Comply and When?

The transition to Making Tax Digital is a phased process, with distinct deadlines for various taxes and business structures. Compliance is not optional, and understanding your specific start date is critical for avoiding penalties. HMRC has adjusted these timelines previously, so it is imperative that businesses refer to the latest official guidance to ensure they are prepared.

This section provides a clear overview of the key MTD deadlines as they currently stand.

MTD for VAT: A Recap of the Rules

MTD for Value Added Tax (VAT) is now fully implemented and mandatory for all VAT-registered businesses. The rollout began in April 2019 for businesses with a taxable turnover exceeding the £85,000 threshold. From April 2022, these rules were extended to all VAT-registered businesses, regardless of turnover. Consequently, all VAT returns must now be submitted to HMRC using MTD-compatible software.

MTD for Income Tax Self Assessment (ITSA)

The next major phase targets sole traders and landlords who file Income Tax Self Assessment returns. The start date is determined by your total qualifying annual income, which is the combined gross turnover from your business and property rentals. According to the Official MTD for Income Tax rules, the system requires quarterly updates and a final declaration, with deadlines structured as follows:

| Annual Qualifying Income | MTD for ITSA Start Date |

|---|---|

| Over £50,000 | From 6 April 2026 |

| Over £30,000 | From 6 April 2027 |

The government has stated that individuals with qualifying income below £30,000, as well as general partnerships, will be mandated to join MTD for ITSA at a future date, which is yet to be confirmed.

The Future: MTD for Corporation Tax

While MTD for Corporation Tax (CT) is part of the government’s long-term tax digitisation strategy, its implementation is not imminent. HMRC has confirmed that MTD for CT will not be mandated before April 2026 at the earliest. A voluntary pilot is expected to launch ahead of this date to allow companies to test the system. Businesses should monitor official announcements from HMRC for definitive timelines and requirements.

How to Prepare for MTD: A Step-by-Step Compliance Checklist

Transitioning to the making tax digital framework is a structured process. A methodical approach removes complexity and ensures your business achieves full compliance efficiently. This checklist breaks down the preparation into three manageable stages, from initial assessment to final registration with HMRC.

Step 1: Assess Your Current Record-Keeping

The foundation of MTD compliance is accurate digital record-keeping. Before selecting any new systems, you must first evaluate your current processes to identify any gaps. A thorough assessment is critical for a seamless transition.

- Review current methods: Document how you currently record business income and expenses. Are you using spreadsheets, desktop software, or paper-based ledgers?

- Identify compliance gaps: Compare your system against MTD’s requirement for all records to be stored and submitted digitally. Spreadsheets, for instance, may require bridging software to become compliant.

- Determine who will manage submissions: Decide if you will handle MTD filings internally or if you will authorise a tax agent or accountant to manage them on your behalf. This decision will influence your software choice.

Step 2: Choose MTD-Compatible Software

Selecting the correct software is a critical decision. Your chosen platform must be able to communicate directly with HMRC’s systems. The first step is to consult the government’s official guidance on Choosing MTD-compatible software, which provides a comprehensive list of approved providers. Your choice will depend on your business’s complexity and existing systems.

- Full accounting package vs. bridging software: A full package (e.g., Xero, QuickBooks) manages all bookkeeping and submits directly to HMRC. Bridging software connects non-compatible spreadsheets to HMRC’s MTD system.

- Key considerations: Evaluate options based on cost (monthly subscription fees), features (invoicing, payroll, bank feeds), and its ability to integrate with your business bank accounts.

Step 3: Sign Up for MTD with HMRC

Once you have a compliant system in place, the final step is to formally sign up for the relevant MTD service. It is imperative to complete this step well in advance of your mandated start date to avoid penalties. You must sign up for MTD for VAT or MTD for Income Tax Self Assessment (ITSA) separately via the GOV.UK website. Have the following information ready:

- Your Government Gateway user ID and password.

- Your VAT registration number (for MTD for VAT).

- Your National Insurance number and Unique Taxpayer Reference (UTR) for ITSA.

Do not wait until your deadline approaches. Sign up as soon as your software is operational to ensure a smooth first submission.

Choosing MTD Software: A Strategic Business Decision

Selecting MTD-compliant software is a critical operational decision that extends far beyond simple tax compliance. The right platform can serve as the financial backbone of your enterprise, enhancing efficiency, providing strategic insights, and reducing administrative overhead. Viewing this choice through a strategic lens ensures your business not only meets HMRC’s requirements for making tax digital but also gains a significant competitive advantage through streamlined financial management.

Full Accounting Software vs. Bridging Software

Businesses must choose between two primary categories of MTD-compatible software. Full accounting platforms like Xero or QuickBooks offer an integrated solution for all financial record-keeping. In contrast, bridging software provides a direct link between your existing spreadsheets and HMRC’s systems, acting solely as a submission tool.

Full Accounting Software

- Pros: Centralises all financial data, automates bookkeeping tasks, provides real-time reporting, and reduces the risk of manual data entry errors.

- Cons: Higher monthly subscription costs and requires an initial setup and learning period.

Bridging Software

- Pros: Lower cost, allows businesses to continue using established spreadsheet systems, and requires minimal training.

- Cons: Higher risk of formula or data errors in spreadsheets, lacks automation features, and offers no additional business management tools.

Key Features to Look For in MTD Software

When evaluating software, prioritise features that deliver operational value. Essential capabilities include:

- Bank Feeds: Automatically import bank transactions to simplify reconciliation.

- Invoicing and Expenses: Create, send, and track professional invoices and manage supplier bills efficiently.

- Real-Time Reporting: Access dashboards for instant analysis of cash flow, profit and loss, and balance sheets.

- Integrations: Seamless connection with payroll, CRM, or project management systems to create a unified operational environment.

Evaluating Costs and Long-Term Value

Subscription costs for full accounting software typically range from £10 to £30+ per month. While free MTD software options exist, they often have limited functionality. The primary consideration should be the return on investment (ROI). The time saved on administrative tasks and the value of accurate, real-time financial data for strategic decision-making often far outweigh the monthly fee. Effective financial management is fundamental to business growth and investor readiness. For insights into securing capital for your enterprise, explore the opportunities at bgscapital.co.uk.

Beyond Compliance: The Strategic Benefits of MTD for Business Growth

Viewing Making Tax Digital purely as a regulatory requirement is a significant missed opportunity. For ambitious companies, MTD is not a burden but a catalyst for modernising financial operations and establishing a foundation for scalable growth. The mandated shift to digital record-keeping imposes a level of financial discipline that directly supports strategic objectives, from optimising cash flow to attracting external capital.

Improved Financial Visibility and Cash Flow Management

The core benefit of MTD-compliant software is the transition from historical accounting to real-time financial intelligence. With up-to-date data on revenue, expenditure, and profitability, leadership can track performance with precision. This clarity enables more accurate cash flow forecasting, robust budgeting, and the ability to make proactive, data-driven decisions regarding inventory, staffing, and capital allocation. It replaces guesswork with strategic certainty.

Streamlining Operations and Reducing Administrative Burden

Digital systems fundamentally reduce the time and cost associated with financial administration. The operational advantages are immediate and tangible:

- Process Automation: Tasks such as bank reconciliation, expense categorisation, and VAT return preparation are automated, freeing up valuable internal resources to focus on growth activities.

- Accelerated Payments: Digital invoicing and integrated payment systems can significantly shorten payment cycles, directly improving a company’s cash position.

- Centralised Data: Having all financial information in one secure, accessible platform provides a single source of truth for reporting, analysis, and strategic planning.

Becoming Investor-Ready with Clean, Digital Financials

For any business seeking external investment, transparent and accurate financial records are non-negotiable. Investors and lenders require unimpeachable data to conduct due diligence. Compliance with making tax digital serves as a clear signal of a well-managed, professional operation with robust financial controls. Organised digital accounts streamline the due diligence process, reducing friction and accelerating the timeline from initial contact to funding. A business with its financial house in order is an inherently more credible and attractive investment proposition. Once your financials are in order, the next step is growth. Feature Your Business to Connect with Investors.

Making Tax Digital: From Compliance to Strategic Advantage

The move to digital tax is a fundamental change for UK businesses. As we’ve explored, successful compliance hinges on understanding key deadlines, adopting compatible software, and maintaining precise digital records. However, the true value lies beyond meeting regulatory requirements. By embracing this change, you gain unparalleled, real-time insight into your financial performance, transforming a mandatory obligation into a powerful tool for strategic decision-making and operational efficiency.

Ultimately, the transition to making tax digital is more than a regulatory hurdle; it is a catalyst for growth. With your financial operations streamlined and data-driven, your business is now better positioned for the next phase of strategic expansion and attracting serious investment.

Ready to leverage this new efficiency for significant growth? Feature your business to our network of sophisticated investors. Gain direct access to our network of accredited investment firms and wealth managers, connect with investor relations teams, and showcase your opportunity to qualified high-net-worth individuals seeking their next venture.

Frequently Asked Questions

What are the penalties for non-compliance with Making Tax Digital?

HMRC operates a penalty point system for late MTD submissions. For each missed deadline, your business accrues one point. Once a penalty threshold is reached-typically four points for quarterly filers-a £200 financial penalty is issued. An additional £200 penalty is then applied for every subsequent late submission while the business remains at the threshold. These penalties are distinct from any penalties for the late payment of tax itself.

Can I be exempt from Making Tax Digital?

Exemption from Making Tax Digital is possible but only under specific circumstances defined by HMRC. Your business may be eligible if it is not practical for you to use digital tools due to age, disability, or location (e.g., no internet access). Exemption may also be granted on religious grounds. A business must formally apply to HMRC and receive confirmation of its exempt status; you cannot simply decide not to comply.

Do I still need an accountant if I use MTD software?

Yes, it is highly advisable. While MTD-compatible software automates the submission of tax data, it does not replace the strategic expertise of an accountant. An accountant provides essential services such as tax planning, identifying potential savings, ensuring overall accuracy, and offering financial advice that software cannot. The software is a compliance tool; the accountant is a financial professional who helps optimise your business’s tax position.

How much will MTD-compatible software cost my business?

The cost of MTD-compatible software varies based on the complexity of your business’s needs. Basic, entry-level cloud accounting packages typically range from £10 to £30 per month. More comprehensive solutions with features like payroll, inventory management, and multi-currency support will incur higher costs. Some free software is available, but it often has functional limitations. Businesses should budget for this as a standard operational expense.

Can I continue to use spreadsheets for Making Tax Digital?

You can use spreadsheets, but not as a standalone solution. To remain compliant, your spreadsheets must be digitally linked to MTD-compatible software using ‘bridging software’. This software connects your spreadsheet to HMRC’s systems to submit the required data digitally. Manual data transfer, such as copying and pasting totals from a spreadsheet into a web form, is not compliant with MTD rules. The digital records must be maintained within the spreadsheet.

What happens if I miss an MTD quarterly submission deadline?

Missing a quarterly submission deadline results in your business receiving one penalty point from HMRC. You will not face an immediate financial penalty for the first missed deadline. However, once you accumulate a set number of points (four points for quarterly submissions), a £200 penalty will be levied. This system is designed to penalise persistent non-compliance rather than isolated errors, but consistent failure to meet deadlines will result in financial consequences.